In today's era where everything is being created and generated by AI (Artificial Intelligence) we are too much dependent on it — and somehow it is useful for us, and somehow it is not. AI is something that was created to make our work faster and with better efficiency, but when we just ended up depending on AI chatbots and autonomous AI features for our everything, we don't know where we actually forgot, lost, and old methods of long-term wealth preservation and financial discipline — we don't know.

So this article basically is going to get you all aware about what we should do with AI and what we should do with authentic and original traditional methods of budgeting, planning for your easy retirement, and securing a peaceful future preservation for easy living.

Autonomous AI Chatbots and the Efficiency They Provide

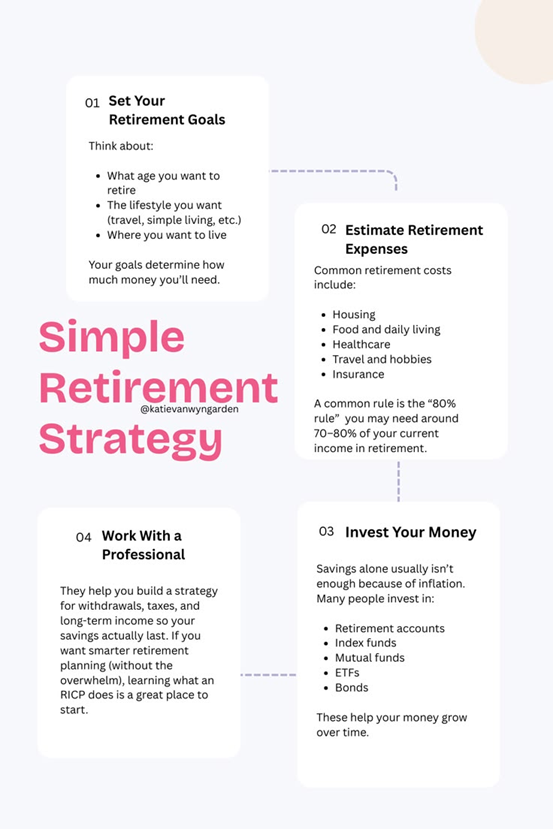

With AI, planning your retirement path has become easier and more efficient to calculate the complex compounded math of your future nest egg and also in managing multi-asset portfolios over decades. Autonomous AI finance tools are evolving beyond simple calculators into "agentic" systems that can:

- Analyze your monthly lifestyle inflation

- Forecast long-term cash flows up to age 90

- Automate your monthly pre-tax contributions

- Optimize target-date funds

- Make micro-investment changes with minimal manual input

These AI tools help you get financial advice while managing your asset allocation and 401(k) or IRA statements, making decisions on your base for your golden years or early retirement goals (like the FIRE movement). These AI tools as well work up on what is trending in the market and help you choose from smart and successful advancements in global equity indexes, high-yield vehicles, and bond ladders to work upon your net worth.

Here are some Agentic AI tools and platforms which you can try to start your retirement planning journey online:

| Platform | Description | Link |

|---|---|---|

| Wealthfront | Autonomous robo-advisor tracking long-term milestones | https://www.wealthfront.com |

| Betterment | Direct automated retirement goals with dynamic tax-loss harvesting | https://www.betterment.com |

| Vanguard Digital Advisor | Structured index-fund automated planning tool | https://vanguard.com |

| Personal Capital / Empower | Comprehensive fee analyzer and retirement cash-flow planner | https://www.empower.com |

| NewRetirement | Deep scenario builder for pension, medical costs, and social security | https://www.newretirement.com |

| MaxFi Planner | Direct optimization engine for maximizing lifetime living standards | https://maxfi.com |

| ChatGPT / Claude / Microsoft Copilot | Can act as conversational mirror to view portfolio breakdowns based on prompt parameters | — |

Cons of Using AI Tools for Retirement Planning

AI, as we know, is still Artificial Intelligence — not a human-based mindset which can think alike like humans and make decisions after calculating endless possibilities in every scenario. In retirement planning, one size never fits all because market black swan events, sudden health care crises, or family legacy decisions cannot be boxed into algorithms.

In recent studies, it was seen that major AI tools do provide wealth management recommendations but with heavier and lengthier prompts where each and every scenario is given, a vast variance in reliability was seen. A wrong projection or missed variable leaves an error in long-term compounding which, if not in weekly household budgets, but in retirement planning can get you into a heavy loss or early depletion of your lifetime savings. Giving prompts and continuously checking asset drawdowns will become an endless loop of getting a few records wrong and getting it changed, which becomes a tiresome chore of the day, leading to severe analysis paralysis.

"Invest consciously and preserve intentionally."

The Traditional Vehicles: Proven Pillars of Preservation

Unlike rapid AI algorithms, traditional retirement architecture relies on time-tested frameworks established by legislative structure and mindful personal discipline. To guarantee an easy living scenario, you must understand the primary paths available:

Annuities & Pensions

| Retirement Plan | Core Mechanism | Ideal User Profile |

|---|---|---|

| 401(k) / 403(b) Plans | Employer-sponsored pre-tax contributions up to $23,000+ per year. Often includes a corporate matching bonus. Tax-deferred growth. | Corporate or non-profit employees looking to instantly double their money via company match. |

| Traditional & Roth IRAs | Individual accounts. Traditional offers up-front tax deductions; Roth offers tax-free withdrawals in retirement. | Individual savers wanting granular control over specific stock/ETF options outside company constraints. |

| Guaranteed Lifelong Income Streams | Backed by insurance contracts or state/corporate systems. | Risk-averse planners looking to secure an exact baseline floor for basic monthly living bills. |

Now it may sound like written versions of AI apps and tools but no — it is the magic of traditional asset allocation which dictates that when you manually map and check your balances yourself, your mind becomes highly aware of what you are building. Knowing exactly how much you save, and reviewing it on raw paper or structured ledgers quarterly, builds an unshakeable habit to think twice before liquidating assets or chasing speculative market bubbles. This physical awareness is the core principle of success in life-long money preservation.

If you prefer standard worksheets to clear your head away from screens, here are some verified manual retirement planning frameworks and PDF sheets to print out:

| Resource | Link |

|---|---|

| DOL Retirement Toolkit PDF | https://www.dol.gov/sites/dolgov/files/EBSA/about-ebsa/our-activities/resource-center/publications/retirement-toolkit.pdf |

| FINRA Retirement Calculator & Worksheet | https://www.finra.org/investors/tools-and-calculators/retirement-calculator |

| IRS Publication 590-B (Distributions Guide) | https://www.irs.gov/forms-pubs/about-publication-590-b |

Disclaimer: All the data provided above was from internet resources and historical studies done upon retirement systems. This should not be taken as professional financial quote or binding legal advice.