It's pretty wild how quickly AI has woven itself into pretty much everything these days. We're creating, analyzing, and generating so much with it, it's almost like we've hit this point of extreme reliance without even noticing. We're really counting on these algorithmic brains to map out our days, draft our emails, and just generally streamline how we get work done. And honestly, a lot of this has been incredibly useful. Things are faster, and we can process way more information than we ever could before. But here's the thing: all this automated ease, this super polished surface, it's hiding a pretty serious vulnerability that we haven't really talked about. In our hurry to hand over the reins to these systems, we might be losing touch with something fundamental: human discipline, how we organize things ourselves, and just being truly present and aware.

When AI first came around, the idea was to make tasks quicker and boost our efficiency. It was supposed to clear away all the tedious administrative stuff so we could actually get to the really important, deep thinking work. But now, when we find ourselves relying completely on things like autonomous AI for managing our finances, or using predictive chatbots for our daily economic survival, a quiet problem starts to emerge. We don't even seem to realize we've forgotten those older, tried-and-true methods of budgeting and taking personal responsibility for our money. It feels like we've slipped into this passive mode, just trusting code to look after our financial future. The problem is, when AI smooths out all the rough edges, all the friction points in our financial lives, it's also paving the way for a new kind of debt we haven't really seen before.

So, looking at where personal and business finances are heading in 2026, it's a really interesting time. We need to be pretty careful about what we're keeping an eye on as we start using these AI tools. And it makes you wonder about those older, more hands-on financial methods. It turns out, those traditional, authentic, and even handwritten approaches to managing money might actually be our strongest protection against bigger economic problems down the road.

Autonomous AI Chatbots and the Efficiency They Provide

You know, it's pretty wild how much artificial intelligence has shaken up the way we handle money. What used to feel like a chore, sifting through bank statements or trying to figure out invoices, now feels… well, different. Easier, for sure. It's like the tedious parts of managing our finances, whether it's our personal checking accounts, business expenses, or even investment portfolios, have just sort of melted away. We're not spending hours poring over spreadsheets anymore, no more mountains of paper receipts. The promise is that this tech takes away this huge mental burden of just keeping track of where our money goes.

Fast forward to 2026, and the AI tools we're seeing now are leagues beyond those basic expense trackers from the early 2020s. We're really in the age of "agentic" systems. Think of these as sophisticated networks of digital agents, kind of like little assistants, that can actually act on our behalf with hardly any input from us. They're constantly watching our cash flow, predicting how much revenue a company might make in a quarter, tweaking our subscriptions to save money, and even making tiny investments based on what the market is doing right now. By connecting directly to things like open-banking APIs and a company's accounting systems, these platforms create this almost self-sustaining financial ecosystem around you.

These advanced tools are also touting this ability to give us instant, highly specialized financial advice. They're constantly comparing massive amounts of data, looking at the bigger economic trends, and then making quick decisions for your business, your career, or even just your personal savings. They keep an eye on what's happening globally, all these fast-moving changes, and then guide you toward smarter ways to put your money to work. To help you get a handle on all this, we've put together a list of some of the big digital platforms and agentic technologies that people and companies are starting to use to kick off their digital budgeting journey:

- YNAB (You Need A Budget) helps you set up financial boundaries using smart envelope tracking methods.

- Monarch Money is great for bringing all your different accounts together and automatically mapping out your financial picture.

- Rocket Money focuses on managing your subscriptions and has agents that can cancel those recurring expenses you might not even realize you're still paying for.

- Cleo uses AI chatbots to talk to you, offering gentle nudges and casual conversations to help you save money.

- Wealthfront is all about automatically optimizing your investment portfolio and growing your wealth through algorithms.

- Betterment offers frameworks for investing based on your goals and uses systems to harvest tax losses.

- Autonomous Technologies Group is building institutional-grade agentic models that can handle treasury operations all by themselves.

- For those who like to tinker, there's the FinRobot project on GitHub, which is an open-source framework for building multi-agent systems.

- ChatGPT by OpenAI is there to act as a personalized financial chat partner, leveraging its large language model capabilities.

- Claude by Anthropic uses its advanced contextual understanding to help you dive deep into financial documents and analyze budgets.

- Microsoft Copilot is built right into spreadsheets, designed to create automatic cash-flow sheets in a snap.

It's a double-edged sword, isn't it? Letting machines handle the financial heavy lifting removes a lot of the headaches, but there's a quiet trade-off happening. We risk losing that human intentionality, that thoughtful approach that's really key to building wealth that lasts.

The same structural tension — where agentic AI promises control but quietly erodes it — is explored in depth in Autonomous Debt Systems or Lost Financial Control?

Cons of Using AI Tools for Budgeting

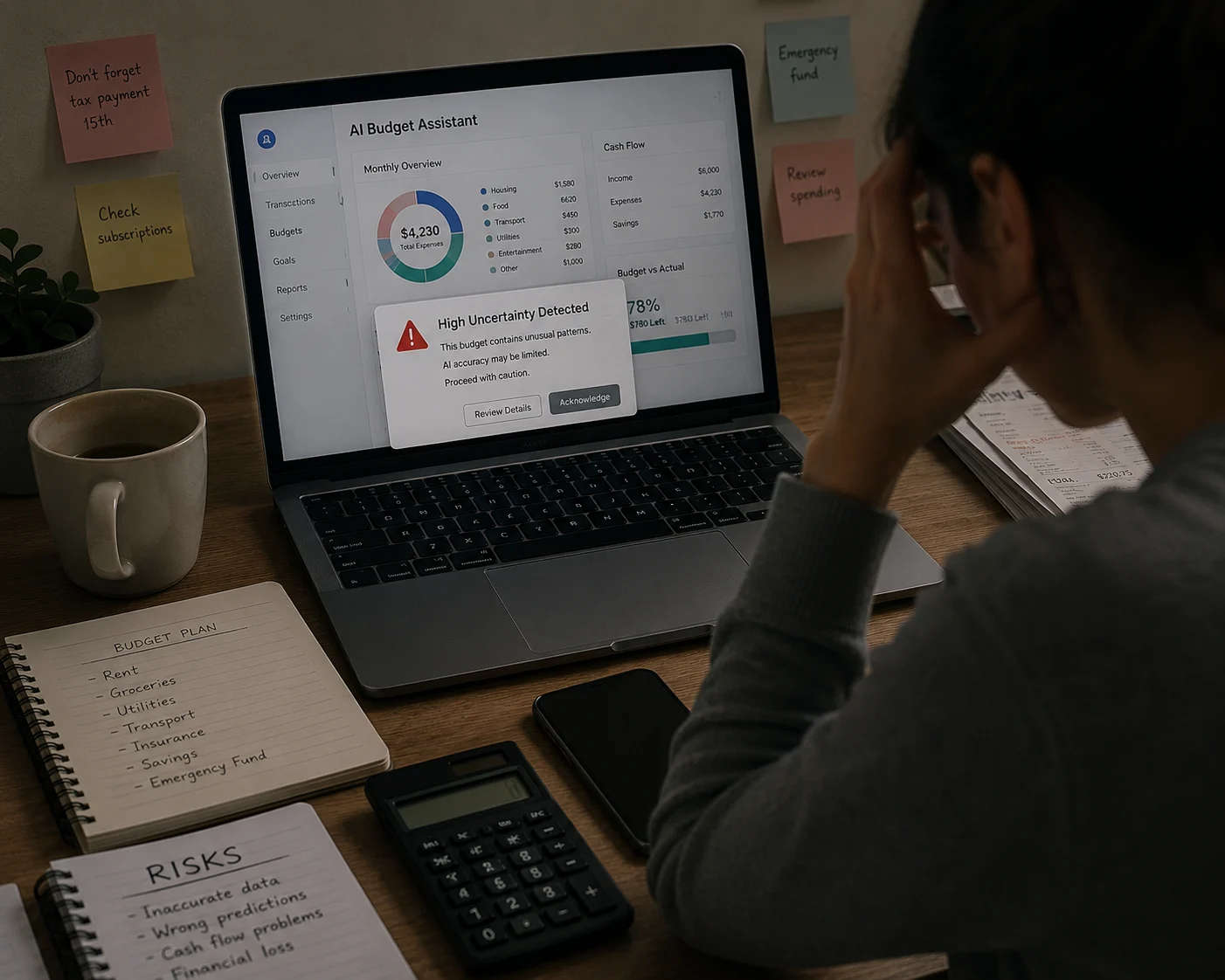

It's funny, isn't it? We've seen AI do some pretty incredible things lately, pushing boundaries we thought were decades away. But as we marvel at these advancements, there's this nagging, slightly awkward truth we have to face: AI, for all its sophistication, is still fundamentally artificial. It's a complex web of algorithms and probabilities, a mathematical construct, and it doesn't quite possess that genuine human spark, that nuanced way of thinking that comes so naturally to us. Empathy, for instance, isn't something it can conjure up organically. And when you think about real-world crises — the messy, unpredictable kind where emotional responses, family obligations, or deeply ingrained local customs often take precedence over cold, hard optimization — AI simply can't grasp those endless, shifting variables. Handing over critical financial decisions entirely to software means we're betting on a level of absolute, unwavering infallibility that, frankly, just isn't a reality.

Some recent studies, the kind that actually track how these financial agents perform in the wild, have uncovered some pretty significant structural issues. You see these major AI tools designed for finance management, and they work reasonably well, but their accuracy takes a nosedive if you're not feeding them incredibly detailed, multi-layered instructions. The research is pretty stark on this: in those tricky, edge-case budgeting situations, the accuracy can be limited to something like 65%. Think about that for a second — that means almost one out of every three automated decisions might be off. For a personal budget, a $40 mistake here or there might just be an annoyance. But scale that up to a corporate treasury or a growing business, and a consistent 35% margin of error in calculating operational risk? That's not just frustrating; that's a recipe for disaster. We're talking about potentially catastrophic losses, damaged relationships with suppliers, and sudden, crippling cash flow problems.

And then there's this whole other layer of hassle that comes with relying on these tools. Instead of saving us time, they often create this frustrating cycle of administrative upkeep. To even get close to accurate results, users find themselves writing these incredibly complex, almost poetic prompts. They're chasing down obscure software bugs, meticulously auditing every single transaction to catch mistakes. What was sold as an effortless, time-saving solution can quickly morph into an exhausting daily grind. This constant mental overhead, the need to second-guess and verify every single decision the machine makes, leads to a kind of widespread cognitive fatigue. It breeds this unsettling professional anxiety and those specific tech-induced headaches that completely negate the very value the system was supposed to provide in the first place.

This cognitive fatigue has a measurable financial cost that extends well beyond the monthly budget. The Hidden Financial Cost of Burnout breaks down exactly what chronic AI-driven work stress is doing to long-term wealth accumulation.

The Invisible Slip: Cognitive Financial Detachment

It's easy to get caught up in the nuts and bolts of technology, like debugging code or untangling those endless prompt loops in AI. But there's something else going on, something a bit more fundamental, that touches on how we think about money. It's this idea of cognitive financial detachment. Think about it: when a system is just handling things for you — automatically sorting out your bills, tweaking your investment portfolios, moving spare cash into savings — money starts to feel less like something you hold and more like an abstract idea. You lose that direct, physical connection to your funds. The satisfying, albeit sometimes painful, act of physically handing over money or seeing it leave your account diminishes.

This smooth, frictionless experience can subtly chip away at our ability to be disciplined with our finances. When everything involved in spending is automated, it's like our built-in financial caution signals get turned down. We're more likely to click "subscribe" on those recurring software services, agree to those little in-app purchases, or easily upgrade to a slightly fancier version of something, all because the system just makes it happen without much fuss. When we take the conscious, deliberate act of budgeting out of the equation, we might unintentionally create a situation where we're structurally overspending. It's like a tiny, unseen drip that, over time, can really wear down both individual savings and a company's bottom line.

The Counter-Revolution: Resurrecting the Traditional Kakeibo Method

With homes and cities under increasing pressures to automate life, an equal and opposite reaction is building. Housewives, professionals and thinkers alike are abandoning automatic dashboards in favor of classic, systematic and thoughtful methodologies. Among the most popular of these is Kakeibo, the conventional Japanese practice of household money management.

The expression is derived directly from 3 core kanji words in Japanese: Kake or 家計 means "household," i in 料理居 (the i within ryo-u-ri means "financial accounts"), and Bo or ぼ in 紙帳簿 (the bo within shi-chōbo means "a physical journal or notebook"). Kakeibo (家計簿) is the traditional Japanese budgeting system.

Kakeibo was created in 1904 by Japan's first female journalist, Hani Motoko. She introduced it in a popular women's magazine as a practical means to assist people in managing household budgets with thought and care during a period of rapid modernization in the country. Her desire was to get people to stop and think about what they were buying, to save more, to stop buying frivolously and to bring a measure of financial discipline to households. But she makes it clear: her intent is to promote conscious consumption, better saving habits, less frivolous purchasing and more comprehensive financial discipline for families.

Unlike modern digital budget apps, Kakeibo prioritizes reflection and self-awareness over the ease of automated math. It dates back to handwritten journaling. Writing your income down, making real-world savings goals, and updating physical pages all in all makes you face your financial situation a little more head-on. The classical model divides expenditure into four basic types:

- Needs: Unavoidable structural living necessities such as housing, utility bills, basic groceries, and health-related expenses like insurance and medicines.

- Wants: Non-essential purchases that you choose to make but don't strictly need — things like designer furniture, fashionable clothes, dining out, or entertainment subscriptions.

- Cultural: Intentional investments in personal development and lifelong learning, including books, museum outings, education courses, skill seminars, and artistic training.

- Unexpected: Irregular yet predictable costs that don't form part of the regular budget — such as celebratory dinners out, personal care appointments, or unforeseen home repairs.

At the end of a month, the Kakeibo process leads users through a purposeful self-examination. You add up all your expenses and subtract them from the money you have coming in, and you know exactly how much you saved. While this may sound like simply a manual version of finance apps, the real magic comes in the writing. Studies have demonstrated that handwriting activates various areas of the brain that are not stimulated when typing on a keyboard.

Writing in a journal builds an immediate, deep consciousness of your options. It introduces a natural pause — compelling you to re-check your choices before investing your money, and that's the root of sustainable wealth management.

"Spend consciously and save intentionally."

For those who want to adopt this approach, some excellent frameworks and print-friendly layout kits can be found online at:

- IOOF Kakeibo PDF Template — Structured corporate-designed reflection frameworks.

- ANZ Kakeibo Method Template — A simple format for daily transaction recording.

- Kawaii Kakeibo Planner Template — An artistic, user-friendly option for daily journaling.

Bridging the Divide: Framework for 2026

There is no necessity to completely throw out the contemporary technology or deny the obvious advantages of automated mechanisms. The way forward is to seek an enlightened compromise between automation and human will. We can utilise the rapidity of agentic AI in heavy data processing whilst maintaining the reflective clarity of Kakeibo in strategic decisions. By pairing structural digital tracking with routine manual audits, you can guard against cognitive dissonance and build long-lasting financial resilience.

Read Further

-

Wikipedia. Kakeibo — Japanese Household Savings Method. — en.wikipedia.org/wiki/Kakeibo

-

Frontiers in Psychology / PMC. The Neuroscience Behind Writing: Handwriting vs. Typing — Who Wins the Battle? — ncbi.nlm.nih.gov/pmc/articles/PMC11943480

Disclaimer: The comprehensive analysis presented above is synthesized from global internet resources, technological case studies, and behavioral budgeting research. It is designed for educational purposes and should not be interpreted as definitive professional investment advice or an official endorsement from our publication.