In today's fast-paced economic arena, where rapid wealth creation and equity market booms are giving rise to thousands of new neo-rich individuals every month, crossing the magical threshold of a 1 Crore INR net worth is celebrated as the ultimate hallmark of middle-class exit and financial liberation. We are constantly flooded with advice on how to accumulate this wealth—investing through systematic investment plans (SIPs), chasing micro-cap multi-baggers, maximizing tax-exempt growth, and optimizing asset allocations via complex modern algorithms. We are conditioned to believe that hitting eight figures is a pure, unadulterated mathematical win that guarantees long-term freedom and automated lifestyle inflation mitigation.

But just as relying solely on automated AI chatbots can blind us to the foundational discipline of conscious manual budgeting, obsessing purely over wealth accumulation blinds us to the harsh structural shifts that trigger the moment you step across the 1 Crore line. Becoming rich in a developing superpower like India carries hidden institutional, social, and psychological side effects. It alters your legal standing with the state, introduces non-linear tax burdens, transforms you into a prime target for systemic mis-selling, and triggers behavioral traps that can silently destabilize your financial health if you do not understand the hidden rules of the wealth game.

This comprehensive analytical report exposes the deep structural shifts, quantitative realities, and mental transformations that occur when your balance sheet touches eight figures in India. It acts as a realistic manual for the modern Indian investor, exposing the invisible costs that wealth managers rarely mention.

The Fiscal Friction: Surcharges, Compliance, and the Taxman's Lens

The first and most brutal realization that hits a newly minted multi-millionaire in India is that the fiscal landscape shifts from a progressive linear tax structure to an aggressive, surcharge-heavy system designed to redistribute wealth. When your individual taxable income scales alongside your growing capital base and crosses specific thresholds, the Indian Income Tax Act introduces the concept of a surcharge—a tax on top of your existing tax. This instantly lowers your net realized rate of return, fundamentally changing your real purchasing power. Use our Income Tax Calculator to model exactly how your effective tax rate shifts across the 50 Lakh and 1 Crore thresholds under both regimes.

The Middle-Class Fiscal Regime

- Standard progressive tax brackets up to 30% under the old or new tax regimes.

- Zero surcharge liabilities on total income beneath the 50 Lakh threshold.

- Minimal regulatory reporting requirements; standard Form 16 and automated ITR-1/2 filing.

- Low probability of deep scrutiny or continuous scrutiny on domestic investment accounts.

The 1 Crore+ Structural Realities

- Immediate imposition of a 10% surcharge if income crosses 50 Lakhs, escalating to 15% at 1 Crore.

- Mandatory compliance with Schedule AL (Assets and Liabilities) for income over 50 Lakhs.

- Capital gains tax structural shift; long-term capital gains (LTCG) on equities face full surcharges.

- Elevated scrutiny through the Annual Information Statement (AIS) and Tax Information Network.

Consider the math behind the surcharge structure. If your taxable income breaches 50 Lakhs INR, a flat 10% surcharge is levied on your total calculated income tax. When your income crosses 1 Crore INR, this surcharge leaps to 15% under both the traditional and modern revised tax frameworks. Let T represent your base income tax calculated via standard slabs. The actual tax liability L is calculated as:

L = T × (1 + S) × (1 + H)

Where S represents the surcharge rate (0.10 or 0.15) and H represents the mandatory Health and Education Cess of 4% (0.04). When S = 0.15, your effective peak marginal tax rate climbs significantly above the nominal 30%, maxing out at 35.6% or 39% depending on the chosen regime and income bracket. This fiscal drag means that for every marginal rupee generated through your professional practice, corporate leadership role, or business operations, nearly 40 paise is automatically reallocated to the state before it can touch your investment accounts.

Furthermore, the moment your total income exceeds 50 Lakhs INR, you are legally obligated to disclose your entire balance sheet to the Income Tax Department via Schedule AL of the Income Tax Return (ITR) form. This requires an exhaustive inventory of your immovable properties (land, commercial, and residential real estate) along with moveable assets, including the exact cost price of your equity portfolios, mutual funds, corporate cash balances, insurance policies, and physical gold or jewelry. The state transforms your financial life from a private notebook into a fully transparent digital asset map, exposing you to higher regulatory compliance risks and the psychological stress of potential audits.

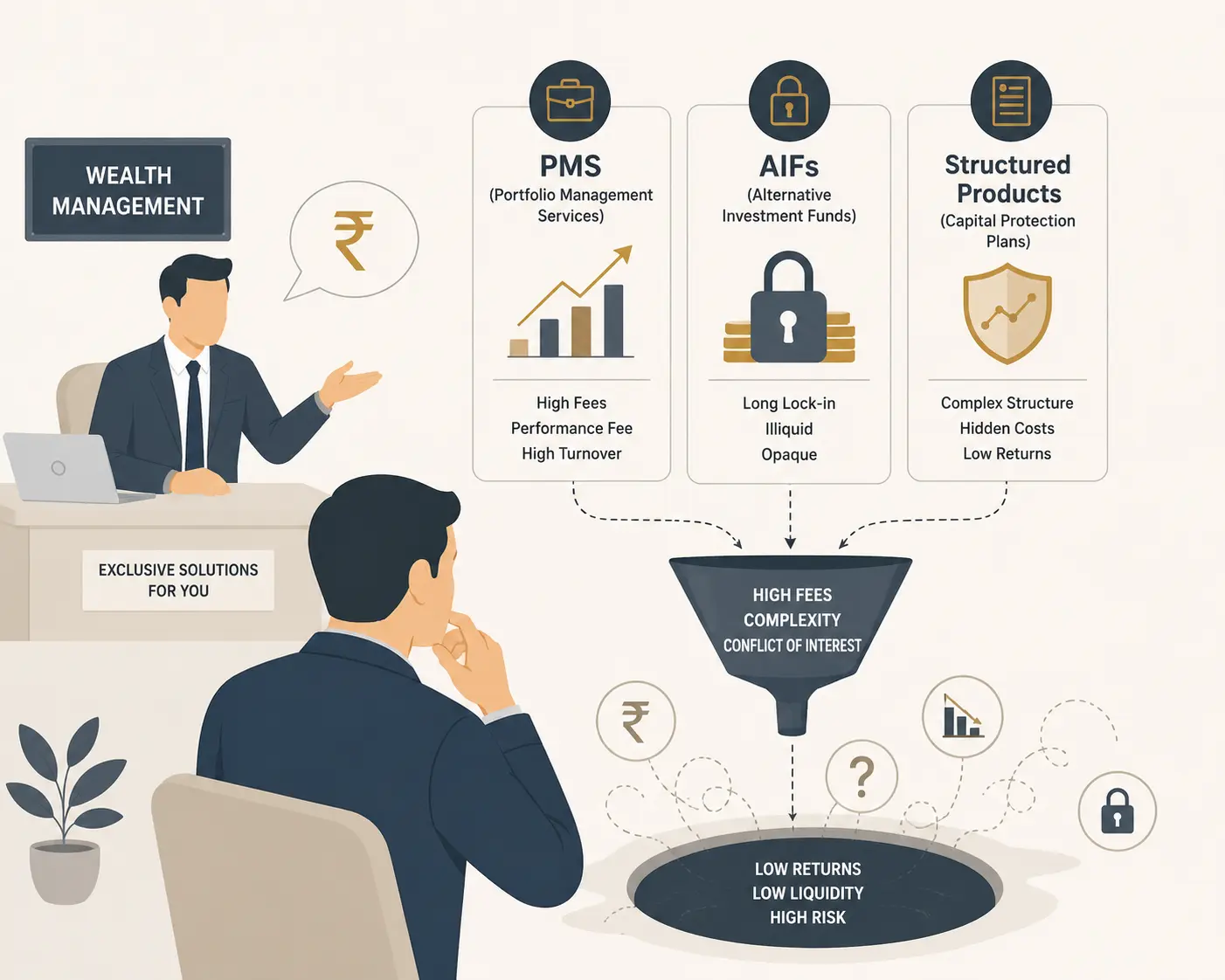

Institutional Mis-selling: The Advisory Trap and Manufactured Complexity

In our reference analysis of financial tools, we noted that relying entirely on automated algorithms can lead to unexpected errors due to a lack of deep, human-centric situational awareness. In the wealth management industry, an even more dangerous dynamic occurs: human financial advisors weaponize complexity against you the moment they identify you as a High-Net-Worth Individual (HNWI). When your liquid capital or visible equity portfolio crosses the 1 Crore mark, your name enters a highly synchronized, institutional database of affluent individuals. Your regular relationship managers at tier-1 banks stop offering basic fixed deposits or standard mutual fund SIPs. Instead, you are aggressively transitioned to the elite "Wealth Management Wing." Here, your capital becomes the target of high-fee financial engineering designed to extract maximum commissions for the institution rather than maximum returns for your family. The core mechanism of this advisory trap relies on three highly profitable investment vehicles:

-

Portfolio Management Services (PMS): These services demand a minimum ticket size of 50 Lakhs INR. They are marketed as highly personalized, elite alternatives to mutual funds that can beat the market. In reality, a large percentage of PMS structures charge high fixed management fees (typically 1.5% to 2.5% per annum) plus a significant share of performance profits (often 15% to 20% of gains above a specific hurdle rate). When you factor in short-term capital gains tax triggered by high portfolio turnover rates, the net return to the investor frequently underperforms a simple, low-cost index fund.

-

Alternative Investment Funds (AIFs): Requiring a minimum investment threshold of 1 Crore INR, AIFs look like exclusive private equity or long-short hedge funds. They feature complex legal structures, lock-in periods of 3 to 7 years, and deep capital call schedules. While they promise uncorrelated structural alpha, they often expose the neo-rich to highly illiquid, opaque developer debts or speculative startup equity that can take years to unwind.

-

Structured Products and Capital Protection Plans: These are complex derivative-linked instruments tied to equity indices or bond yields. They are engineered to look completely secure while offering upside exposure. In practice, the internal costs are hidden within the derivative pricing structures, leaving the client with sub-par risk-adjusted returns while the issuing bank pockets large upfront structuring fees.

"The ultimate paradox of modern Indian wealth is that as your balance sheet expands, the financial industry works harder to make your money complicated, illiquid, and expensive. True wealth protection requires resisting manufactured complexity."

The Lifestyle Inflation Engine: Keeping Up with the 'Neo-HNWIs'

Wealth is not merely an isolated mathematical metric; it is deeply tied to social positioning and your peer group. In India, crossing a net worth of 1 Crore often triggers an unconscious shift in your reference group. You move away from the hyper-frugal, value-conscious middle class and enter the world of competitive, luxury-driven consumption—a phenomenon known as the Neo-HNWI Lifestyle Trap. When you achieve this level of wealth, your baseline expectations for everyday services change completely. This structural shift can be mapped across four distinct categories of personal spending:

| Expense Category | Middle-Class Baseline (Value-Driven) | Neo-HNWI Shift (Status-Driven) | Hidden Real Cost & Structural Drag |

|---|---|---|---|

| Primary Housing | Functional 2-3 BHK in an urban suburb (frugal, stable maintenance costs) | Premium gated community, luxury township with high-end club membership | High monthly maintenance charges (₹10,000–₹30,000), steep property taxes, and massive interior decoration costs |

| Vehicles & Mobility | Reliable Japanese/Korean compact SUV or sedan focused on mileage and resale value | Entry-level European luxury brands (German trio) or premium SUVs | Rapid asset depreciation (20-30% in year one), expensive maintenance visits, and high comprehensive insurance premiums |

| Childhood Education | Reputable regional or national curriculum schools (CBSE/ICSE) with predictable fees | Elite International Schools offering the IB or Cambridge pathway | Annual fees scaling from ₹4 Lakhs to ₹12 Lakhs per child, plus expensive international field trips and social networking events |

| Leisure & Socializing | Domestic vacations and occasional dining out at popular family venues | Bi-annual international long-haul vacations, fine dining, and curated lifestyle club memberships | High expenditure per trip (₹5–₹10 Lakhs), driven by premium air travel, luxury resorts, and high status-driven consumption |

Advertisement

This upward shift in consumption is driven by the human desire for social validation and peer alignment. When you move into a luxury apartment complex where your neighbors drive premium vehicles and send their children to elite international academies, your baseline definition of a "normal lifestyle" changes. This structural lifestyle inflation locks you into high fixed monthly costs. It creates a situation where, despite having an eight-figure net worth, your cash flow remains tight. You find yourself trapped on a premium treadmill, forced to constantly work harder just to maintain your new standard of living.

The Indian Family Tax: Wealth Redistribution Expectations

In the socio-cultural landscape of India, wealth accumulation is rarely treated as a purely individual achievement. Because of our deep history of collectivism and extended family networks, individual financial success often brings unwritten family obligations. This dynamic can be thought of as the "Indian Family Tax"—a series of financial expectations that emerge the moment your extended network realizes you have achieved significant wealth. When you cross the 1 Crore net worth mark, you become the default financial anchor for your extended family. This brings a variety of unwritten capital demands that are very difficult to refuse due to cultural and social expectations:

1. The Zero-Interest Emergency Loan: You become the first point of contact for extended family members facing medical emergencies, business downturns, or personal cash flow crunches. These loans are rarely backed by formal legal agreements or structured repayment schedules. Culturally, asking for your money back can create lasting friction within the family, meaning these loans often turn into uncollectible, interest-free capital grants that quietly reduce your net wealth.

2. Subsidizing Shared Family Events: From massive family weddings to milestone anniversary celebrations and religious ceremonies, you are naturally expected to shoulder a disproportionate share of the costs. While less affluent family members contribute via physical help and coordination, you are expected to provide the actual capital for venue bookings, high-end catering, and expensive gifts, creating a steady drain on your liquid savings.

3. Funding the Next Generation: You will often face subtle or direct requests to fund the aspirations of nieces, nephews, or cousins. This can include financing expensive coaching classes for competitive exams, subsidizing international postgraduate tuition, or providing the seed capital for a relative's new business venture. Refusing these requests can cause you to be viewed as self-centered or disconnected from the family, creating an emotional tax that tests your boundaries and financial discipline.

The Illiquidity Illusion: The Paper Crore vs. Cash Reality

The final and most dangerous side effect of hitting a 1 Crore net worth in India is the structural illusion of wealth itself. Many people reach this milestone on paper without realizing how fragile and illiquid their asset allocation actually is. In the modern Indian economy, it is very common to find "paper millionaires" who are asset-rich but cash-poor, leaving them highly vulnerable to sudden market shifts or personal financial emergencies. This vulnerability stems from an unbalanced asset allocation that is heavily weighted toward two specific classes:

The Real Estate Concentration Trap: A large percentage of newly affluent Indians cross the 1 Crore threshold simply because the market value of their primary residence or an ancestral plot of land has surged. If 75 Lakhs of your 1 Crore net worth is locked up in the apartment you live in, your true financial runway is incredibly small. Real estate is inherently illiquid. You cannot easily sell off a single bedroom to cover an immediate medical emergency or a sudden business crisis. Selling property in India also involves complex capital gains tax calculations, long negotiation cycles, and high transaction costs, making it a poor source of emergency liquidity.

The Paper-Profit Equity Euphoria: For others, their eight-figure net worth is built on a roaring bull market, driven by highly inflated mid-cap and small-cap stock portfolios or unvested corporate ESOPs (Employee Stock Ownership Plans). These paper valuations can look highly impressive on a digital dashboard. However, they remain exposed to sudden market corrections, sector-specific downturns, or strict corporate vesting schedules. Until those gains are systematically locked in, structured into stable income-generating assets, and insulated from market volatility, your 1 Crore net worth is a variable projection rather than a permanent financial reality. Without adequate cash flow and liquid reserves, a paper millionaire can easily be forced into high-interest debt or a painful financial crunch by a single prolonged emergency. This reveals the core truth: true financial resilience is determined by your liquid cash flow and asset accessibility, not just the total figure at the bottom of your balance sheet.

"True financial freedom is not defined by an arbitrary eight-figure number on a digital screen. It is found in liquid resilience, clear emotional boundaries, and the discipline to resist status-driven lifestyle inflation."

Conclusion: Navigating the Eight-Figure Realities with Discipline

Crossing the 1 Crore net worth milestone is an undeniable achievement in an individual's financial journey, representing hard work, dedication, and long-term planning. However, avoiding the hidden len traps of this new status requires moving beyond simple accumulation. You must develop a deep awareness of the structural shifts that come with wealth. To successfully preserve your wealth across generations in India, you must actively manage these invisible costs. This means building a highly optimized tax plan to handle surcharges, setting clear financial boundaries with your extended family, and maintaining a healthy skepticism toward complex, high-fee wealth management products. Most importantly, it requires the self-discipline to resist the pressure of lifestyle inflation, ensuring that your rising net worth translates into true, lasting freedom rather than just a more expensive, stress-filled lifestyle. By treating wealth management as an ongoing practice of mindfulness and intentional planning—much like the timeless principles of the traditional Kakeibo method—you can ensure that your financial success serves as a true foundation for personal liberty, rather than becoming a golden cage of hidden costs and endless obligations.

Read Further

[1] SEBI Investor Education Programme. Portfolio Management Services (PMS) — Regulations, Minimum Investment, Fees, and Investor Rights — Click here

[2] Income Tax Department, Government of India. Income Tax Act — Schedule AL: Assets and Liabilities Disclosure Requirements for Incomes Above ₹50 Lakhs — Click here

Disclaimer: The analytical data, structural insights, and statutory tax provisions outlined in this report are compiled from current public fiscal policies and macroeconomic studies on wealth demographics within India. This document is intended solely for educational and informational purposes and must not be construed as formal legal, tax, or investment advice. Capital allocations and wealth planning decisions should be executed in consultation with qualified, independent professionals.

Advertisement