In today's era where political narratives are increasingly driven by immediate electoral incentives and populist guarantees, we are becoming far too dependent on short-term fixes that satisfy current voters while aggressively shifting fiscal burdens onto future generations. Somehow, these populist measures offer immediate relief, but economically, they establish unsustainable traps. Systems are built to ensure institutional continuity and structural safety, but when governance ends up compromising financial discipline for immediate political validation, we lose the structural guardrails that protect state finances from outright collapse. We don't realize where we forgot the tough lessons of the past, but the macroeconomy remembers.

This comprehensive briefing focuses on a critical policy shift that has sent shockwaves through India's financial regulatory architecture: the decisions by five state governments — Rajasthan, Chhattisgarh, Jharkhand, Punjab, and Himachal Pradesh — to abandon the market-linked National Pension System (NPS) and revert to the legacy Old Pension Scheme (OPS). Through data compiled directly by the Reserve Bank of India's (RBI) internal research teams, this report uncovers the mathematical realities, structural risks, and generational inequities behind this regressive shift.

The Mechanisms of the Fiscal Trap: OPS vs NPS

To fully understand why RBI economists view this shift with extreme alarm, one must break down the fundamental mathematical structures of the two pension systems. The Old Pension Scheme (OPS) is characterized as a defined-benefit plan. Under its provisions, retiring government employees receive a guaranteed monthly payout equivalent to 50% of their last drawn salary, supplemented by regular Dearness Allowance (DA) adjustments to counter inflation. The primary systemic hazard of the OPS is that it operates as an unfunded, "Pay-As-You-Go" (PAYG) system. Current pension liabilities are not funded by assets saved or invested in the past; instead, they are paid directly out of the current tax revenues collected from today's citizens.

The Old Pension Scheme represents a classic structural mismatch: it locks in long-term, inflation-indexed liabilities on the expenditure side without any corresponding asset creation on the revenue side, forcing a direct transfer of liability onto future tax paying generations.

Conversely, the National Pension System (NPS), introduced systematically across India for new employees joining after January 1, 2004, is a defined-contribution system. Under the NPS, both the employee and the employing government make predefined monthly contributions (typically 10% and 14% of the basic salary respectively) into a dedicated corpus. This corpus is dynamically managed by professional fund managers across diversified equity and debt instruments. Upon retirement, the accumulated corpus is utilized to purchase an annuity that yields a steady monthly income. The NPS shifts the fiscal risk away from the state exchequer to the capital markets, making the state's annual expenditure completely predictable and legally capped.

Macro Analysis: The structural pivot from NPS back to OPS allows states an artificial, temporary cash windfall today because they immediately stop transferring the government's 14% matching share to the pension regulatory body (PFRDA). However, this creates a compounding, unfunded massive liability balloon that begins to burst exactly when the current workforce starts retiring en masse.

Quantifying the Dangerous Surge: The Implosion of State Finances

A rigorous study published by researchers within the RBI's Strategic Research Unit evaluated the quantitative impacts of this policy reversal. The findings indicate that if all state governments revert to the OPS, the cumulative fiscal burden could escalate to an astonishing 4.5 times that of the NPS framework. The short-term benefit realized by the five states is dwarfed by the massive tail-end liability that will accumulate over the coming decades.

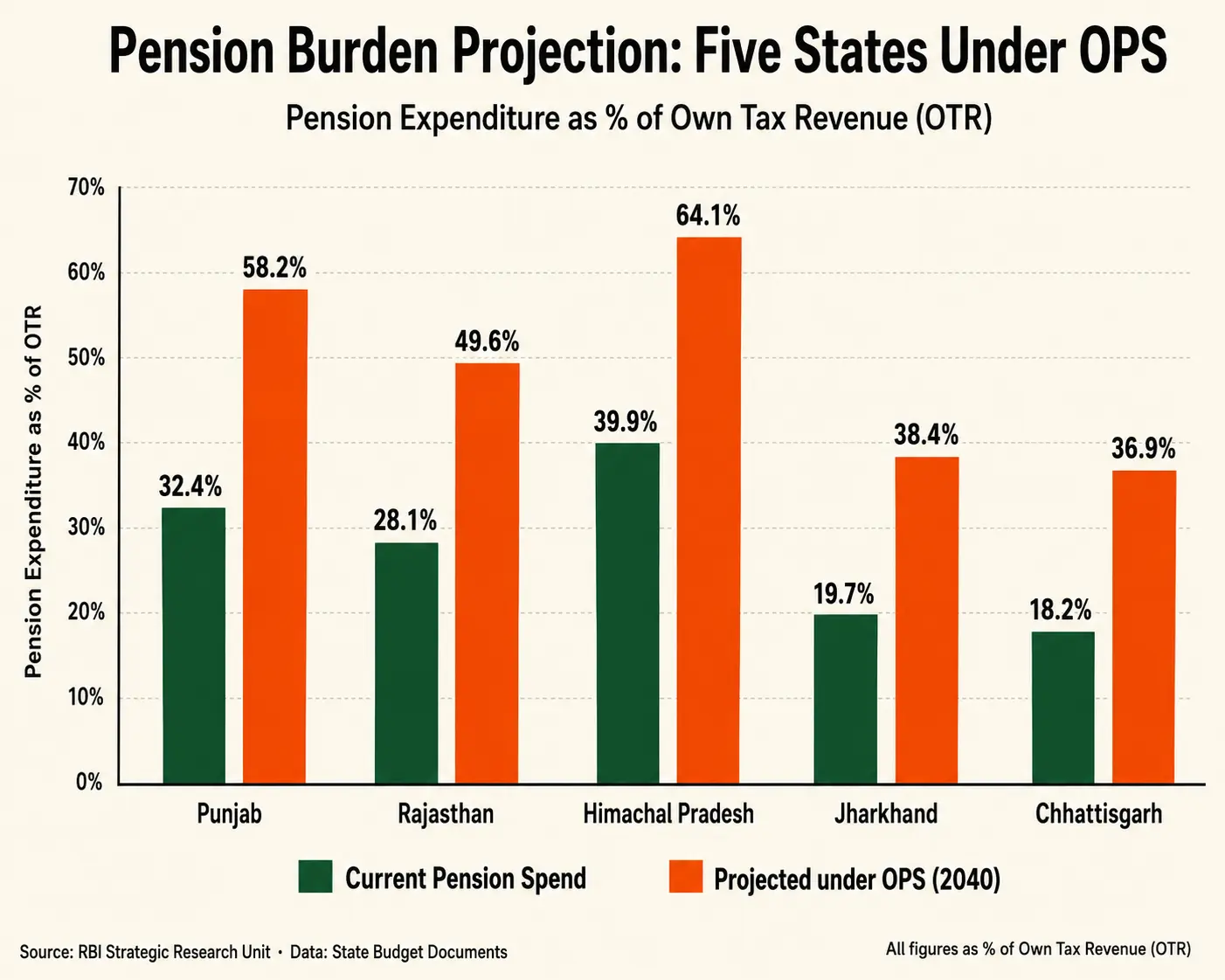

The ratio of pension expenditures to the states' own tax revenues (OTR) highlights the extreme structural fragility introduced by this choice:

| State Government | Pension Spend as % of OTR (Current) | Projected Pension Spend as % of OTR under OPS (2040) | RBI Fiscal Risk Assessment |

|---|---|---|---|

| Punjab | 32.4% | 58.2% | Critically High / Imminent Debt Trap |

| Rajasthan | 28.1% | 49.6% | High Structural Stress |

| Himachal Pradesh | 39.9% | 64.1% | Severe Institutional Vulnerability |

| Jharkhand | 19.7% | 38.4% | Moderate-to-High Structural Stress |

| Chhattisgarh | 18.2% | 36.9% | Accelerating Fiscal Risk |

The numbers demonstrate an alarming trend: states like Himachal Pradesh and Punjab are already spending between 32% and 40% of their internally generated tax revenue purely to fulfill pension obligations for a tiny fraction of their population (typically less than 4% of the state population consists of government servants). Reverting to the OPS means that by the year 2040, nearly 50 to 65 paise out of every single rupee collected via state taxes will be directly funneled to pay for pensions, leaving virtually zero fiscal room for critical public services, healthcare, infrastructure development, or school education.

The Long-Term Consequences: Crowding Out and Capital Starvation

Giving in to popular pressure and abandoning financial prudence creates a continuous cycle of compounding mistakes. Managing state finances through unfunded schemes requires checking and rechecking revenue allocations, leading to a tedious chore of shifting funds, issuing emergency bonds, and struggling to manage market borrowings. This introduces immense friction into public expenditure management and results in structural fiscal headaches for years to come.

The core economic consequences of this return to OPS can be synthesized into three critical vectors:

1. Capital Expenditure Starvation The laws of fiscal mathematics dictate that every rupee allocated to an unfunded, non-productive pension payout is a rupee stolen from asset creation. States will be forced to compress their capital outlays. This means fewer highways, compromised power grids, minimal investments in technology parks, and a total deceleration of physical infrastructure creation. This starvation of capital outlays directly hurts the long-term gross state domestic product (GSDP) growth rate.

2. The Widening Debt-to-GSDP Spiral As pension obligations grow, states will inevitably turn to open market borrowings to cover basic operational costs. This triggers an aggressive rise in the Debt-to-GSDP ratio, quickly pushing states beyond the recommended 25% threshold outlined by fiscal responsibility frameworks (FRBM). Higher borrowing requirements trigger market premium penalties, raising the cost of capital for the entire state economy.

3. Extreme Generational Inequity The OPS creates a highly unequal moral dynamic. A tiny elite of retired public sector employees is protected by inflation-indexed lifetime payouts funded by taxing the vast majority of unorganized sector workers, who possess no formal social security. Future generations are burdened with heavy taxes to pay for services consumed decades earlier, without inheriting any productive infrastructure assets.

"Spend consciously and save intentionally" is a maxim that applies just as sharply to sovereign states as it does to individual households. Abandoning market-linked contributions for defined-benefit guarantees is the exact antithesis of intentional macroeconomics.

Concluding Analysis: Balancing Populism with Financial Sanity

The warnings from RBI economists are clear and urgent. The decision by these five states is a dangerous choice that puts immediate political gain ahead of long-term financial stability. It trades permanent, compounding institutional liabilities for minor, short-term relief on matching contributions. While automated accounting and market borrowing can temporarily disguise this fiscal stress, they cannot alter the mathematical reality of unfunded debt.

To avoid a sub-national debt crisis, states must maintain strict financial discipline. True social security is not achieved by bankrupting the public treasury for a small group of retired employees. Instead, it requires strengthening defined-contribution frameworks, enhancing annuity yields, and building a broad, sustainable social safety net that protects all citizens without placing an unfair burden on future generations.

References

[1] Reserve Bank of India. State Finances: A Study of Budgets — Click here

[2] Ministry of Finance, Government of India. Fiscal Responsibility and Budget Management (FRBM) Act and Framework — Click here

Disclaimer: The data, projections, and qualitative evaluations presented in this document are synthesized from research papers published by economists associated with the Reserve Bank of India, state budget documents, and public financial databases. This analysis is intended for educational and structural research purposes and should not be construed as direct financial or investment advice.