In the highly dynamic Indian telecommunications industry, the line separating state intervention from market capitalism has increasingly blurred. Nowhere is this trend more pronounced than in the structural reality of Vodafone Idea Limited (Vi) in 2026. Once a premier private sector enterprise formed by the high-profile merger of Vodafone India and Idea Cellular, the company has gradually transformed into a quasi-state-backed entity. Following a series of massive debt-to-equity conversions culminating in April 2025, the Government of India solidified its position as the single largest shareholder, commanding a staggering 48.99% (effectively 49%) stake in the enterprise.

While equity injection and structural moratoria provided a temporary lifeline to preserve a three-private-player market structure, the stock market remains strangely complacent about a fundamental risk: the absolute absence of a defined government exit strategy. This massive holding behaves like a classical market overhang — a ticking technical and strategic time bomb that restricts capital appreciation, paralyzes transformative corporate decision-making, and deters deep-pocketed strategic international investors from making long-term commitments.

"A sovereign rescue without an institutional exit blueprint is merely a delayed restructuring. The market is pricing the survival, but ignoring the structural entrapment."

The Genesis of the Stake: How Debt Became Control

To fully grasp the magnitude of the market overhang in 2026, one must examine the legacy structural deficiencies that precipitated this unprecedented government holding. The conversion mechanism was rooted in the historic September 2021 Telecom Reforms and Support Package. This framework permitted cash-strapped telcos to convert the interest component arising from deferred Adjusted Gross Revenue (AGR) and spectrum installment liabilities into equity shares.

Initially, this manifested in February 2023 when the Ministry of Communications converted approximately ₹16,130 crore of outstanding interest dues into a 22.6% equity stake. Far from solving the systemic undercapitalization, the company's fiscal position continued to deteriorate under a mounting wall of statutory debt. By early 2025, with deferred spectrum auction dues compounding relentlessly, the Union Government enacted a second, much larger conversion. It injected an additional ₹36,950 crore by absorbing 3,695 crore equity shares priced at a face value of ₹10 per share, scaling the sovereign holding to its present 48.99% ceiling.

| Timeline / Milestones | Government Stake (%) | Statutory Debt Owed (Approx.) | Primary Operational Focus |

|---|---|---|---|

| Pre-September 2021 Reforms | 0.00% | ₹1,80,000 Cr | Survival & Core Network Maintenance |

| February 2023 (First Conversion) | 22.60% | ₹2,01,000 Cr | Stabilizing 4G Footprint |

| April 2025 (Second Massive Conversion) | 48.99% | ₹2,17,000 Cr | Commercial Viability & 5G Vendor Deals |

| Current Fiscal Year 2026 | 48.99% | ₹1,64,000 Cr (Post-AGR Reduction) | Consortium Debt Refinancing & CapEx |

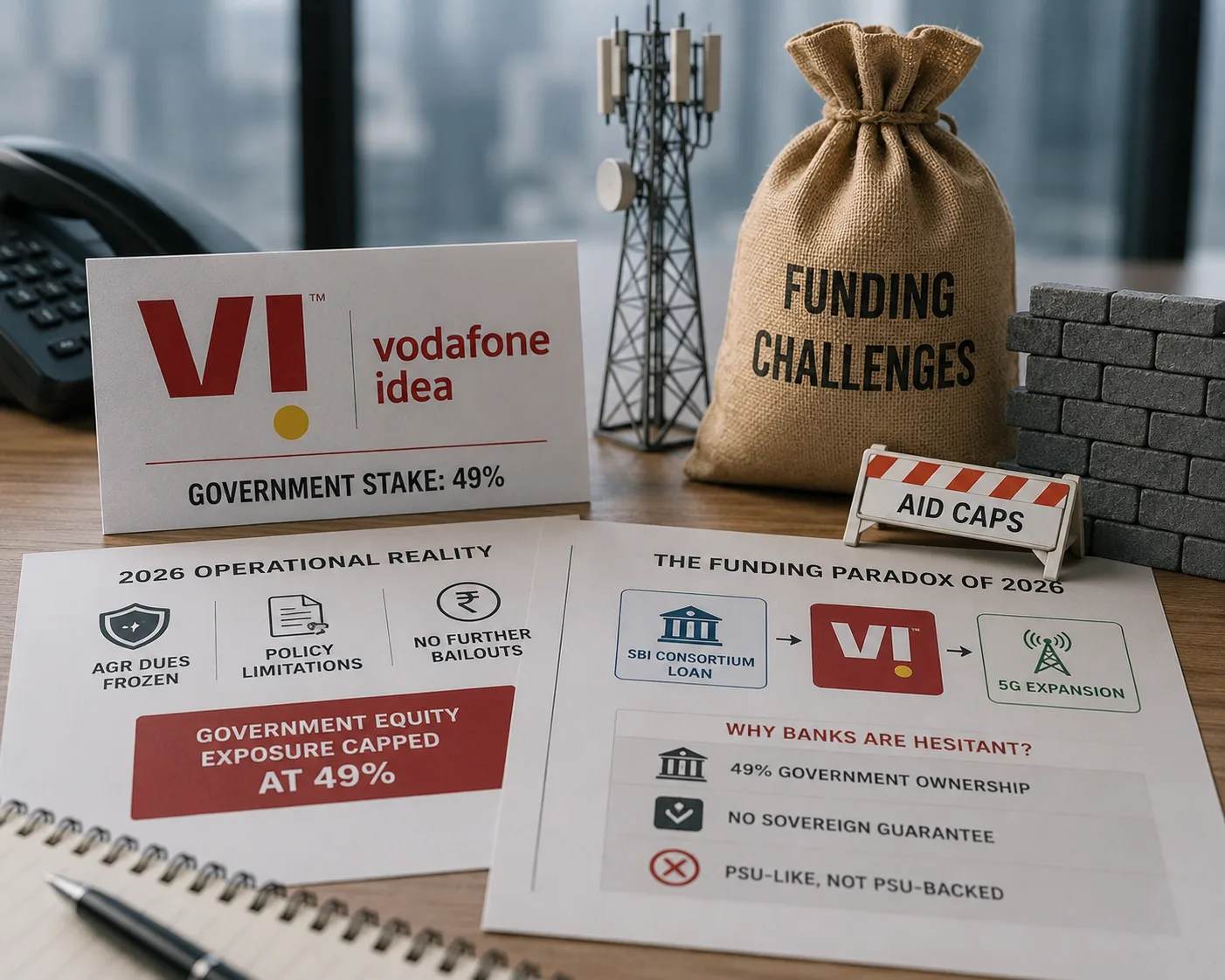

The 2026 Operational Reality: Aid Caps and Financial Walls

Entering 2026, the structural landscape shifted following the landmark late-2025 Union Cabinet decision, which froze Vodafone Idea's Adjusted Gross Revenue (AGR) dues and rationalized its immediate obligations, cutting its long-standing legal liability down from ₹87,695 crore to approximately ₹64,046 crore ($6.75 billion). This provided essential breathing space and generated speculative optimism among retail market participants. However, the operational reality remains constrained by clear policy limitations.

The Ministry of Communications, led by Telecom Minister Jyotiraditya Scindia, has formally capped the government's equity exposure at the current 49% mark. The administration has explicitly ruled out further fiscal bailouts or incremental debt conversions, declaring that the company must independently navigate its path toward market recovery. This hard cap presents a fundamental challenge: Vodafone Idea is locked in an intensive capital expenditure battle against Reliance Jio and Bharti Airtel, yet its largest shareholder has closed its capital wallet.

The Funding Paradox of 2026

While Vodafone Idea attempts to negotiate an essential ₹35,000 crore ($3.7 billion) consortium loan led by the State Bank of India (SBI) — comprising ₹25,000 crore in term funding and ₹10,000 crore in non-funded facilities — commercial banks remain hesitant. Lenders view the 49% government ownership as an ambiguous structural paradox: the company possesses the heavy bureaucratic footprint of a Public Sector Undertaking (PSU) without any of the associated sovereign credit guarantees or direct fiscal backing. This compares directly to the structural governance ambiguities visible across other Reliance-ecosystem entities, as analyzed in our examination of Jio's 77% Reliance Retail Revenue Dependency and the Governance Risk Minority Shareholders Cannot Price.

Deconstructing the Market Overhang

In equity research, a "market overhang" describes a situation where a massive block of shares is held by a single entity that must eventually liquidate its position, creating a persistent cap on share price appreciation. In Vodafone Idea's case, the overhang is multifaceted and poses a unique challenge to retail and institutional investors alike:

A. The Profitability Yardstick vs. Market Liquidity

The government's internal guidelines state that any eventual divestment of its 49% stake must be executed at a financial profit, utilizing the initial conversion price of ₹10 per share as a baseline floor. Because the market price frequently fluctuates below or near this threshold due to continuous operational deficits and subscriber losses, a standard secondary market block sale remains unviable. If the state attempts to liquidate a portion of its holding on the open market, it risks triggering an immediate collapse in share value, wiping out institutional capital.

B. Disincentivizing Foreign Direct Investment (FDI)

Global telecom operators and institutional private equity firms operate on models requiring clear paths to absolute corporate control and agile governance. With the Indian state maintaining a near-majority 49% stake, any external investor faces a structural bottleneck. Even though original promoters Vodafone PLC (holding roughly 19%) and the Aditya Birla Group retain operational management, their equity control has been diluted. Prospective buyers are reluctant to invest billions into a company where a government ministry acts as an unpredictable partner with ultimate voting weight.

"No global telecom conglomerate or sovereign wealth fund will inject Tier-1 equity capital into an asset where the state controls 49% of the equity votes but disclaims all operational liabilities."

The Strategic Dilemmas of a Sovereign Exit

The core issue of the 2026 telecom landscape is that every potential exit pathway for the government is blocked by significant economic or political hurdles:

1. The Strategic Private Sale Route: The most rational exit strategy involves selling the entire 49% block to a major domestic conglomerate or a foreign consortium. However, this approach requires navigating intense domestic political scrutiny regarding the perceived underpricing of public assets, alongside strict regulatory reviews by the Securities and Exchange Board of India (SEBI) concerning minimum public shareholding mandates.

2. The Treasury Share Transfer Alternative: Recent market discussions indicate that Vodafone Group PLC has explored transferring a portion of its 19% holding into the Indian entity as treasury shares to bolster capital. While this mechanism assists short-term liquidity, it fails to address the state's large equity position, leaving the underlying overhang unresolved.

3. Institutional Inaction: The most likely scenario is long-term bureaucratic inertia. The state may choose to hold its 49% position indefinitely, absorbing equity losses while prioritizing market stability over capital efficiency. This dynamic leaves Vodafone Idea permanently positioned between a private commercial business and a state-supported utility.

Conclusion: The Market's Cost of Complacency

The market's current valuation of Vodafone Idea appears to overlook the structural complexities of its ownership. Investors have responded positively to near-term positives, including the 2025 statutory dues reduction, tariff hikes, and ongoing credit negotiations with the State Bank of India. However, the long-term outlook remains limited by the government's unhedged 49% stake.

Until the government establishes a clear, transparent institutional framework for its exit — whether through a phased institutional block trade, a targeted buyback mechanism, or a structured strategic divestment to a global operator — Vodafone Idea will likely face structural headwinds. The state's intervention successfully prevented a market duopoly in 2021, but without an exit strategy, that rescue mechanism now limits the company's long-term commercial potential.

Read Further

- How Vodafone Idea Will Service Its ₹2 Trillion AGR and Spectrum Dues After Government's Relief — Outlook Business, January 2026

- Vodafone Idea Plans ₹35,000 Crore Fundraise, SBI-Led Banks Likely to Back Deal — TechStory, May 2026

- Government Increases Stake in Vodafone Idea: Equity Conversion & AGR Dues — Vajiram & Ravi Current Affairs, April 2025

Disclaimer: All financial data, structural details, and market analyses provided above are compiled from publicly available internet resources, corporate disclosures, and policy studies. This analytical piece is for educational and informational purposes only and must not be construed as statutory market guidance, investment advice, or an institutional quote from our platform.