In today's era where digital systems capture our focus, stock trading apps make market access instant, and algorithmic recommendation models offer countless opinions on where to put our hard-earned money, we face a major challenge. We are often overwhelmed by options and detached from the actual value of our capital. Financial tools have become highly streamlined, allowing automated one-click investments into mutual funds, fractional equities, and high-yield vehicles. Yet, much like relying on automated apps to run our lives without human thought, we risk losing the core mindset of financial management: mindful intent and deliberate discipline.

Investing is not merely a game of choosing numbers or letting an autonomous system make choices for you. It requires an understanding of structural boundaries, asset behavior, and systemic risk. To invest effectively, one must treat the portfolio as a piece of architectural engineering. It needs a clear foundation, structured partitions, and columns designed to handle stress during market volatility. Whether you are deploying a starter sum of ₹10,000, a moderate stack of ₹50,000, or a deeper capital base of ₹1,00,000, the foundational rule remains constant: you must know what your capital is protecting, where it is building, and why it is positioned there.

"Deploy consciously, structure intentionally, and measure consistently."

This article provides a practical blueprint for navigating the current market environment across three different tiers of capital. We bypass speculative trends to focus on real asset classes available to Indian investors — ranging from low-cost Nifty index funds and sovereign-backed instruments to targeted sectoral equities and skill acquisition. By structuring these allocations, we combine the efficiency of modern financial instruments with the mindful oversight needed for long-term growth.

The Foundation Tier: Deploying ₹10,000

When you have a capital base of ₹10,000, your primary objective is not complex diversification across a dozen different assets. Attempting to spread ₹10,000 too thinly reduces compounding potential and increases transactional friction. At this stage, your focus should be on building a strong foundation, prioritizing high-equity exposure for long-term growth, and investing in yourself to enhance your earning capacity. At this tier, we partition our capital into two structural areas: Market Exposure (80%) and Knowledge Capital (20%). This balance ensures your money begins working in the broader economy immediately, while a dedicated portion goes directly toward upgrading your personal skills and financial literacy.

Market Exposure: Low-Cost Index Accumulation (₹8,000)

For the core market allocation of ₹8,000, the most reliable approach is to invest in a low-cost Nifty 50 Index Mutual Fund or Exchange-Traded Fund (ETF). By tracking the top 50 companies listed on the National Stock Exchange (NSE) by market capitalization, you gain immediate exposure to India's leading corporate sectors — including banking, information technology, energy, and consumer goods — without the high management fees of actively managed funds. Historically, India's broader market index has delivered long-term compounded annual growth rates (CAGR) fluctuating between 11% and 14% over extended periods. Investing in an index fund offers a major structural advantage: automatic rebalancing. If a company underperforms and falls out of the top 50, the index replaces it with a growing competitor. This ensures your capital stays tied to the strongest parts of the national economy without requiring daily tracking or constant portfolio adjustments.

Knowledge Capital: Practical Skill and Literacy Acquisition (₹2,000)

The remaining ₹2,000 should not be placed into speculative options or high-risk micro-cap stocks. Instead, it is best used as Knowledge Capital. In the early stages of building wealth, your personal capacity to generate income is your most valuable asset. Spending ₹2,000 on deep-dive technical books, professional certifications, or specialized courses yields an incomparable return on investment (ROI). Consider dedicating this capital to foundational literature on market psychology, technical accounting, or specialized skills within your professional field. Improving your core capabilities can directly lift your primary income, turning a ₹2,000 investment into thousands more in recurring earning capacity over the following months.

₹10,000 Structural Breakdown

| Asset Classification | Allocation (%) | Exact Capital (₹) |

|---|---|---|

| Nifty 50 Index Direct Fund / ETF | 80% | ₹8,000 |

| Technical Certifications / Financial Books | 20% | ₹2,000 |

| Total Stack | 100% | ₹10,000 |

The Balanced Tier: Deploying ₹50,000

With a capital base of ₹50,000, your strategy moves from a simple starter layout to a more deliberate, multi-layered architecture. Here, you have enough funds to split your investments across different asset classes, balancing market growth with fixed-income stability. This approach protects your core capital from sudden market drops while still capturing long-term gains. At this level, we use a structured three-part allocation strategy: Large-Cap & Mid-Cap Equities (60%), Debt & Sovereign Security (30%), and Dynamic Strategic Alpha (10%). This balance gives you strong growth potential while keeping a stable cash or fixed-income buffer to smooth out market volatility.

Core Equity Base: Large-Cap and Mid-Cap Partitioning (₹30,000)

We split the ₹30,000 equity core evenly into two distinct tranches to capture different types of market opportunities:

- Tranche A: Large-Cap Stability (₹15,000): This goes into a Nifty 50 index fund or top-tier blue-chip companies. These businesses provide steady performance, clear corporate governance, and reliable dividend yields, forming the stable core of your equity portfolio.

- Tranche B: Mid-Cap Growth Potential (₹15,000): This goes into a Nifty Midcap 150 Index Fund or a select mid-cap mutual fund. Mid-cap companies are established businesses that are expanding rapidly into market leaders. While they carry higher short-term volatility than large-caps, they offer significantly higher growth potential during economic expansions, helping to boost your portfolio's overall returns over time.

Fixed Income Buffer: Debt & Sovereign Instruments (₹15,000)

To balance your equity investments, we place ₹15,000 into secure debt instruments, such as Corporate Debt Funds, high-rated Fixed Deposits (FDs), or Sovereign Gold Bonds (SGBs) if available on the secondary market. This allocation serves as your portfolio's anchor. When equity markets face sharp declines, fixed-income assets remain steady, preserving your capital and ensuring your overall portfolio value doesn't experience extreme swings. Additionally, keeping funds in liquid debt or fixed income gives you the flexibility to rebalance into equities when market corrections offer attractive buying opportunities.

Strategic Alpha: Active Satellite Selection (₹5,000)

The final ₹5,000 is your Strategic Alpha satellite. This smaller allocation allows you to take focused positions in specific sectors without risking your broader portfolio. You can use it to invest in individual high-quality companies with strong earnings growth, or sector-specific mutual funds (such as technology, infrastructure, or banking) that are positioned to benefit from upcoming economic cycles. This lets you chase higher returns while keeping 90% of your capital safe in your core investments.

₹50,000 Balanced Allocation Matrix

| Asset Pillar | Allocation (%) | Exact Value (₹) |

|---|---|---|

| Nifty 50 Index Fund / Large-Cap Core | 30% | ₹15,000 |

| Nifty Midcap 150 Index Direct Fund | 30% | ₹15,000 |

| Liquid Debt Funds / High-Grade Fixed Deposits | 30% | ₹15,000 |

| Sectoral Selection / High-Conviction Individual Stock | 10% | ₹5,000 |

| Total Stack | 100% | ₹50,000 |

The Advanced Tier: Deploying ₹1,00,000

Managing a capital pool of ₹1,00,000 opens up a much wider range of investment options. At this level, you can build a highly resilient portfolio across multiple asset classes, including large-cap stability, mid-cap and small-cap growth, international diversification, precious metals, and opportunistic liquid reserves. This advanced structure is designed to actively grow wealth while thoroughly managing risk across different economic environments. We divide this portfolio into five clear capital components to balance growth, stability, and liquidity: Broad Market Core (50%), High-Growth Aggressive Satellite (20%), Fixed Income Anchor (15%), Hard Assets & Commodities (10%), and an Opportunistic Cash Reserve (5%).

Broad Market Core: The Equity Anchor (₹50,000)

The cornerstone of this portfolio is a ₹50,000 allocation dedicated entirely to highly stable, broad-market equities. This capital is split into two main areas: ₹35,000 goes into a Nifty 50 Index Fund or an absolute blue-chip large-cap fund to secure consistent, long-term market returns. The remaining ₹15,000 goes into a Next 50 or Large & Mid-Cap blended fund, capturing the growth of emerging market leaders while maintaining a highly secure foundation.

High-Growth Aggressive Satellite (₹20,000)

To boost the long-term compounding potential of your portfolio, we allocate ₹20,000 to high-growth, higher-risk assets, split into two specific components:

- Small-Cap Allocation (₹10,000): This is placed into a Nifty Smallcap 250 Index Fund or an actively managed small-cap fund. Small-cap stocks can experience sharp price swings over shorter periods, but over multi-year horizons, they can deliver exceptional growth as young companies expand their operations and market share.

- International Diversification / Technology Sector (₹10,000): This goes toward international mutual funds or domestic technology-focused ETFs. Investing globally or in high-innovation sectors reduces your reliance on a single geographic market, protecting your capital from localized economic downturns while capturing global technology growth trends.

Fixed Income Anchor & Capital Preservation (₹15,000)

To balance out the high-growth equity allocations, we place ₹15,000 into low-risk, income-generating debt instruments, such as highly-rated banking debt funds, Public Provident Fund (PPF) contributions, or multi-year corporate debt securities. This fixed-income anchor creates a predictable yield stream and acts as a financial shock absorber, keeping your portfolio grounded and resilient when equity markets face sudden volatility.

Hard Assets & Commodities: The Inflation Hedge (₹10,000)

We allocate ₹10,000 into digital gold or silver via regulated Exchange-Traded Funds (ETFs) or Sovereign Gold Bonds on the secondary market. Precious metals serve a vital role in long-term wealth protection: they act as a natural store of value and an inflation hedge. During periods of geopolitical stress or high global inflation, commodities often move in the opposite direction of traditional equities, providing excellent diversification and protecting your portfolio's purchasing power.

Opportunistic Cash Reserve: Liquidity and Flexibility (₹5,000)

The final ₹5,000 is kept entirely liquid in a high-yield savings account or a liquid overnight fund. Rather than being fully invested on day one, this reserve is held explicitly for market opportunities. When equity markets experience sudden corrections, asset valuations drop to highly attractive levels. Having this cash readily available allows you to make calm, tactical purchases during market pullbacks, turning short-term corrections into long-term advantages.

₹1,00,000 Advanced Capital Map

| Portfolio Segment | Weight (%) | Value Allocation (₹) |

|---|---|---|

| Nifty 50 Direct Index Allocation | 35% | ₹35,000 |

| Nifty Next 50 / Blended Mid-Cap Index | 15% | ₹15,000 |

| Nifty Smallcap 250 / Active Small-Cap Selection | 10% | ₹10,000 |

| International Index Feeder Fund / Tech ETF | 10% | ₹10,000 |

| Banking & PSU Debt Fund / Corporate Debt Allocation | 15% | ₹15,000 |

| Gold ETF / Digital Gold Sovereign Units | 10% | ₹10,000 |

| Overnight Liquid Fund / High-Yield Capital Reserve | 5% | ₹5,000 |

| Total Comprehensive Capital | 100% | ₹1,00,000 |

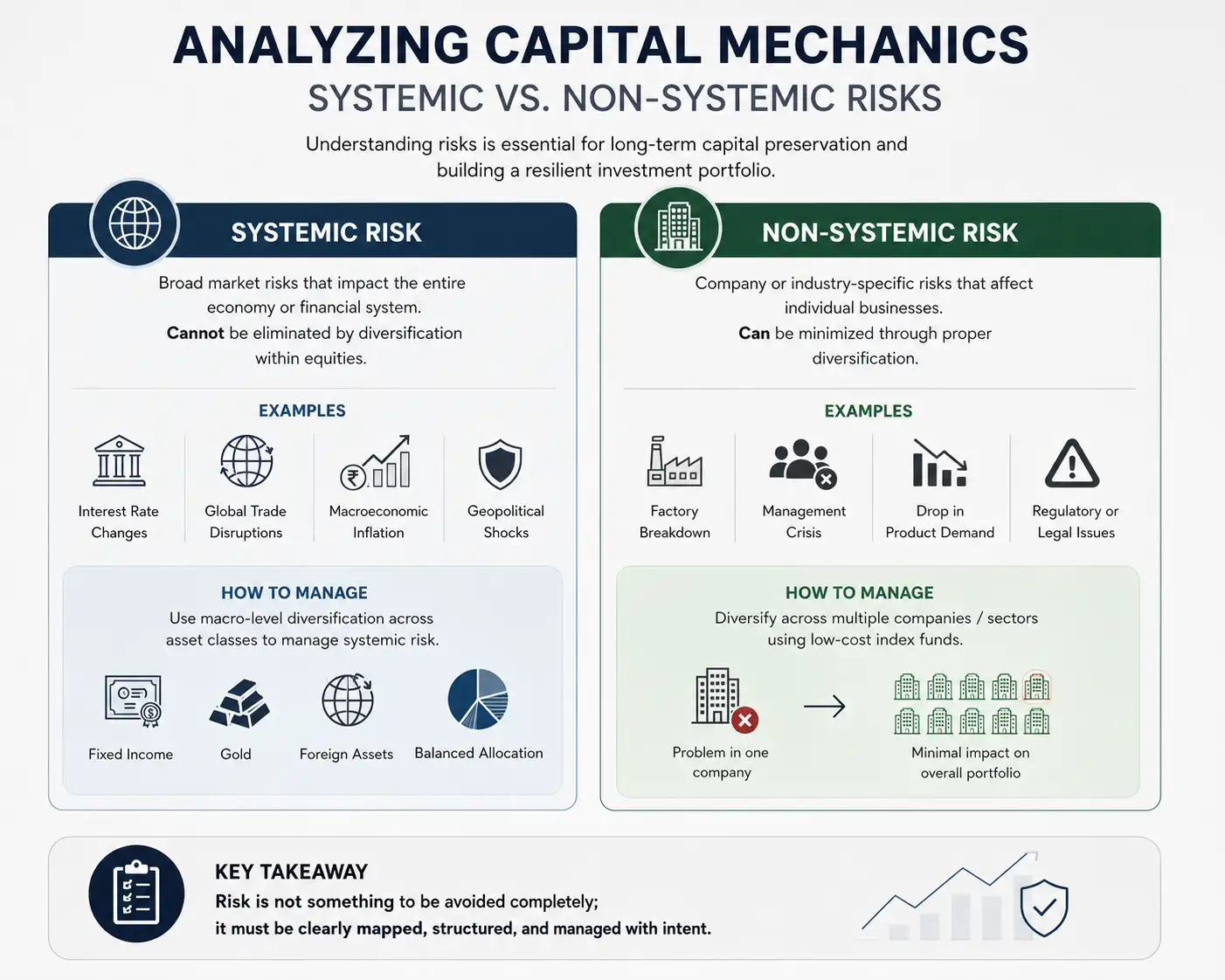

Analyzing Capital Mechanics: Systemic vs. Non-Systemic Risks

To manage an investment portfolio effectively at any level, you must understand the core risk factors that influence asset performance. Broadly speaking, risks are split into two categories: systemic and non-systemic risk. Understanding the difference between them is essential for long-term capital preservation.

Systemic Risk: This refers to broad market risks that impact the entire economy simultaneously, such as shifts in central bank interest rates, global trade disruptions, macroeconomic inflation, or sudden geopolitical shocks. Systemic risk cannot be eliminated by simply adding more stocks to your portfolio. Instead, it must be managed through macro-level diversification — such as holding fixed income, gold, or foreign assets alongside your equity investments.

Non-Systemic Risk: This is corporate or industry-specific risk, such as a company suffering a factory breakdown, facing a sudden management crisis, or dealing with a drop in product demand. Non-systemic risk can be easily minimized through sensible asset diversification. By using low-cost index funds to spread your capital across dozens of companies, you ensure that a crisis at any single business won't cause severe damage to your overall portfolio value.

"Risk is not something to be avoided completely; it must be clearly mapped, structured, and managed with intent."

The Discipline of Long-Term Wealth Accumulation

While selecting the right asset allocation is highly important, the true driver of long-term wealth accumulation is consistency and emotional discipline. Many investors start with great plans but abandon them during periods of market volatility. Achieving excellent financial outcomes relies heavily on implementing consistent execution frameworks, such as Systematic Investment Plans (SIPs) and steady Rupee Cost Averaging.

Markets naturally move in cycles of expansions and corrections. Trying to time the exact bottom or peak of a market cycle is nearly impossible and often leads to costly emotional mistakes. By investing a fixed amount at regular intervals, you automatically buy fewer mutual fund units when prices are high and more units when prices drop during market pullbacks. This disciplined process removes guesswork and emotion from investing, turning short-term market fluctuations into a powerful engine for long-term compounding. To understand the common behavioral traps that derail this discipline at the very start of an investor's journey, see 10 Investing Mistakes That Cost Beginners Lakhs.

Concluding Thoughts: Merging Modern Access with Clear Financial Intent

Ultimately, successful wealth management is about finding the right balance between modern convenience and personal financial discipline. Today's digital tools offer incredible convenience — allowing us to open investment accounts, automate recurring deposits, and track global portfolios with a few taps on a screen. However, this ease of access can sometimes detach us from the real value of our money, leading to impulsive decisions or a hands-off approach to our long-term goals.

True financial success comes from combining the speed and efficiency of modern investment platforms with a deeply mindful, hands-on approach to our financial structures. No matter if you are deploying ₹10,000, ₹50,000, or ₹1,00,000, your focus should remain on building a clear asset architecture, setting deliberate goals, and reviewing your progress regularly. By taking active ownership of your financial structures and understanding exactly where and why your money is positioned, you can build a highly resilient portfolio designed to support your long-term future.

Read Further

- Nifty 50 Index — Composition, Methodology, and Historical Returns — NSE India Official

- Sovereign Gold Bond Scheme — Reserve Bank of India

- Public Provident Fund (PPF) Scheme — Ministry of Finance, Government of India / India Post

Disclaimer: The information and analysis provided in this article are for educational and informational purposes only. This content should not be interpreted as definitive financial, investment, or legal advice. Asset allocations, market returns, and financial metrics are based on historical trends and publicly available data, which can fluctuate over time. Readers should perform their own thorough research or consult with a certified financial professional before making any real-world financial commitments or investment decisions.