In the intense world of Indian corporate history, numbers can act as both a shield and an illusion. In May 2026, the domestic telecom sector experienced a jolt when Vodafone Idea Limited (VIL) reported a remarkable consolidated net profit of ₹51,970 crore for the last quarter of the fiscal year 2025-26. For a company weighed down by debt and facing net losses for nearly six years, this impressive profit announcement sparked celebrations, market rallies, and hopeful stories of a complete turnaround.

However, a massive accounting adjustment can hide serious operational issues; temporary improvements on the balance sheet don't mean sustainable cash generation. When we take a closer look at this record ₹51,970 crore quarterly profit, we see a very different economic picture. This profit surge was driven entirely by a significant non-cash item: a major reduction in statutory liabilities due to the Department of Telecommunications' (DoT) reassessment of Adjusted Gross Revenue (AGR) dues. Without factoring in these revisions, Vodafone Idea's actual operational metrics showed continued financial struggles. The operational reality for the quarter was a net pre-exceptional loss of around ₹5,515 crore, while the total core loss for the full fiscal year 2026 was a troubling ₹24,059 crore. This ongoing operational gap highlights a key issue in viewing Vodafone Idea's recent legal breakthroughs as a complete win. While the accounting changes provided a temporary boost to the balance sheet, the company's fundamental operations remain highly cash-consuming and limited. It continues to work in a capital-heavy industry where leading players have already developed strong 5G network advantages, leaving Vi stuck in a cycle of trying to catch up with a severely drained treasury.

"A massive accounting adjustment can mask severe operational bleeding; temporary balance sheet expansions are not identical to sustainable operational cash generation."

The Anatomy of the AGR Relief: What Actually Transpired in Early 2026?

To understand how Vodafone Idea survived its financial crisis, you have to look at the legal and government decisions made in early 2026. After the Supreme Court allowed for a review of old debts in late 2025, the Department of Telecommunications recalculated what the company owed. On April 30, 2026, the government cut Vodafone Idea's historical debt by about 27 percent, bringing it down from ₹87,695 crore to ₹64,046 crore.

The government also changed the payment schedule so the company wouldn't go bankrupt immediately. Instead of demanding the full amount upfront, they set up a long-term plan. From March 2026 until 2031, Vodafone Idea only has to pay a small amount of up to ₹124 crore each year. After that, between 2032 and 2035, they will pay at least ₹100 crore annually. The bulk of the ₹64,046 crore will then be paid off in six equal parts between 2036 and 2041.

This extra time saved the company from collapsing. Without this intervention, Vodafone Idea would have owed ₹18,000 crore by March 2026 — impossible to pay because the company only generates between ₹8,400 crore and ₹9,200 crore in cash each year. At the same time, the Bombay High Court dropped another ₹23,600 crore in spectrum charges, giving both Vodafone Idea and Airtel even more financial relief.

| Key Reassessment Framework | |

|---|---|

| Original AGR Claim Assessment | ₹87,695 crore |

| Reassessed and Corrected AGR Claim | ₹64,046 crore |

| Absolute Liability Reduction | ₹23,649 crore |

| Sovereign Equity Conversion | ₹36,950 crore of deferred dues converted into equity shares, raising the Government of India's direct ownership to 48.99% |

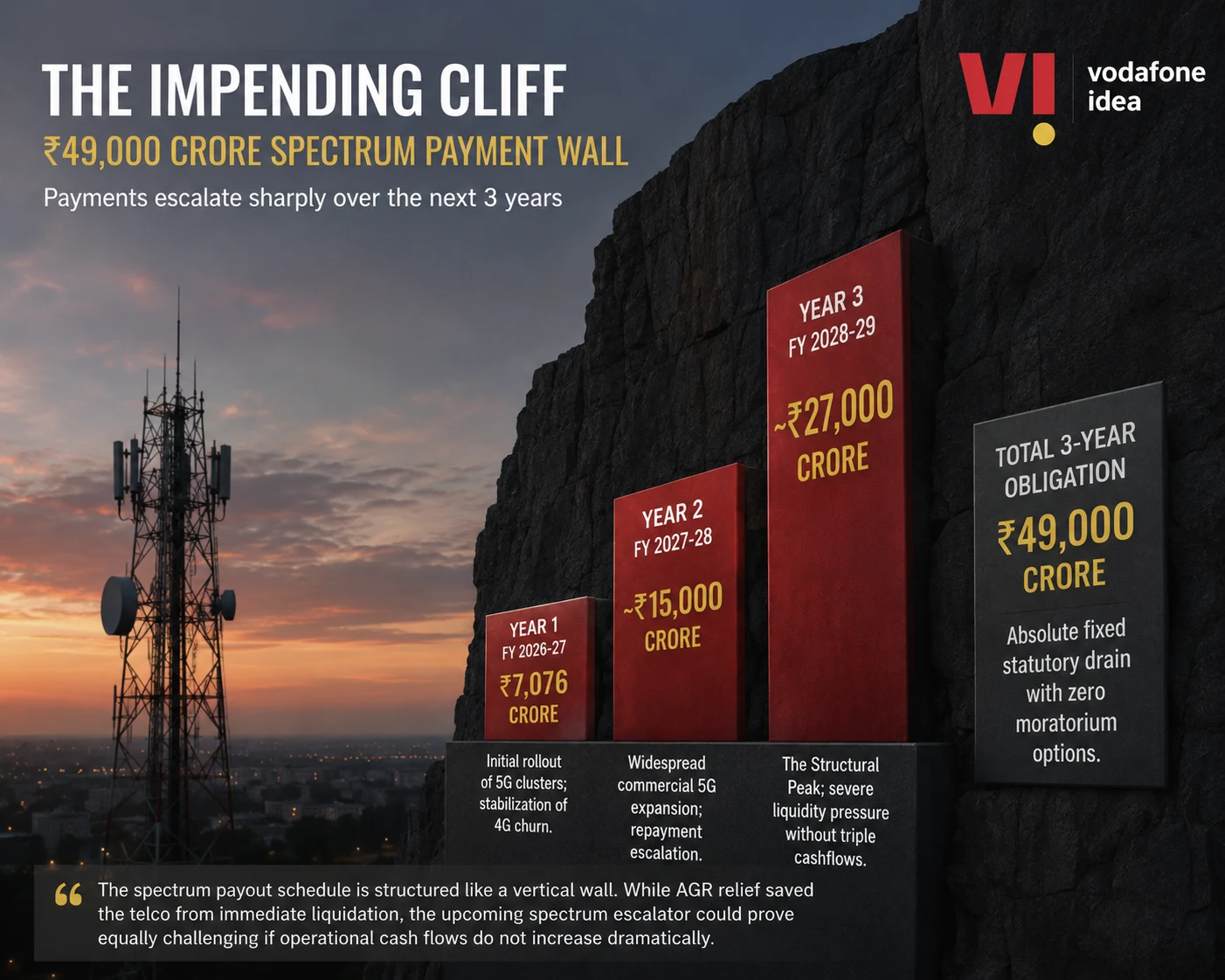

The Impending Cliff: The ₹49,000 Crore Spectrum Payment Wall

Most people are focused on the long-term AGR debt that has been pushed back, but there is a much more immediate problem coming up. The company has to pay ₹49,000 crore in spectrum fees over the next three years. Unlike the AGR dues, these payments haven't been delayed and the schedule is fixed. Analysts have pointed out that these costs are heavily back-ended, meaning they get much more expensive as time goes on. In the first year, the payment is ₹7,076 crore, which takes up almost all the cash the company normally brings in. By the third year, the payment jumps to ₹27,000 crore — nearly three times the most cash the company has ever generated in its best year. They have to pay the government this amount before they can even cover basic operating costs like employee salaries, power bills, or network maintenance.

| Fiscal Repayment Period | Estimated Annual Spectrum Outflow | Primary Strategic Objective & Headwind |

|---|---|---|

| Year 1 (FY 2026–27) | ₹7,076 crore | Initial rollout of 5G clusters; stabilization of 4G churn |

| Year 2 (FY 2027–28) | ~₹15,000 crore | Widespread commercial 5G expansion; repayment escalation |

| Year 3 (FY 2028–29) | ~₹27,000 crore | The Structural Peak; severe liquidity pressure without triple cashflows |

| Total 3-Year Spectrum Obligation | ₹49,000 crore | Absolute fixed statutory drain with zero moratorium options |

"The spectrum payout schedule is structured like a vertical wall. While AGR relief saved the telco from immediate liquidation, the upcoming spectrum escalator could prove equally challenging if operational cash flows do not increase dramatically."

The ₹1 Lakh Crore Capital Conundrum: Breaking Down the Management's 3-Year Target

Most people are focusing on the delayed AGR debt, but there is a much more urgent financial problem coming up soon. The company has to pay ₹49,000 crore in deferred spectrum fees over the next three years. While the AGR payments were pushed back by more than a decade, the schedule for these spectrum payments is fixed and has not changed. Analysts and bank reports show that this ₹49,000 crore debt is not spread out evenly. Instead, the payments get much heavier toward the end, creating a massive cash flow problem just as the company is trying to grow its business.

In the first year, the ₹7,076 crore payment will use up almost all the cash the company usually makes from its operations. By the third year, that annual payment jumps to ₹27,000 crore. This means that in just one year, Vodafone Idea will have to pay the government about three times more than its best historical cash flow — before they can even cover basic costs like employee salaries, network repairs, electricity, or marketing.

1. Network Infrastructure and Capex Expansion (₹45,000 crore): For years, Vi has underspent on its network relative to its peers. While competitors deployed hundreds of thousands of 5G base stations and achieved nationwide coverage, Vi was forced to ration its capital, resulting in consistent subscriber losses. The targeted ₹45,000 crore capex is crucial to expand 4G capacity, roll out competitive 5G networks in key industrial circles, and stop the ongoing erosion of its post-paid and premium user base.

2. Spectrum Liability Service (₹49,000 crore): As analyzed in the previous section, this represents the non-negotiable statutory payments required to retain the company's essential operating licenses and wireless frequencies.

3. Commercial Bank Debt Amortization (₹5,000 – ₹6,000 crore): While the company has worked to reduce its exposure to domestic banking syndicates, it still faces near-term maturities and debt-servicing obligations on its remaining bank loans that must be paid to avoid cross-default triggers.

To accumulate this ₹1 lakh crore pool, the management is relying on a combination of internal operational improvements and external funding injections. The strategy relies on a planned tripling of internal cash flows through tariff hikes and premium user growth, new long-term bank financing packages, potential tax refunds from historical disputes, and direct capital injections from its primary promoters, the Aditya Birla Group and the Vodafone Group.

The Sovereign Ceiling: Why the 49% Government Cap Changes Everything

While everyone is focused on the delay in old AGR debts, a much bigger and more immediate financial problem is coming up. The company owes ₹49,000 crore in deferred spectrum payments that must be paid over the next three years. Unlike the AGR dues, which were pushed back for over a decade, the government has not changed the schedule for these spectrum installments at all. For the full strategic context of what this sovereign ownership ceiling means for Vodafone Idea's long-term commercial independence, see our detailed analysis of The Government's 49% Stake in Vodafone Idea Has No Exit Strategy.

The math behind this schedule is very difficult for the company to handle. In the first year, the ₹7,076 crore payment will use up almost all the cash the company usually makes from its operations. By the third year, the yearly payment jumps to ₹27,000 crore. This means that in just one year, Vodafone Idea will have to pay the government three times more than its best historical cash flow — and this has to be paid before they can even cover basic costs like employee salaries, network repairs, electricity, or marketing.

"The state has explicitly positioned itself as an investor of public interest, not an operational guarantor or a source of endless financial bailouts."

Financing the Struggle: The SBI Consortium and the Execution Risks

Since the government is not offering more bailouts and the promoters are short on cash, Vodafone Idea has to rely on bank loans. The company is currently in talks with a group of banks led by the State Bank of India to get ₹35,000 crore. This money is split into two parts: ₹25,000 crore to pay for network equipment and ₹10,000 crore to cover bank guarantees and credit lines.

Binding Capital Commitments from Promoters: Banks require the core promoters to inject fresh equity alongside any new bank debt, ensuring they maintain significant skin in the game. While the Aditya Birla Group committed an initial ₹4,730 crore, lenders are pushing for further structural capital commitments.

Sustained Operational Performance Metrics: Funding tranches are directly tied to meeting specific operational goals, such as arresting subscriber losses and demonstrating consistent growth in average revenue per user (ARPU).

Escrow and Asset-Charging Structures: Banks require strict control over cash flows through dedicated escrow accounts, prioritizing bank debt servicing over other non-statutory expenses.

However, getting this money is not a sure thing. Indian banks are nervous because they have dealt with many bad loans in the telecom industry before. They are demanding clear proof that the company can actually survive and stay profitable before they hand over any cash. The biggest risk right now is timing. If the banks take too long with their checks and negotiations, the company will have to put its expansion plans on hold. If the network does not improve, more customers will leave for other providers. This would make the company's financial situation even worse, which in turn makes the banks even more hesitant to provide the funding. Breaking out of this cycle is the biggest challenge the management faces over the next year.

Operational Performance vs. Financial Liabilities: The ARPU Paradox

A company's financial survival really comes down to how well it operates day to day. In this regard, Vodafone Idea is showing some signs of stability. By the fourth quarter of FY26, the company's average revenue per user, or ARPU, rose to ₹190, up from ₹175 during the same period the year before. This 8.3 percent increase happened because more customers moved from 2G to 4G services. Vi's growth in this area actually outpaced its larger competitors, Reliance Jio and Bharti Airtel, who both saw their ARPU numbers stay mostly flat during that same quarter. Also, after years of losing subscribers, Vi finally started seeing a positive trend in monthly active users in February 2026. This was helped by the expansion of their 4G network and the start of 5G rollouts in industrial parts of Punjab, including Ludhiana, Jalandhar, and Patiala.

The Operational Paradox (FY 2025–26 Data):

While an ARPU of ₹190 shows a solid operational recovery, industry analysts estimate that to comfortably service its long-term liabilities while funding its network expansion, the company needs to raise its ARPU beyond the ₹250 threshold. This creates a significant commercial paradox: Vi must raise tariffs to generate the cash required to build its network, but if it raises tariffs too aggressively before its network matches the quality of its competitors, it risks driving users away and accelerating subscriber losses.

Conclusion and Strategic Outlook: Can Vi Survive the Upcoming Cliff?

Vodafone Idea's situation in 2026 is a mix of government relief and looming debt. While the AGR relief package and recent court wins stopped the company from going bankrupt immediately, these are not permanent fixes. A huge ₹49,000 crore payment for spectrum is coming up soon, and it will be a major test for the company. To get through this, they need to do three main things: secure a ₹35,000 crore bank loan to expand their network, raise their prices so the average revenue per user reaches ₹250 without losing too many customers, and ensure their management stays focused without more regulatory trouble. The government has given them some breathing room, but ultimately, the company's survival depends on whether it can start generating enough actual cash from its own operations.

Read Further

- Vodafone Idea Posts ₹51,970 Crore Q4 Profit on AGR Dues Relief Boost — Business Standard, May 2026

- Vodafone Idea Posts PAT of ₹51,970 Crore in Q4 FY26 — Business Standard Capital Market News, May 2026

- Vodafone Idea Plans ₹35,000 Crore Fundraise, SBI-Led Banks Likely to Back Deal — TechStory, May 2026

Disclaimer: The analysis and financial metrics presented in this document are synthesized from public corporate filings, Department of Telecommunications updates, institutional research briefs, and broader macroeconomic studies. This report is intended for analytical and educational purposes only and does not constitute formal financial, investment, or legal advice.