In today's era where upward economic mobility is celebrated and showcased through soaring stock indices, luxury real estate booms, and high-tech consumerism, we are too much dependent on outward projections of wealth. Somehow, this aggressive financial evolution is useful for creating national economic power, and somehow it is completely failing to heal the underlying wounds of the people who drive it. We live in a time when modern salary structures, disposable corporate earnings, and multiple lines of credit should give us ultimate security. Yet, when we end up depending entirely on digital bank balances, algorithmic investment portfolios, and automated tax planning for our sense of peace, we don't know where we actually forgot the raw, emotional human cost of survival that our ancestors paid. We lost the old, authentic understanding of what money is actually supposed to do — provide freedom, not just a slightly more decorated cage. So this article basically is going to get you all aware about what we should do with our financial resources and what we should do with the heavy, unaddressed psychological baggage that we carry from our childhoods. It aims to tear down the wall of false responsibility and look closely at the deep seated financial trauma affecting millions within India's extensive middle class.

The Architecture of Middle-Class Scarcity

When we trace the lineage of the modern Indian middle-class worker, we find an architectural framework built entirely on hyper-vigilance. The historical memory of pre-liberalization India — characterized by rationing, license raj restrictions, structural job shortages, and severe economic fragility — is not something that evaporated when the markets opened in 1991. Instead, that ancestral memory was hardcoded into the child-rearing patterns of the generation that followed. Parents who survived on single government tenures or volatile agricultural income passed down a philosophy where saving money was not an analytical tool for asset allocation; it was an act of raw survival against a hostile, resource-scarce ecosystem. This mindset created a deep psychological blueprint that equates spending with immediate danger. If you grew up in a household where a sudden medical emergency meant breaking fixed deposits or pleading with relatives for personal loans, your brain learned a profound lesson: liquidity is the only barrier between your family and absolute ruin. When these children grow up to become software engineers, corporate lawyers, and product managers earning six-figure monthly salaries, the physical environment changes entirely, but the neural pathways remain stuck in 1984. They view every commercial transaction through a lens of existential panic, analyzing their ability to purchase basic comfort as if it might trigger structural insolvency.

"We think we are practicing financial prudence when we refuse to spend on comfort, but we are actually just honoring the ghosts of our family's economic hardships."

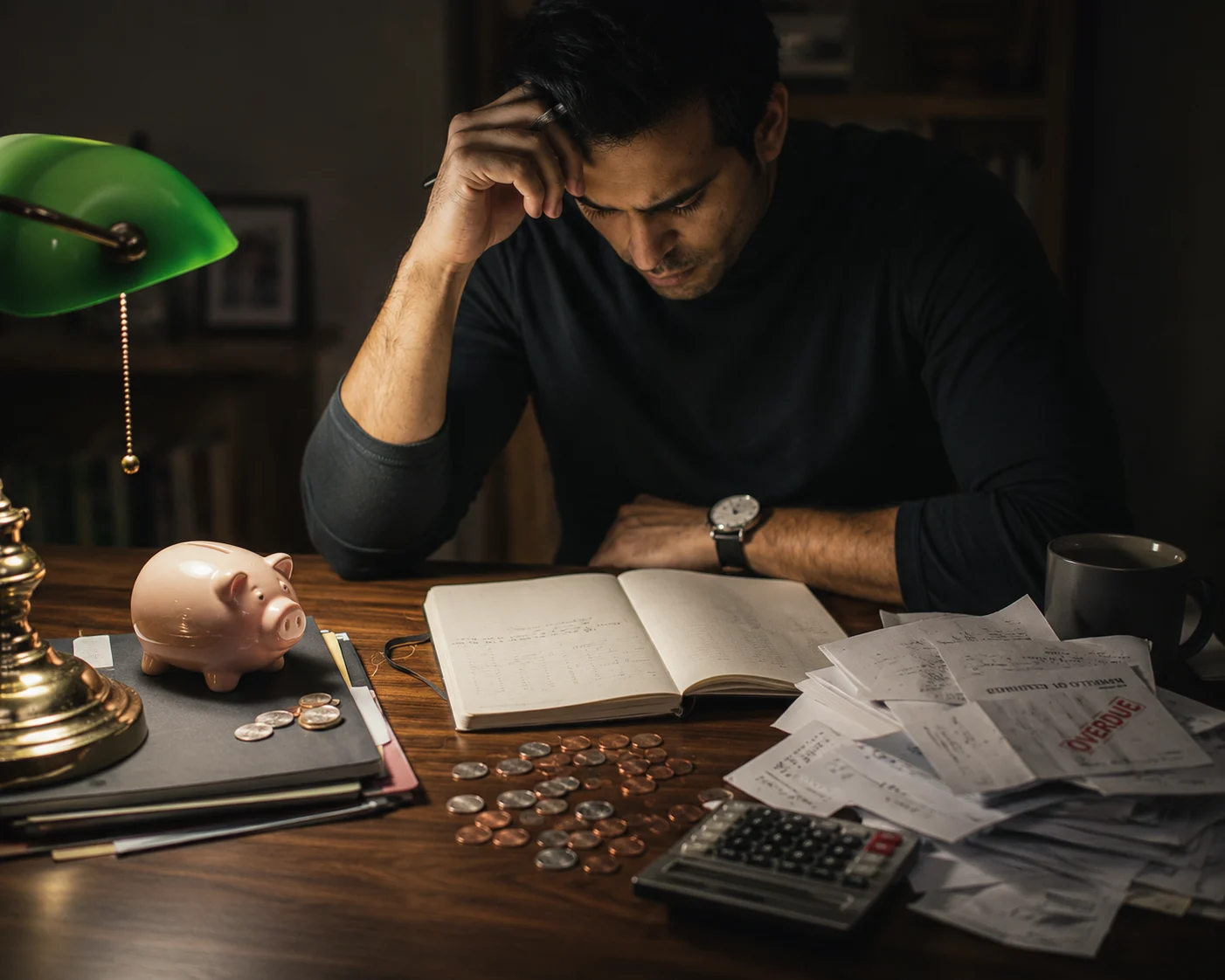

This reality is highly evident when we look closely at statistical consumption shifts. While credit card usage and consumer lending have grown exponentially, the internal experience of spending that money remains ridden with profound guilt. The average middle-class professional cannot purchase a high-end appliance or book an international flight without experiencing a somatic response — a tightening of the chest, a wave of immediate regret, or a subconscious drive to immediately "make up" for the expenditure by cutting down on fundamental daily needs like food or healthcare. This is not financial responsibility. This is structural anxiety wearing a well-tailored business suit.

KEY INSIGHTS: THE SCALE OF INDIAN SAVINGS & CREDIT PSYCHOLOGY

- The Household Wealth Paradox: Recent macroeconomic data reveals that despite rising per-capita incomes, Indian household net financial savings hit a multi-decade low of roughly 5.1% of GDP, driven by high post-pandemic real estate debt and inflationary cost pressures. Yet, the emotional drive to accumulate cash remains at an all-time high.

- The Credit Growth Trap: Unsecured personal loans and credit card outstanding amounts have grown at an aggregate rate exceeding 20% year-on-year, showing that middle-class consumers are structurally forced into debt to match lifestyle aspirations, exacerbating systemic financial anxiety.

- The Inherent Failure of Digital Enablers: Automated expense tracking applications report that over 72% of users manually override or review alerts multiple times a week, reflecting a deep-seated lack of trust in automated systems and a compulsive need to monitor micro-transactions.

The Core Symptoms: Financial Trauma in Disguise

In recent psychological studies focusing on emerging market demographics, it has been observed that major financial behaviors are dictated not by logical math, but by traumatic reenactment. A vast behavioral gap is seen where individuals act against their own long-term wealth building out of deep-seated fear. For example, every 3rd out of 5th investment choices made by middle-class Indians is fundamentally driven by capital preservation rather than inflation-adjusted growth. This calculation leaves a massive error in long-term wealth building, which, if not destructive in immediate daily household calculations, ensures that families lose significant purchasing power over a ten-year cycle, leaving them structurally vulnerable to high inflation.

Let us look systematically at the primary symptoms of this financial trauma, which are routinely praised as traditional virtues:

The Compulsive Hoarding of Safe Assets: Millions of modern professionals keep vast sums of capital locked in legacy fixed deposits, public provident funds (PPF), or unproductive traditional gold jewelry, earning returns that barely beat real inflation. When asked why they do not allocate funds to diversified equities or global mutual funds, the response is rarely based on structural financial logic. It is an emotional response. The tangible nature of a fixed deposit receipt or a gold biscuit provides a localized sense of safety that a volatile equity screen can never replicate. The fear of losing nominal capital overrides the absolute mathematical certainty that their money is slowly decaying in value.

The "Luxury Guilt" Cycle: Giving into consumer desires is followed by an immediate psychological penalty. When a financially traumatized individual spends money on a luxury — such as a fine-dining experience, a premium vehicle, or a wellness retreat — the initial dopamine spike is instantly replaced by an inner critical voice. This voice accuses them of being reckless, wasteful, and disrespectful to the struggle of their parents. To ease this internal friction, they enter an endless loop of hyper-frugality, logging every tiny transaction and obsessively cutting minor expenses to make up for the "sin" of spending. This turns daily life into a tiresome chore of constant microauditing, taking up massive mental energy and causing major psychological headaches and ongoing stress.

Advertisement

The Martyrdom of Self-Neglect: This is perhaps the most insidious manifestation of middle-class money wounds. It is the practice of delaying essential medical checkups, refusing psychological therapy, driving compromised vehicles with outdated safety features, or living in poorly insulated, uncomfortable housing, all under the guise of "saving money for the future." Individuals sacrifice their present physical health and mental stability to feed an imaginary future state of perfect security — a state that, due to the nature of trauma, never actually arrives. No matter how large the bank account grows, the internal threshold for safety is continuously pushed further away.

"True financial wealth is measured by the absence of financial anxiety, not by the height of an accumulated pile of capital that you are terrified to touch."

The Intergenerational Transmission of Debt and Guilt

The dynamic between Indian parents and their adult children is deeply entangled with transactional financial guilt. In many middle-class families, children are explicitly or implicitly raised to be the ultimate retirement plan. Because the previous generation lacked access to robust institutional pension structures, diversified financial products, or sovereign social security, they poured their entire life savings into two specific buckets: ancestral or residential real estate, and their children's higher education. While this represents a monumental sacrifice, it leaves a heavy, invisible debt on the shoulders of the next generation. When the adult child enters the modern workforce, their income is not entirely their own. It is psychologically mortgaged to the expectations, validation, and unfulfilled material dreams of their parents. They find themselves buying properties they do not want to live in, paying for elaborate social weddings they do not agree with, or maintaining massive emergency cash reserves for extended family networks, simply because the weight of the historical sacrifice is too heavy to put down. This creates an environment where personal financial planning becomes impossible. The individual cannot plan for their own early retirement, career transitions, or entrepreneurial ventures because they are completely tied down by the responsibility of stabilizing their entire family tree. This dynamic also creates a deep resentment that is rarely spoken about in open family discussions. The adult child resents being locked into high-stress, soul-crushing corporate jobs to service legacy expectations, while the parents feel anxious that any deviation from traditional financial paths will lead to immediate disaster. This friction turns every conversation about money within the household into an absolute minefield of emotional blackmail, tears, and defensive historical reminders of how "we survived on a fraction of your income."

Healing the Wounds: Moving from Survival to Sovereignty

To heal from generational financial trauma, we must realize that numbers alone cannot solve an emotional disorder. You can design the most efficient, hyper-automated financial spreadsheet in Google Sheets, link it to every bank API, and run predictive cash flow models, but if the hand typing the data is trembling with ancestral panic, the spreadsheet is entirely useless. We must move away from simple calculations and focus on reflection and deep emotional awareness. The first step toward true financial sovereignty is the explicit separation of historical family reality from your present physical environment. The economic danger that your family faced in the past was real, valid, and required brutal defensive mechanisms. However, your present environment — characterized by specialized skills, diverse asset classes, insurance protection, and consistent cash flows — does not require those same defensive measures.

Honoring your parents' sacrifices does not mean you must replicate their deprivation.

Secondly, we must redefine our definition of financial risk. The traumatized mind views volatility as an immediate precursor to poverty. The mature financial mind understands that the greatest risk is not short-term market corrections, but the long-term certainty of purchasing power loss through inflation and self-neglect. Spending capital on systemic therapy, physical healthcare, functional living spaces, and time-saving services is not an expense; it is a high-yield strategic investment in the preservation of your primary income-generating asset — yourself.

Finally, we must cultivate the habit of intentional, guilt-free spending. Just as traditional budgeting systems encourage setting strict limits on discretionary spending, individuals recovering from financial trauma need to set "minimum joy quotas." This means allocating a distinct, non-negotiable portion of monthly cash flow specifically for personal comfort, exploration, and lifestyle elevation, with the explicit psychological condition that this money must be spent, and that spending it is a sign of psychological recovery and financial maturity.

"Spend consciously on the things that enrich your human experience, and save intentionally to protect that experience from future vulnerability."

We must ultimately realize that money is nothing more than energy. It is an instrument designed to buy back your time, extend your choices, and bring peace to your daily existence. When we allow it to become an engine of perpetual anxiety, a source of toxic family guilt, or a metric for validation, we are not being responsible citizens or dutiful children. We are simply remaining financially traumatized, passing down the unmodified chains of economic scarcity to the generations that come after us. It is time to break the loop, heal the wound, and learn to live in the abundance we have worked so hard to build.

Read Further

- RBI Data: Household Net Financial Savings Fell to a Multi-Decade Low of 5.1% of GDP in FY23 — Business Standard

- Your Nani's Famine Lives Inside Your Body — How Inherited Scarcity Shapes the Modern Mind, OneMint

Disclaimer: All the data and behavioral insights provided above were compiled from public socioeconomic internet resources, consumer psychology reviews, and demographic studies on middle-class financial behaviors. This comprehensive analysis should not be taken as formal, legally binding investment, psychological, or financial advice.

Advertisement