In today's era where everything is being digitized and automated by modern systems, we are too much dependent on formalized retail and banking architectures. Somehow it is useful for us who belong to the middle and upper tiers of society, and somehow it is completely broken for those at the bottom of the pyramid. Modern supply chains and financial markets were engineered to bring structural efficiency, but when we end up relying purely on capital-intensive algorithms and corporate frameworks for resource distribution, we don't know where we actually forgot the basic socioeconomic realities of the micro-economies that sustain over half of India's population. We don't know.

So this article basically is going to get you all aware about what is actually happening in the deep corridors of Indian local retail markets, financial networks, and daily wage structures. It will uncover what we should do with modern economic designs to bridge this devastating systemic gap, and what we must understand about the raw, harsh traditional realities of the "Poverty Premium" — the invisible structural tax that forces poor households to pay significantly more per unit for basic survival commodities, utilities, credit, and services than the wealthy.

The Structural Mechanism of the Poverty Premium and the Efficiency of Bulk Arbitrage

When we look at the financial setups of modern Indian metropolitan areas, a stark contrast emerges between supermarket baskets and local slum vendor purchases. The wealthy buy in bulk, securing steep volume discounts and cashbacks. The poor, constrained by erratic daily cash flows, must buy things in the absolute smallest quantities available. This introduces a structural mathematical penalty known as the packaging and distribution premium. In the micro-retailing ecosystem of suburban shantytowns and rural outposts, FMCG manufacturers pack items into microsachets or small plastic bags — whether it is edible oil, shampoo, tea leaves, or milk. This micropackaging adds substantial material and labor overheads per unit of volume, which is passed entirely down to the buyer.

"Buy daily to survive today, pay twice as much by tomorrow."

In a recent economic analysis of urban consumer clusters in Mumbai and Delhi, a massive variance was observed when comparing the unit prices of daily essentials purchased by low-income daily-wage workers against standard monthly packages bought online or at large supermarket chains. For instance, a 5ml sachet of premium shampoo or a 10g packet of blended spices carries an effective markup of up to 45% to 65% per liter or kilogram when compared to a standard 1-liter bottle or 1-kg container. This calculates to an alarming metric: every 2nd out of 5th rupee spent by a low-income household on basic consumables is entirely lost to structural overheads and fragmented supply chains, which leaves a devastating error in their micro-budgeting efforts. If this pattern remains unaddressed in household or personal expenses, it quietly drains the financial viability of our most vulnerable workforces, pulling them into heavy lifelong losses from which they can never truly recover.

| Commodity / Service | Low-Income Procurement (Sachet / Daily) | Affluent Procurement (Bulk / Monthly) | Effective Premium / Markup Paid by Poor |

|---|---|---|---|

| Edible Oil (Mustard/Palm) | ₹15 to ₹20 per 100ml pouch | ₹125 per 1L PET bottle | 20% – 28% Premium |

| Shampoo / Toiletries | ₹2 per 5ml sachet | ₹280 per 650ml pump bottle | 50% – 65% Premium |

| Informal Credit / Loans | 10% per month (Local Money Lender) | 11.5% per annum (Personal Bank Loan) | Over 900% Relative Interest Spread |

| Drinking Water Delivery | ₹5 per 15L jerrycan (Unsafe) | ₹0.04 per L (Municipal/RO Infrastructure) | 300% – 500% Infrastructure Penalty |

| LPG Cooking Fuel | ₹30–₹40 per day (Coal/Wood/Small Cylinder) | ₹850–₹950 per 14.2kg subsidized cylinder | 35% Alternative Fuel/Health Overhead |

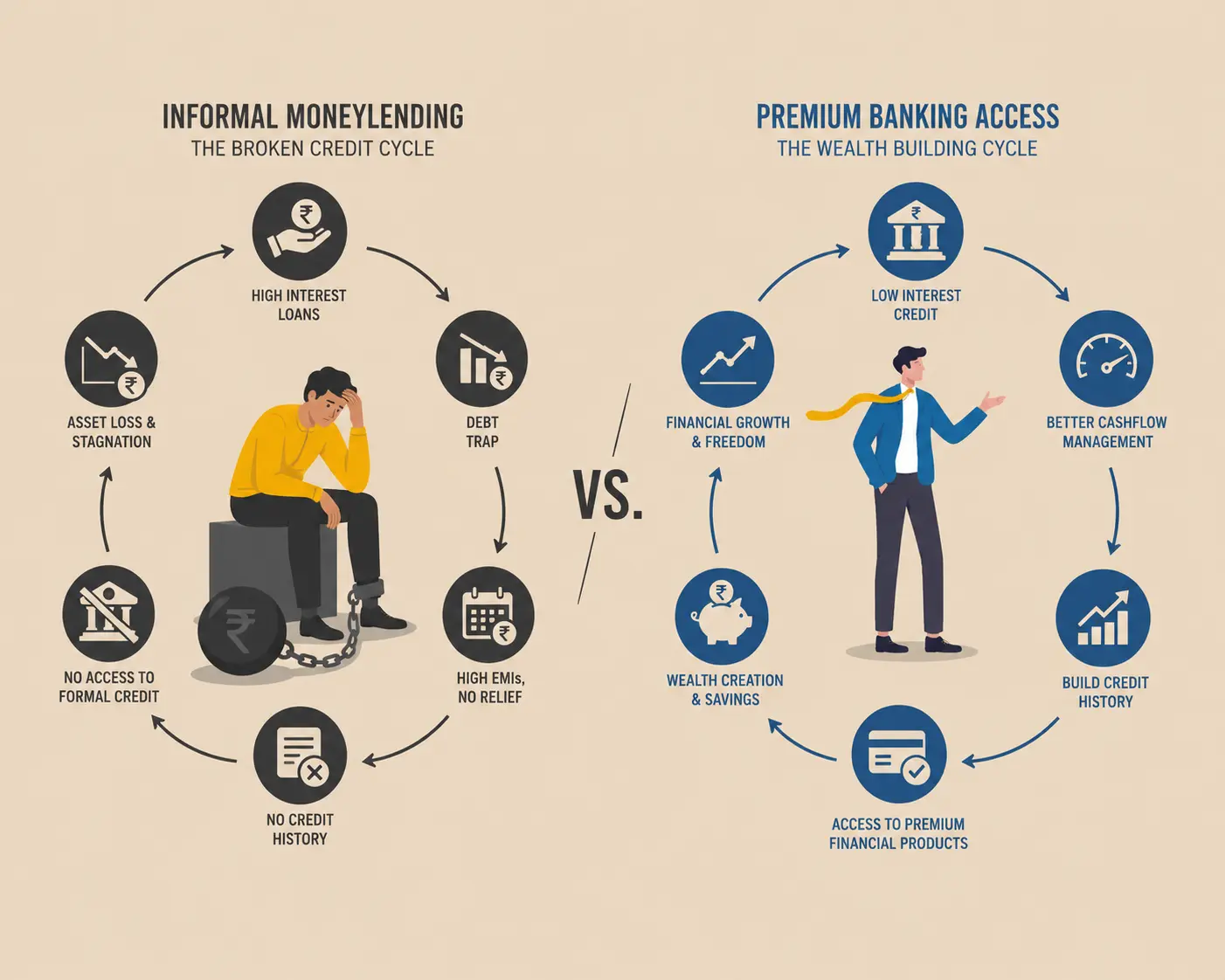

The Broken Credit Cycle: Informal Moneylending vs. Premium Banking Access

The financial infrastructure of formal institutions remains deeply biased toward capital density. For an affluent citizen, accessing credit is a seamless loop driven by automated underwriting algorithms, high credit scores, and collateralized assets. They secure home loans at 8.5% per annum or personal credit lines at 12%. However, for a street vendor or a construction laborer without standard document stacks, formal bank doors remain tightly shut. This complete institutional failure forces them back into the grip of local informal moneylenders, chit funds, or exploitative daily-finance rings operant within local mandis and urban slum colonies. The operational mechanics of these informal lending networks are brutally straightforward. A vendor borrows ₹1,000 in the morning to purchase fresh vegetables from the wholesale market, and must return ₹1,100 by the evening. This is a seemingly small ₹100 fee, but when calculated as an Annual Percentage Rate (APR), it amounts to an astronomical and mathematically impossible rate of over 3,600%. Giving up their hard-earned daily profits to service these micro-debts becomes an endless loop of compounding poverty. Constantly running to keep up with these short-term liabilities becomes a tiresome, exhausting chore of the day, draining mental bandwidth and causing severe psychological stress, migraines, and long-term health issues within these communities.

Advertisement

"The poor man's credit is a daily lease on his own physical labor."

Infrastructure Failure and the Indirect Overheads of Basic Public Utilities

The poverty premium is not merely confined to commercial products and informal financial debts; it is deeply embedded within our broken urban infrastructure. In major Indian tier-1 and tier-2 cities, affluent neighborhoods enjoy subsidized piped municipal water supply and stable electrical grids with structured slab billing. Conversely, unauthorized colonies, slums, and urban villages are completely cut off from formal utility lines. This institutional gap creates a massive parallel black market where the poor are forced to buy basic survival items like drinking water from private tanker mafias or local purifying shops at highly inflated rates. A household in a low-income settlement pays anywhere between ₹5 to ₹10 for a single 20-liter jerrycan of water. When you scale this cost to match the monthly consumption volume of an upper-middle-class apartment, the poor end up paying nearly four to five times more for a lower grade of unverified water. This water often carries biological contaminants, leading to water-borne illnesses, which further exposes them to the exploitative private healthcare ecosystem. Because public clinics are perpetually understaffed or lack essential medicines, these families have to buy expensive medicines out-of-pocket from local pharmacies, losing multiple days of wages. This is an invisible, compounding drain that operates quietly, away from corporate statistics and macroeconomic models.

Digital Exclusion and the Mirage of Cashbacks and Fintech Efficiency

With the rapid expansion of unified payment interfaces and e-commerce apps, the Indian middle class enjoys an unprecedented era of optimized personal finance. From digital discount coupons, zero-cost EMI cards, and fuel rewards to dynamic app cashbacks on grocery apps, the system rewards capital density with continuous compounding cost reductions. If you have a solid bank balance, the technology saves you money automatically. But for someone whose entire liquidity is bound to paper cash and daily physical collections, this entire ecosystem becomes an invisible barrier that excludes them from these savings. The daily wage worker can never participate in flat 20% online grocery discounts because they lack the necessary upfront liquidity to purchase a month's worth of goods at one go. Furthermore, smartphone data plans are frequently purchased in expensive, short-term daily vouchers rather than optimized annual bundles, adding another 30% premium on basic digital access. The system is designed such that the smaller your pocket, the higher the structural frictional cost to spend each rupee. This is the tragic paradox of modern Indian consumerism: those who have the least money are forced to pay the highest real price to keep their households running from day to day.

"Capital density unlocks optimization; structural liquidity scarcity invites systemic exploitation."

Strategic Remediation: Redesigning Financial and Retail Architecture for Equity

To dismantle this predatory structure, Indian economic planners, FMCG conglomerates, and financial technology developers must fundamentally reimagine their operational systems. We cannot rely on traditional trickle-down economic logic to resolve a problem deeply rooted in structural distribution design. First, micro-credit architectures must be integrated with localized public digital infrastructure. By leveraging data from public distribution schemes and local trade associations, micro-loans can be underwritten based on cash-flow consistencies rather than formal collateral, breaking the monopoly of high-interest informal moneylenders. Second, consumer goods manufacturers must redesign their micro-packaging models. Instead of single-use multi-layered plastic pouches that impose a heavy unit cost penalty and create massive environmental waste, corporate entities should collaborate with local Kirana stores to install automated bulk-refill dispensing kiosks. This allows a customer with a tight daily budget of ₹20 to purchase edible oil or liquid soap at the same exact per-liter bulk rate as an affluent buyer purchasing a 5-liter container. This simple alteration can immediately shift consumption patterns from reactive survival to intentional saving, which is the core principle of long-term financial success and community wealth building.

Read Further

- Reserve Bank of India — National Strategy for Financial Inclusion 2019–2024: Addressing Structural Barriers to Credit and Banking Access

- The Poverty Premium in India: How Low-Income Households Pay More — NITI Aayog / NCAER Consumer Expenditure Research, Ministry of Statistics and Programme Implementation (MoSPI)

Disclaimer: All the data and analytical points provided above were derived from Indian economic research studies, consumer market surveys, and public finance reports examining the poverty premium across developing nations. This analysis is presented for educational and conceptual purposes and should not be taken as formal economic advisory or an institutional quote from our website.

Advertisement