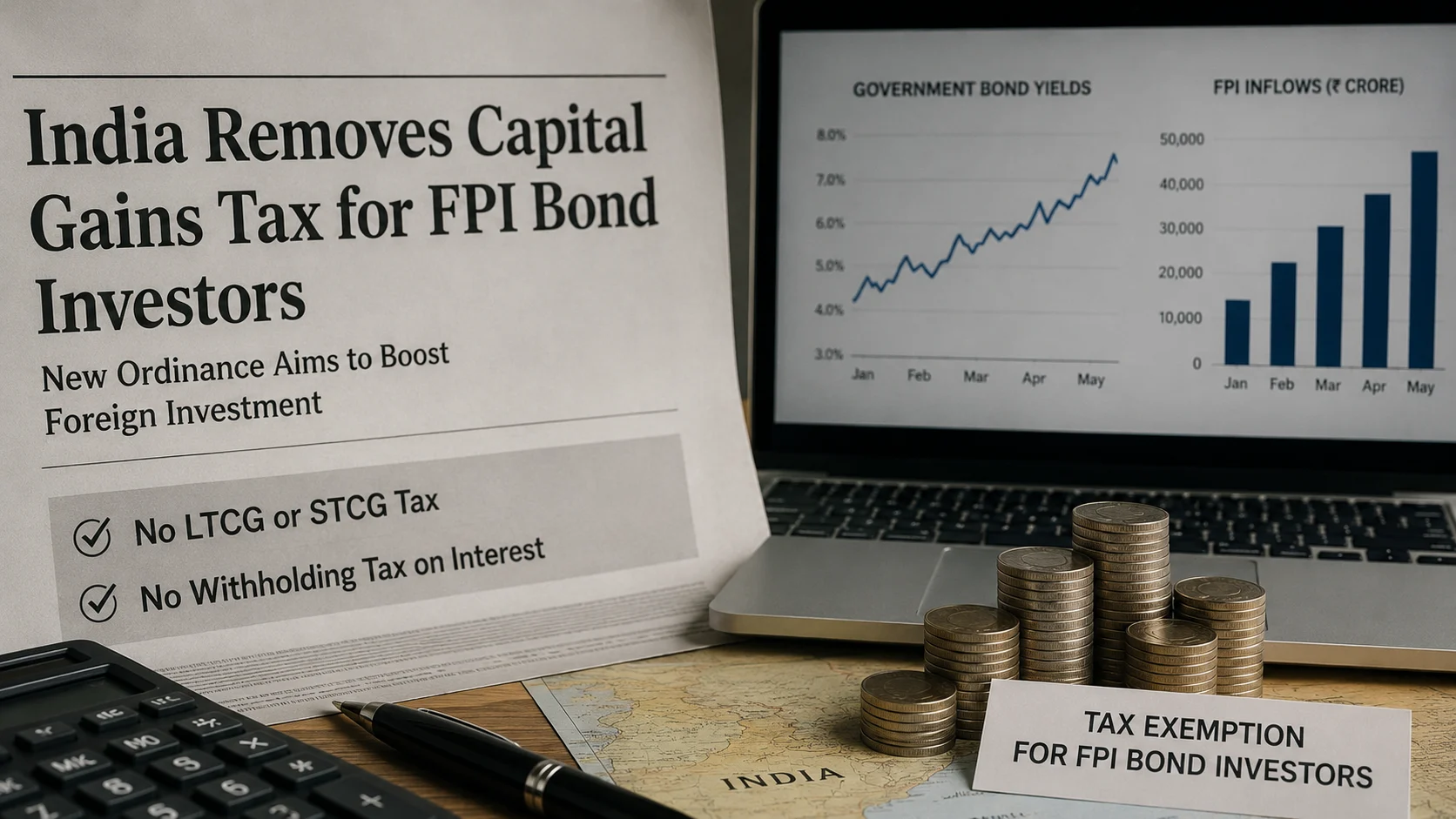

The global macro environment has become incredibly crowded lately, with emerging markets practically tripping over each other to attract specialized liquidity. In this scramble for capital, it is getting harder to tell whether governments are making frantic, reactive moves or following a deliberate strategic script. India just provided a massive case study for this on June 4 and 5, 2026. The government shifted its entire approach by issuing a presidential ordinance to amend the Income Tax Act, essentially cutting through years of complaints from foreign investors who felt that the existing tax structures were just too much friction for their liking.

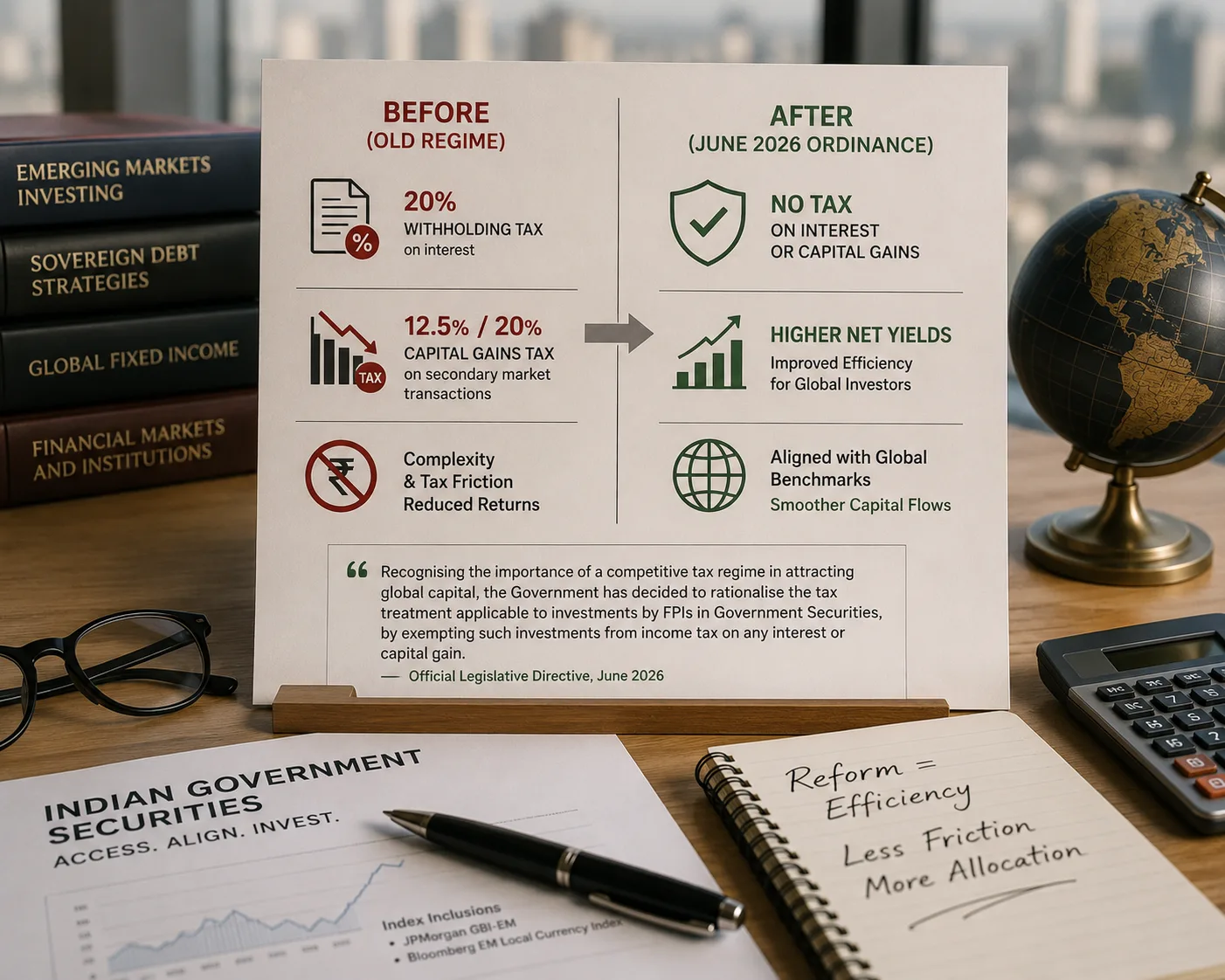

This new Income-tax (Amendment) Ordinance is a heavy hitter. The Union Cabinet decided to completely wipe out the 12.5% long-term capital gains tax and the 20% short-term capital gains tax for Foreign Portfolio Investors holding central government securities. On top of that, they removed the 20% withholding tax on interest income. Because this is retroactive to April 1, 2026, Indian sovereign bonds have suddenly become some of the most tax-efficient fixed-income assets you can find anywhere in the world. However, the sheer speed of this move is jarring. Usually, such massive changes come with budgetary projections and a lot of debate, but here we have a significant institutional void. There is no official statement on what this is going to cost the treasury, effectively creating a subsidy worth thousands of crores that is currently sitting outside the usual parliamentary oversight.

From a market perspective, you can see why they did it. This moves India toward becoming a highly competitive destination for sovereign debt allocations. By removing these taxes, the government has basically eliminated the "index drag" that happens when domestic yields don't match up with gross index calculations used by big names like JPMorgan or Bloomberg. It also acts as a cushion for the Rupee; if you have a steady flow of dedicated debt capital coming in, it helps insulate the local currency from whatever the Federal Reserve decides to do with interest rates. For the foreign investors themselves, the math is simple and attractive. Their actual returns have jumped from around 5.5% to somewhere between 6.9% and 7.1% almost overnight.

But there is a flip side to this that is harder to ignore if you care about fiscal transparency. We are looking at a total lack of public disclosure regarding how much tax revenue is being sacrificed. Because this was handled through a quick Cabinet Ordinance instead of the standard Union Budget process, there was no real floor debate in Parliament. It also feels like a bit of a regressive model. The government is essentially subsidizing large foreign institutional funds while domestic retail investors — the regular people buying bonds at home — aren't getting any similar relief. While the government stays quiet on the numbers, private institutional estimates are already floating around, suggesting that this could cost taxpayers up to ₹6,000 crore annually — money that is being given up entirely off the books.

Autonomous Market Realities and the Efficiency It Provides

The new June 2026 framework has fundamentally changed how sovereign bond investing works, moving it away from a messy, tax-heavy process into something much more streamlined for global asset managers. If you look back at how things used to be, any offshore manager trying to get into the Indian debt market had to deal with a double layer of tax complications that made every move a headache. For starters, those semi-annual interest payments on traditional or Fully Accessible Route securities were hit with a flat 20% withholding tax right at the source. Unless you had a specific bilateral tax treaty to fall back on, that money was just gone before it even hit the account. Then there was the secondary market side of things. If a manager wanted to optimize their trade or play the yield curve, they were looking at a 12.5% long-term capital gains tax for holdings over a year, or a 20% tax if they decided to sell sooner. It was a lot of math just to figure out if a trade was actually worth the effort.

Everything changed with the 2026 Ordinance. By cleaning up these structural layers, the new rules have essentially removed the manual processing hurdles that used to slow everything down. Now, institutional systems can look at gross yields and treat them as net yields without worrying about hidden tax bites. This removes the frictional drag that used to make investors hesitate. It is a massive shift, especially when you consider that Indian sovereign debt is being added to major global benchmarks like the JPMorgan Government Bond Index-Emerging Markets and the Bloomberg Emerging Market Local Currency Index.

This matters because the big index-tracking funds operate on automation. They try to mirror these indices under the assumption that there is zero tax friction involved. Before this reform, the withholding taxes in India were causing constant tracking errors, which basically penalized passive funds for holding Indian bonds and gave them a reason to avoid an overweight position. The 2026 reform fixes this mechanical misalignment. It brings the market into immediate compliance with global benchmarking standards, allowing capital to flow in much more freely without the old tax-related roadblocks getting in the way.

"Recognising the importance of a competitive tax regime in attracting global capital, the Government has decided to rationalise the tax treatment applicable to investments by FPIs in Government Securities, by exempting such investments from income tax on any interest or capital gain." — Official Legislative Directive, June 2026

The Hidden Cost: Cons of a No-Estimate Fiscal Subsidy

The recent move to scrap taxes for international investors has sparked quite a bit of celebration in the markets, but there is a much quieter and more technical conversation happening among public finance experts that we should probably pay attention to. The main issue they are raising is not just about the policy itself, but about the total lack of a published revenue foregone statement. In the world of government accounting, when you give a specific group a tax break, you are essentially giving them a subsidy. It just happens to be an implicit one. By choosing not to collect these taxes from international investors, the state is doing something economically identical to collecting the money and then writing those same investors a check for the same amount. The difference is that one shows up on the books as a cost, while the other just disappears from the ledger entirely.

This creates a serious gap in fiscal accountability. Usually, when a big policy change like this happens, there is a clear estimate of what it will cost the taxpayer. Because the 2026 Ordinance was pushed through outside of the normal legislative schedule, we never got an official projection of how much revenue the government is actually giving up. To get a sense of the scale here, we have to look at the numbers ourselves. Foreign Portfolio Investors currently hold about ₹3,80,487 crore in Indian sovereign debt. That represents roughly 3.34% of the total ₹112.42 lakh crore in outstanding central government securities. When you run the math on the yields for these specific assets, the size of this unmonitored sacrifice starts to look very significant.

From the investor's perspective, this is a massive win for yield optimization. It moves their actual net returns from around 5.5% to a much cleaner range of 6.9% to 7.1% almost overnight. This jump is intended to help manage reserve volatility by drawing in more dedicated debt inflows, but it happens while domestic retail bond participants are left without any similar relief. Some private institutional estimates suggest that the annual sacrifice being made by the taxpayer could be as high as ₹6,000 crore, all of which is currently being kept off the official budget.

When you break down the tax parameters before and after this ordinance, the numbers are stark:

| Tax Component | Pre-Ordinance Rate | Post-Ordinance Rate | Estimated Annual Revenue Foregone |

|---|---|---|---|

| Withholding Tax on Interest Income | 20% | 0% | ₹4,000 – ₹5,000 crore |

| Long-Term Capital Gains Tax (12+ months) | 12.5% | 0% | ₹500 – ₹800 crore |

| Short-Term Capital Gains Tax | 20% | 0% | ₹200 – ₹400 crore |

| Total Combined Fiscal Subsidy | ₹4,700 – ₹6,200 crore annually |

Recent studies show that when major policy actions like this lack explicit cost estimates, they tend to create large tracking errors in national budgetary planning. We are effectively flying blind on the true cost of attracting this foreign capital. While the immediate market reaction is positive because the numbers look better for participants, the structural bypass of fiscal oversight remains a concern for anyone looking at the long-term health of public finance. The lack of a transparent report means we are trading away a massive amount of potential tax revenue to stabilize debt inflows without a clear public accounting of whether the trade is actually worth it.

The Mechanics of the Index Fund Effect

To really get why the government felt like they had to hand out such a massive, uncalculated subsidy, you have to look at the rigid way global index tracking actually works. We aren't talking about human fund managers making gut calls here. Most modern investment follows passive mandates that rely on automated rebalancing. When a country gets included in something like the JPMorgan GBI-EM index, it triggers billions of dollars in inflows through non-discretionary purchase models. These systems don't think; they just buy based on the math.

The math driving these flows is incredibly sensitive to what an investor actually takes home after all the layers of costs are peeled away. You can look at it through a simple formula where the net yield equals the raw coupon rate of the bond multiplied by what's left after withholding taxes, minus whatever value is lost to currency depreciation. By early 2026, things were looking rough. Foreign institutional investors were dumping domestic equities at a staggering rate, selling off more than ₹2.5 lakh crore. This put a massive amount of pressure on the Rupee. As the currency started to slide, keeping the withholding tax at 20% meant the net return for foreign investors was falling off a cliff. Suddenly, Indian bonds didn't look nearly as attractive as options in Brazil, Indonesia, or South Africa.

By making the move to completely scrap withholding taxes and capital gains taxes, the government essentially forced the tax variable in that equation down to zero. Overnight, they turned a 6.9% gross yield into a 6.9% net return. It was a calculated adjustment designed to offset the hit investors were taking from the falling Rupee. The goal was to build a structural defense for the exchange rate. Instead of having the Reserve Bank of India jump into the market and burn through its hard-earned foreign exchange reserves to prop up the currency, the government decided to use the tax code as a shield.

It comes down to a trade-off in priorities. The logic seems to be that while you should spend consciously on building domestic infrastructure, you have to be intentional about cutting out the friction that foreign taxes create if you want to keep the lights on. The 2026 Ordinance is effectively a massive transfer of potential tax revenue straight into the pockets of international capital pools. It is an aggressive, perhaps even desperate, attempt to buy stability for local currency debt by making sure the math for global investors always stays in the green, regardless of how much the Rupee fluctuates.

"Spend consciously on domestic infrastructure, but save intentionally on foreign tax friction. The 2026 Ordinance represents an aggressive transfer of fiscal revenue to international capital pools to establish local currency debt stability."

Structural Disparities and Public Policy Oversight

There is something fundamentally strange about the current policy direction that feels like a massive contradiction in terms of public fairness. When you look at how the tax system treats different groups of people, you see a glaring gap that is hard to ignore. If you are a domestic retail investor living in India, or even a local company trying to grow, you are essentially paying the full price for your investments. Your interest income gets hit with whatever tax slab you fall into, often at the highest rates. If you choose to invest in debt mutual funds or buy market bonds directly, you are still facing the standard capital gains taxation rules. You are playing by the rules and paying into the national system as expected.

Now, look at the other side of the fence where the offshore institutional funds operate. Because of the 2026 amendment, we have ended up with a situation that is anything but balanced. An offshore fund can come in and buy the exact same government securities that a local individual or a domestic company does, yet they walk away with zero tax liability. It is a completely different world for them. One group is shouldering a significant tax burden for supporting the same national debt that another group gets to profit from entirely tax-free. This is not just a minor difference in rates or a small incentive. It is a total exemption for the outsider and a heavy bill for the local participant, even though they are both holding the same assets.

The issue goes even deeper than just the lopsided tax rates. Usually, when the government decides to spend money or provide a financial subsidy, there is a clear paper trail that the public can follow. You can typically find these things listed in the annual receipt budget or under the official sections for Demands for Grants. Those documents are the primary tools that allow the Comptroller and Auditor General, or the CAG, to do their job and perform a proper public audit. However, this specific tax break for foreign funds acts as a sort of hidden subsidy. It does not show up as a formal line item in those records. Because it stays off the main books in that way, it effectively avoids the kind of rigorous oversight and public scrutiny we usually expect for such significant financial decisions.

This lack of transparency makes it very difficult for anyone to see the real trade-offs being made behind the scenes. India obviously needs to fund its national fiscal deficit, and drawing in foreign portfolio capital is a very effective way to do that quickly. By making these FAR bonds so attractive to outsiders through tax exemptions, the government successfully brought in over ₹16,567 crore in a very short period. That is a massive amount of capital flowing into the country. But by bypassing the traditional checks and balances of a public audit, we are losing sight of the long-term cost. We are becoming increasingly reliant on foreign money to keep the national finances moving, while at the same time giving up a huge amount of potential tax revenue that never reaches the public treasury.

This brings us to a very difficult spot regarding the structural health of our financial system. The strategy worked in the sense that the money arrived, but the method used to get it here raises some serious concerns about what comes next. When you have this ongoing sacrifice of valuable tax revenue that could have been used for schools, roads, or healthcare, and you combine it with a lack of direct public accountability, you have to look at the bigger picture. We really have to ask if this way of managing the deficit is actually sustainable in the long run without more transparency.

Read Further

- Government Issues Ordinance to Exempt FIIs from Capital Gains Tax on Government Securities — ANI, June 5, 2026

- FPI Investments in G-Secs Become Tax-Free Under Income-tax (Amendment) Ordinance, 2026 — Ministry of Finance Official Statement via CAClubIndia, June 2026

- Government Issues Ordinance Exempting Foreign Investments in G-Secs from Capital Gains Tax: What Does It Mean? — India TV News, June 2026

Disclaimer: All financial data, structural details, and market analyses provided above are compiled from publicly available internet resources, official gazette notifications, and policy studies. This analytical piece is for educational and informational purposes only and must not be construed as statutory tax advice, investment guidance, or an institutional quote from our platform.