In today's highly advanced and mechanized economic ecosystem, we often deceive ourselves into thinking we have outgrown the whims of nature. We depend heavily on automated forecasting, data modeling, and predictive algorithms to build our corporate structures. Yet, when the skies refuse to break and the clouds withhold their bounty, we are suddenly reminded of a timeless vulnerability. The Indian subcontinent is facing exactly this reality in the summer of 2026. A massive climate shift is underway, driven by an unyielding El Niño pattern that has locked its grip on the equatorial Pacific Ocean.

According to the latest June bulletin from the India Meteorological Department (IMD) and verified global data from the World Meteorological Organization (WMO), the transition from neutral conditions to an active El Niño is now fully established with a striking 99.4% probability persisting through the latter half of the year. The early numbers are already painting a challenging picture: by late June, the nation recorded just 45.6 mm of rainfall against the seasonal long-period average of 84.4 mm, creating an immediate and alarming 46% national deficit. This isn't just a minor meteorological variance; it is a profound macroeconomic disruption that will ripple through corporate balance sheets, agricultural output, and consumer sentiment across the country.

Critical Risk Highlights: El Niño 2026 Status

- Rainfall Deficit: A 46% shortfall recorded in the early weeks of the monsoon cycle, leaving major agricultural belts under severe moisture stress.

- Regional Vulnerability: The National Stock Exchange (NSE) reports the highest probability of below-normal rainfall in Northwest India at 46%, followed closely by the South Peninsula at 45% and Central India at 43%.

- Macro Recalibration: Leading global agencies like S&P Global Ratings have already adjusted India's FY27 GDP growth projections downward to 6.6%, a stark contrast from the 7.7% growth achieved in FY26.

Macroeconomic Perspective: Squeezing the Rural Engine

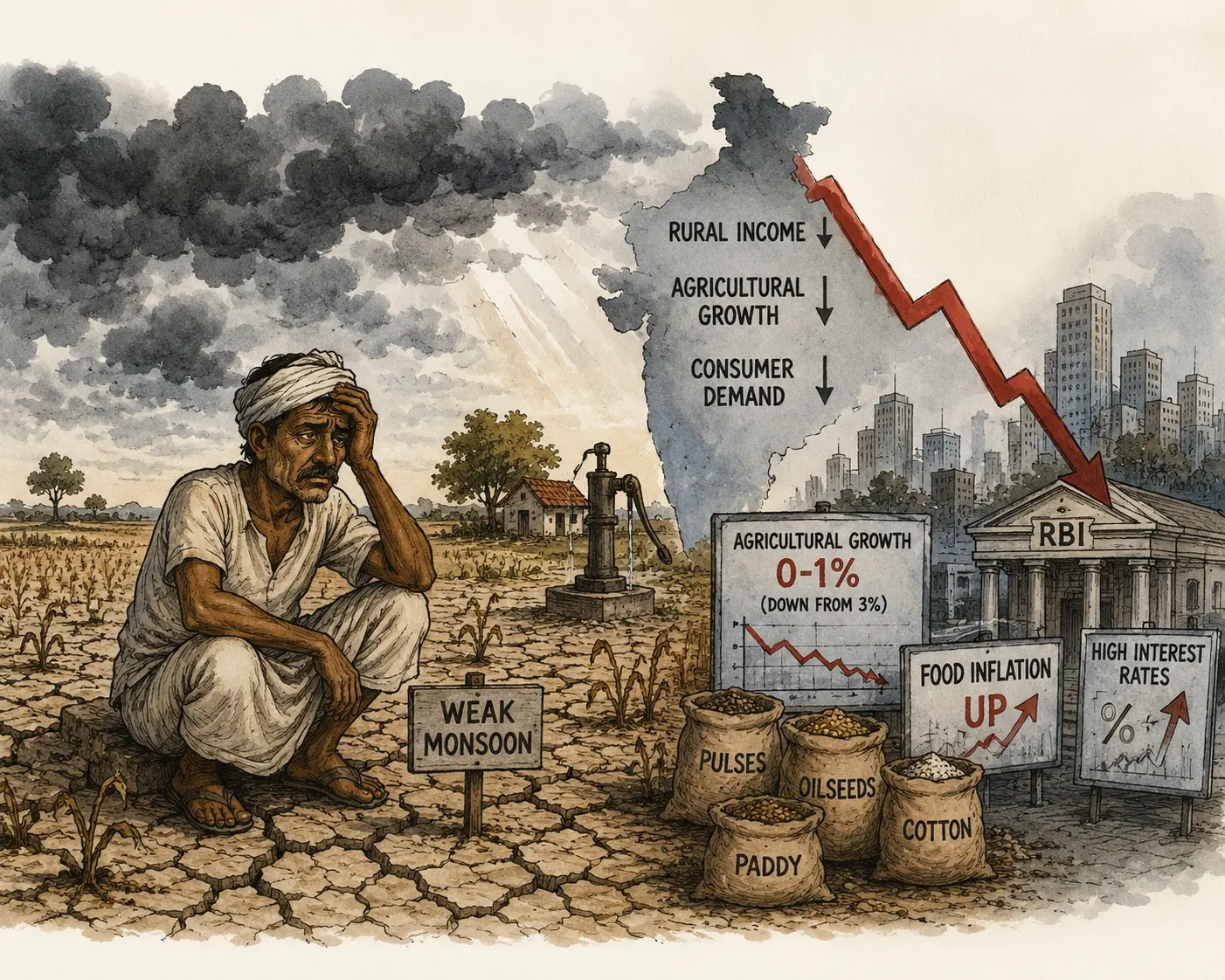

To fully comprehend why a weak monsoon sends shockwaves through the Indian corporate landscape, one must look directly at the underlying anatomy of the domestic economy. Nearly 16% of India's GDP remains directly tied to agriculture, but more importantly, over 46% of the country's entire workforce relies on the rural sector for their livelihood. When 70% of the year's total precipitation is packed into a volatile four-month southwest monsoon window, any structural failure in these rains acts as a direct tax on rural disposable income. The immediate consequence is a double-edged sword of energy stress and sub-par agricultural growth. Economists project that agricultural growth could collapse to a mere 0-1% for the fiscal year, down significantly from the stable 3% seen previously. As water reservoir levels plummet to historical lows, the sowing of critical kharif crops — specifically paddy, pulses, oilseeds, coarse cereals, and cotton — is experiencing a heavily subdued start. This structural deficit sets off a chain reaction: lower crop yields feed directly into higher food inflation, forcing the central bank to maintain elevated interest rates, which in turn compresses overall domestic demand and drives up the cost of capital.

"When you strip away the digital infrastructure of modern commerce, you find that the velocity of rural money is entirely tied to the depth of the topsoil moisture. A dry monsoon means a dry pipeline for consumer demand."

The Sufferers: Sectors Bearing the Brunt of the Deficit

A subpar monsoon creates clear structural headwinds for specific corporate segments that depend heavily on rural consumption, agricultural capital expenditure, and predictable harvesting cycles.

A. Fast-Moving Consumer Goods (FMCG) and Rural Staples

The core engine of volume growth for India's largest consumer goods companies is rooted deeply in rural villages, which historically contribute between 35% to 50% of total everyday-goods volumes. Listed behemoths like Hindustan Unilever (HUL), Dabur, Marico, Colgate-Palmolive, Jyothy Labs, and Emami are heavily exposed to these dynamics. When farm incomes stall due to crop failure or delayed harvests, rural consumers instinctively pivot toward essential survival purchases, abandoning discretionary, branded, or higher-margin products. Compounding this problem is the reality of rising input costs. A weak monsoon inevitably triggers an upward spiral in the prices of raw agricultural inputs like oilseeds, sugar, and grains. FMCG companies are trapped in a vice: they face suppressed volume growth on one hand and escalating raw material costs on the other, forcing margin compression or unpopular price hikes that further alienate a struggling consumer base.

B. Automotive: Tractors and Entry-Level Two-Wheelers

The automotive industry experiences a severe bifurcation during a weak monsoon year. The rural transport and farming segments act as direct barometers of agricultural health. Roughly two-fifths of all motorcycle demand originates from rural areas, where entry-level two-wheelers are treated as essential utility vehicles rather than luxury statements. When agricultural incomes slip, upgrades and replacement cycles are immediately delayed or cancelled entirely. The situation is even more pronounced for tractor manufacturers and agro-machinery providers. Tractors represent a major capital investment for a rural household, a decision that relies entirely on a confident multi-season financial outlook. With falling disposable income and rising fuel overheads, asset replacement is pushed down the line, leading to significant inventory pile-ups at dealerships and sharp drops in monthly dispatch volumes for major manufacturing lines.

C. Agricultural Inputs: Agrochemicals, Seeds, and Fertilizers

One might assume that a lack of rain would force farmers to buy more chemical protections, but the operational reality is quite different. Delayed monsoons distort the traditional buying calendar, pushing critical input sales from the first quarter into late the second quarter. This adds immense inventory carrying costs to fertilizer and seed distributors. Furthermore, if a farmer believes a crop is likely to fail due to water scarcity, they will actively cut down on high-cost crop protection products and premium seeds to minimize their total capital risk, hitting the top lines of specialized chemical providers.

D. Rural Financial Institutions and NBFCs

The health of rural credit and microfinance institutions is intrinsically tied to the harvest calendar. Repayment schedules for agricultural loans are tightly synchronized with the selling cycles of kharif and rabi yields. When a monsoon fails, the immediate casualty is the collection efficiency of rural lenders. Bad-loan stress and non-performing assets (NPAs) begin to surface a few quarters down the line. To mitigate this risk, lenders are forced to tighten credit availability, which inadvertently chokes off local economic activity and deepens the cyclical downturn.

The Beneficiaries and Resilient Segments

While a weak monsoon presents undeniable challenges across the broader economic canvas, it simultaneously creates distinct operational demand and capital allocation shifts that structurally favor alternative sectors.

A. Water Management, Irrigation, and Piping Systems

When natural precipitation fails, artificial water transportation becomes an immediate and critical national priority. A severe deficit in rainfall forces agricultural enterprises, regional administrations, and industrial complexes to invest heavily in groundwater extraction, drip irrigation systems, and extensive water transportation pipelines. Companies involved in manufacturing PVC/CPVC pipes, industrial pumps, and advanced micro-irrigation systems experience a substantial surge in demand as the country scrambles to preserve crop yields and secure drinking supplies.

B. The Power and Energy Grid

A weak monsoon is almost always accompanied by prolonged periods of extreme heat and suppressed cloud cover, pushing daytime and nighttime temperatures well above historical averages. This creates an immediate, massive surge in power consumption across both urban residential centers and rural agricultural pumps. Urban areas experience an unprecedented spike in air conditioning and cooling demands, while rural regions require continuous, heavy electrical loads to power tube wells and groundwater pumping systems to replace missing rainwater. Utilities and power generation companies find themselves operating at maximum load factors, driving up merchant power prices and boosting short-term utility revenues.

C. Premium Urban Consumption and Insulated Global Exports

A crucial trend in modern economic analysis is the clear decoupling of urban premium luxury consumption from rural agricultural cycles. While entry-level two-wheelers and mass-market staples feel the pinch of a weak monsoon, high-end discretionary spending remains remarkably insulated. Luxury automobile sales, premium real estate, high-end retail, and elite hospitality services are supported by a booming corporate sector, robust services industry, and affluent urban demographics whose incomes are completely detached from farm output. Similarly, export-oriented sectors like Information Technology (IT) services, specialized software development, and pharmaceutical manufacturing remain entirely unaffected by domestic weather volatility. These industries derive their revenues from international markets, capitalizing on global corporate spending and structural cost advantages rather than domestic consumer demand. For investors looking to shelter capital during a domestic climate shock, these outward-facing sectors serve as natural, highly stable hedges.

Sectoral Revenue Impact Summary Matrix

| Sector | Classification | Impact |

|---|---|---|

| FMCG (High Rural Exposure) | Vulnerable | Anticipated 15-20% slowdown in volume growth if moisture deficits persist beyond July. |

| Auto (Tractors & Entry 2W) | Sufferer | Postponed replacement cycles leading to margin pressures and rising dealer discounts. |

| Irrigation & Infrastructure | Beneficiary | Heightened demand for efficient water deployment and deep-well delivery systems. |

| Power Utilities | Beneficiary | Peak power deficits drive merchant electricity pricing higher amidst relentless heatwave conditions. |

| Global IT & Pharma | Highly Resilient | Complete insulation from localized rainfall deviations with performance guided strictly by international macro indicators. |

Strategic Outlook and Mitigation

Navigating an economy disrupted by an active El Niño requires a fundamental shift in perspective — moving away from traditional reactive practices toward structural, built-in resilience. The challenges of 2026 clearly highlight that relying purely on historical averages is a flawed approach to capital allocation and corporate planning. Sophisticated market participants and enterprise leaders must construct their strategies around structural adaptation, recognizing that weather anomalies are increasingly becoming structural realities rather than temporary exceptions. For corporations, this means building deep supply-chain flexibility and diversifying geographic revenue distributions to ensure that localized climate shocks cannot completely derail operational continuity. For the broader economy, it underscores the critical urgency of accelerating structural investments in water security, micro irrigation networks, and climate-resilient agricultural technologies. Ultimately, those who look beyond short-term challenges to recognize these changing structural patterns are the ones who will successfully protect their operations and capture emerging opportunities in an increasingly volatile landscape.

Read Further

- S&P Cuts India FY27 Growth Forecast to 6.6% on Energy Stress, Weak Monsoon — Business Standard, June 2026

- Why Is Monsoon Stuck? 5 Reasons Behind the 43% Rainfall Deficit This June — BusinessToday, June 2026

Disclaimer: All the structural data, climate insights, and corporate breakdowns provided in this strategy report were compiled from verified public internet resources, institutional research briefs, and historical macroeconomic studies. This document is intended solely for informative and educational purposes and must not be interpreted as definitive financial advice, corporate directives, or an official investment quote from our publication.