In the architecture of modern personal finance, we are meticulously trained to account for known vectors of capital depletion: compounding student loan amortization, structural housing inflation, hyper-inflated childcare costs, and our own distant retirement targets. Yet, a silent, mathematically aggressive structural liability is gestating beneath the surface of millennial and Gen Z balance sheets. It does not appear on any credit report, it cannot be discharged through conventional structural refinancing, and it remains completely unaccounted for in traditional algorithmic wealth projections. It is the imminent financial insolvency of our aging parents.

For decades, the standard socio-economic contract assumed that each generation would attain self-sufficiency, building an independent nest egg to absorb the friction of their twilight years. The historical reality of the mid-to-late twentieth century largely validated this model, buoyed by robust corporate pension systems, reliable real wage appreciation, and predictable healthcare cost trajectories. However, structural macroeconomic shifts over the past thirty years have systematically dismantled this paradigm. Today, we stand on the precipice of an unprecedented demographic collision: a generation of aging parents who are living longer but retiring with acutely insufficient assets, colliding with an adult offspring generation that is already structurally wealth-compromised.

When a parent's retirement capital is exhausted, the resulting financial vacuum does not simply resolve itself through state intervention or systemic welfare. Instead, the burden is forced downward. The choice confronting adult children is rarely an abstract ethical dilemma; it is a brutal, direct diversion of cash flow. To preserve a parent's basic dignity—shelter, medical care, and nutritional stability—younger cohorts are increasingly forced to cannibalize their own financial foundations, transforming what should be their peak wealth-accumulation decades into an extended rescue operation. This is not merely an emotional challenge; it is an unhedged, asymmetric financial liability that represents the single greatest threat to generational wealth transfer in modern economic history.

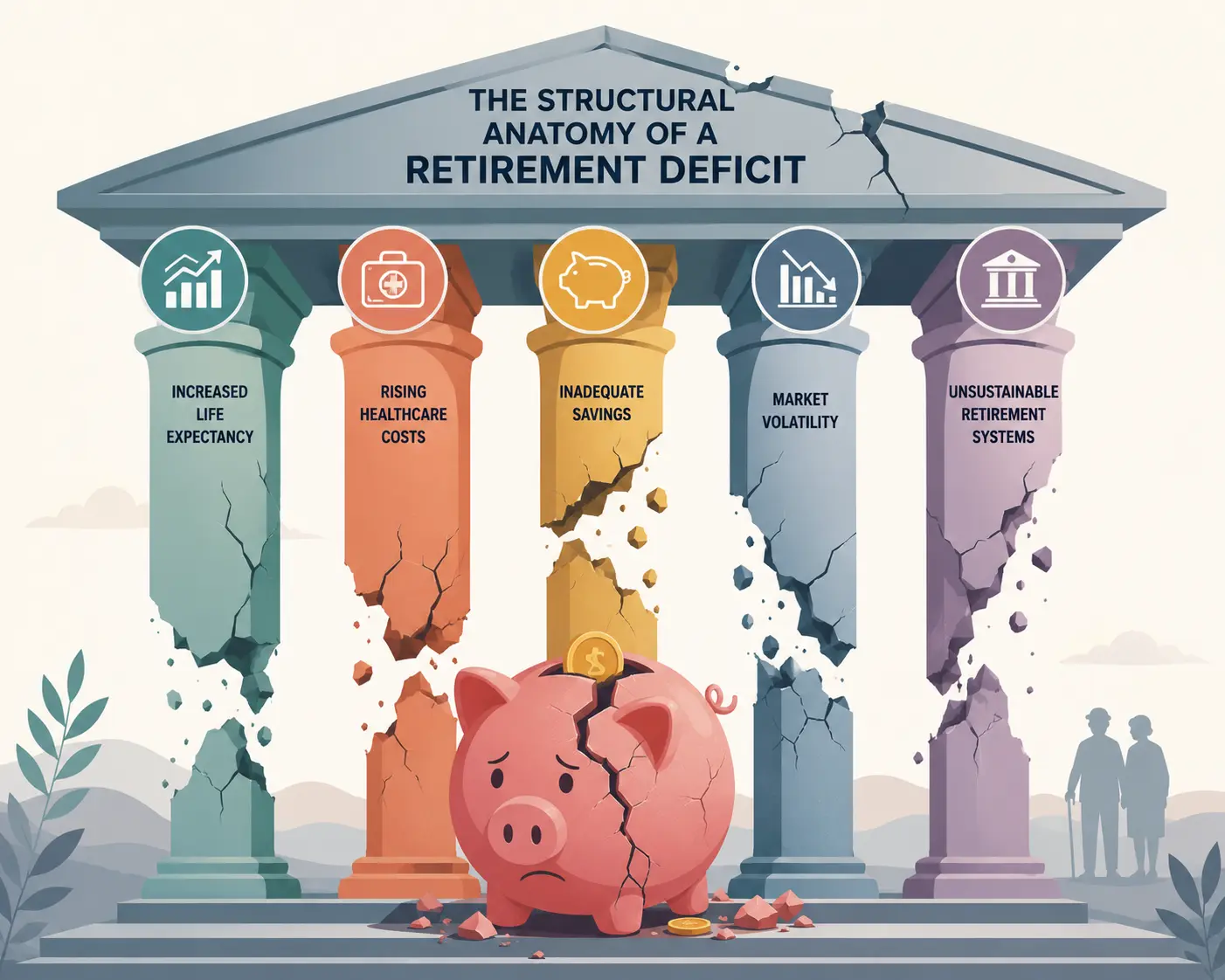

The Structural Anatomy of a Retirement Deficit

To understand how parental retirement evolved from a localized family milestone into a systemic macroeconomic liability, one must analyze the structural changes in how retirement security is funded. The most critical shift has been the wholesale migration from defined-benefit pension schemes to defined-contribution models, primarily the 401(k). In essence, macroeconomic risk was shifted entirely from institutional balance sheets to the fragile cognitive bandwidth of the individual worker. The mathematical fallout of this experiment is now plain to see. Millions of individuals currently transitioning into retirement were the first full generation subjected to this self-directed regime. Deprived of institutional guardrails and forced to navigate volatile equity markets, predatory financial retail products, and stagnant real wage growth, an overwhelming majority failed to accumulate the critical mass of capital required to sustain a multi-decade retirement.

53% — Of Millennials currently rely on their parents for financial support, delaying their own independence and creating a fragile, interdependent financial loop.

$7,242 — Average annual out-of-pocket expenditure incurred by family caregivers, representing roughly 26% of their personal net household income.

Compounding this structural deficit is the aggressive expansion of human longevity. Due to advancements in medical technology, pharmaceuticals, and acute clinical care, the average lifespan has decoupled from historical actuarial assumptions. While living longer is an undeniable triumph of human ingenuity, living longer without a proportional extension of economic productivity introduces severe systemic friction. A nest egg originally engineered to sustain a ten-year retirement is systematically obliterated when stretched across twenty-five or thirty years. When individual capital reserves run dry, the structural dependency on adult children becomes absolute.

According to the June 2026 Northwestern Mutual Planning & Progress Study, a staggering 53% of Millennials—now aged 30 to 45—still rely on their parents for some degree of financial support or guardrails. Simultaneously, a parallel crisis is mounting from the opposite direction: younger generations are increasingly being pulled into the financial care of those very same parents, creating a bidirectional drain on capital that prevents both generations from achieving long-term solvency.

The Velocity of Capital Depletion: Medical and Long-Term Care

The primary catalyst that transforms a parent's minor savings shortfall into an acute, catastrophic financial liability for their children is the hyper-inflationary cost of healthcare and long-term assistance. While routine living expenses can be modified, optimized, or downsized, the cost trajectory of geriatric medical decline is fundamentally inelastic. Most people operate under the dangerous assumption that state mechanisms like Medicare will insulate them from these expenses. This is a profound misunderstanding of policy framework. Medicare is designed to absorb acute medical interventions—surgeries, short-term hospital stays, and prescription drugs. It explicitly excludes custodial care, which constitutes the vast majority of late-stage retirement costs: assistance with daily living activities, memory care, and long-term nursing oversight.

When custodial care becomes necessary due to physical frailty or cognitive decline, the market rates are staggeringly punitive. Modern long-term care infrastructure is priced as a premium luxury service, yet it is a non-negotiable survival necessity.

| Care Infrastructure Tier | Median Monthly Cost | Annualized Capital Requirement | Primary Funding Mechanism |

|---|---|---|---|

| Adult Day Health Care | $1,850 | $22,200 | Out-of-Pocket / Private Cash Flow |

| Assisted Living Facility | $4,800 | $57,600 | Private Assets / Family Supplement |

| Home Health Aide (44 hrs/wk) | $5,150 | $61,800 | Private Assets / Family Supplement |

| Nursing Home (Semi-Private) | $8,200 | $98,400 | Spend-down to Medicaid Welfare |

| Memory Care Unit / Specialized | $10,500+ | $126,000+ | Severe Family Capital Liquidation |

Consider the mathematical reality presented in the table above. If a parent requires a specialized memory care unit due to progressive dementia or Alzheimer's disease, the annualized capital drain exceeds $126,000. For a parent with a modest, or even slightly above-average retirement balance, a single year of cognitive decline can entirely liquidate their lifelong savings. Once that threshold is crossed, the legal and moral liability cascades directly into the personal cash flow of their children.

The Sandwich Generation: The Multi-Generational Squeeze

The financial damage of this liability is not distributed evenly across time; it concentrates aggressively during the peak earning and accumulation years of adult children. This phenomenon has created the "Sandwich Generation"—a cohort of adults simultaneously squeezed between the financial dependencies of their aging parents and the structural developmental costs of their own children. Data from the Bipartisan Policy Center and recent 2025 BMO Financial Group surveys illustrate that nearly 48% of Millennials and Gen Z parents are currently balancing the double weight of managing the emotional and financial care of an aging relative while raising a family. This creates an environment of permanent financial triage. The capital that should be compounding in an index fund for the child's future university tuition or the adult child's own retirement is instead diverted to subsidize parental pharmaceuticals, rent, or part-time home care aides.

"The modern family balance sheet has become a site of systemic structural triage. We are witnessing an unprecedented economic phenomenon where the historical flow of generational wealth is being forcefully reversed, flowing upward to plug structural deficits in an underfunded retirement system."

Advertisement

The hidden cost of this arrangement extends far beyond direct cash transfers. The opportunity cost of time is equally devastating to long-term wealth accumulation. Family caregivers provide an average of 24.4 hours of unpaid labor per week. To accommodate this intense workload, workers are frequently forced to make severe career compromises: declining promotions that require travel, reducing their billable hours, shifting from full-time to part-time status, or exiting the workforce entirely during their highest-earning decades.

The Family Caregiver Alliance notes that the long-term career sacrifice for women—who disproportionately bear the burden of caregiving—ranges from $295,000 to over $324,000 in lost lifetime wages, career progression, and unvested retirement matching contributions. By sacrificing their own career velocity to support their parents, adult children are systematically underfunding their own future retirement, guaranteeing that this cycle of dependency will repeat itself with the next generation.

The Great Inheritance Illusion

Compounding the systemic danger of this unplanned liability is a pervasive psychological blind spot: the expectation of a generational wealth transfer. Financial media frequently trumpets the arrival of "The Great Wealth Transfer," predicting that trillions of dollars will pass down from Baby Boomers to their millennial and Gen Z descendants over the next two decades. This narrative has created a false sense of security, leading many young adults to view inheritance as a structural backstop for their own financial shortcomings.

This expectation represents a catastrophic misunderstanding of late-stage capital velocity. While it is true that older generations hold a significant portion of national wealth, that wealth is highly concentrated in illiquid real estate and concentrated portfolios. More importantly, that capital is highly vulnerable to rapid liquidation by the long-term care industry. A 2025 New York Life Wealth Watch survey highlighted that while over 50% of Millennials anticipate a significant cash or property inheritance, nearly 47% of households currently dealing with an aging parent report that their savings are actively being depleted to meet immediate care expenses. The reality is that for the vast majority of middle-class families, the "Great Wealth Transfer" will actually be the "Great Capital Dissipation." The family home will not be passed down to the children; it will be sold via a standard or reverse mortgage to finance private nursing care or to satisfy Medicaid spend-down provisions. The inheritance is an illusion, masking a looming net liability.

Strategic Mitigation: De-risking the Parental Liability

Given the structural inevitability of this demographic crisis, treating parental retirement as an abstract, emotional issue is a form of financial negligence. It must be reframed as a structural portfolio risk and managed with the same analytical rigor applied to market volatility, inflation hedging, or tax optimization. De-risking this liability requires execution across three distinct strategic pillars.

1. Radical Transparency and Document Auditing

The greatest compounding factor in parental financial failure is silence. Cultural taboos surrounding money frequently prevent adult children from understanding the true state of their parents' balance sheets until a crisis—a stroke, a fall, or an eviction notice—forces the issue. We must break this taboo through deliberate, structured financial audits. Adult children must gain clear visibility into their parents' cash flow inputs (Social Security, defined pensions, annuities) and asset pools (traditional IRAs, liquid brokerages, home equity). Crucially, this audit must include a legal review of estate architecture. Without an established Durable Power of Attorney (DPOA), Healthcare Proxy, and a properly structured living trust, a sudden cognitive decline will freeze parental assets, forcing children into expensive, bureaucratic guardianship proceedings just to access their parents' own funds to pay for their care.

2. Actuarial Risk Shifting: Long-Term Care Insurance (LTCI)

If a parent is still in their late 50s or early 60s and possesses reasonably good health, the option to structurally shift the risk to an insurance balance sheet remains viable. Traditional long-term care insurance policies have faced severe premium inflation, but modern financial engineering has introduced hybrid asset-based policies. These products combine a life insurance policy or annuity with a long-term care rider. If the parent requires care, the policy dispenses tax-free monthly benefits to cover home health aides or assisted living. If they pass away without needing care, a death benefit is passed down to the beneficiaries, protecting the capital from being lost to premium waste. Paying or subsidizing these premiums for your parents is often the highest-ROI investment an adult child can make, effectively buying insurance for their own future cash flow.

3. Structural Medicaid Planning

For parents whose asset base is clearly insufficient to sustain long-term private care, the ultimate financial backstop is Medicaid. However, accessing Medicaid long-term care benefits requires navigating strict asset and income ceilings, alongside a rigorous five-year asset look-back period. Waiting until a crisis occurs to apply for Medicaid is a tactical failure. It forces an immediate, unmitigated spend-down of all parental assets, leaving nothing for a surviving spouse and creating an immediate cash shortfall that children must fill. Engaging an elder law attorney to execute structural asset transfers—such as establishing an irrevocable Medicaid Asset Protection Trust (MAPT)—well in advance of the five-year window is essential. This protects the core family property from estate recovery and ensures the parent qualifies for institutional support without liquidating the entire family safety net.

Conclusion: The Ultimate Imperative of Self-Preservation

Confronting the reality of parental financial decline is an uncomfortable exercise. It demands that we intersect the emotional intimacy of family with the cold, unyielding mechanics of compound interest and healthcare actuarial tables. Yet, failing to do so does not protect our parents; it merely ensures the destruction of our own financial autonomy. The ultimate rule of emergency management applies perfectly to intergenerational finance: you must secure your own oxygen mask before assisting others. Allowing your parents' underfunded retirement to swallow your personal capital structure does not solve their long-term problem; it simply expands the scope of the economic catastrophe. It transforms a single generation's financial deficit into a multi-generational structural vulnerability. By treating your parents' retirement as a quantifiable, manageable financial liability today, you gain the strategic clarity required to protect their dignity tomorrow, without sacrificing your own economic future on the altar of unplanned dependency.

Read Further

[1] Northwestern Mutual. 2026 Planning & Progress Study — More Than Half of Millennials Still Financially Dependent on Parents — Click here

[2] Genworth Financial / CareScout. 2025 Cost of Care Survey — National Median Costs for Assisted Living, Memory Care, and Nursing Home Infrastructure — Click here

Disclaimer: All data, macroeconomic frameworks, and strategic recommendations provided in this article were compiled from publicly available financial surveys, actuarial research, and elder care cost studies. This article is intended for educational and financial literacy purposes only and should not be construed as formal legal, tax, investment, or estate planning advice. Readers are advised to consult a qualified financial planner or elder law attorney for personalized guidance.

Advertisement