If you follow the global economy even casually, you probably know that the old playbooks for investing in Western markets are feeling pretty worn out these days. For a long time, the strategy for big private equity firms was straightforward: lean on mature markets like the US or Europe, use plenty of cheap debt, and wait for valuations to climb. But that world has changed. We are looking at a landscape of persistent structural shifts, regulators who are much more eagle-eyed than they used to be, and a long-running argument over whether those high valuations ever really made sense. Plus, with interest rates staying higher for longer, the old trick of using massive leverage to juice returns just isn't working the way it did ten years ago.

This shift is forcing the world's biggest funds to rethink where they actually put their money. When you are managing billions, you can't just sit on your hands; you have to find places where the wind is actually at your back. You need a combination of a steady economy, a legal and structural framework that won't fall apart, and companies that are big enough to actually move the needle when you take an active role in running them. This explains why EQT Asia recently made a very public and very deliberate point of naming India as its number one priority for the coming year. This isn't just the kind of thing a CEO says to be polite during a press junket in Delhi. It represents a massive pivot in where capital is flowing. It's a signal that the real opportunity for outsized returns has moved to a new center of gravity.

To understand why this matters, you have to look at how private equity itself has changed. It used to be about making lots of small, fragmented bets on growth. Now, the big players want control. They want to buy whole companies and run them according to a specific industrial philosophy. EQT is a perfect example of this. They carry the DNA of the Swedish Wallenberg family, which means they tend to think like industrial owners rather than just financial traders. After they merged with Baring Private Equity Asia to create EQT Private Capital Asia, they became a massive force in the region.

By 2026, EQT is managing somewhere around €270 billion in total assets. That makes them one of the biggest private equity platforms on the planet. When a firm of that size decides that one specific country is their absolute top priority, it isn't just a local news story. It's the kind of move that shifts currency values, changes how corporations are structured across the region, and forces every other major institutional investor to rethink their own maps. They aren't just watching the trend; they are effectively creating the new reality of where global money goes next.

The Shift to India and the Strategic Momentum It Provides

When you look at the sheer scale of what EQT is doing right now, the logic behind their heavy tilt toward India starts to make a lot of sense. They recently closed their latest flagship vehicle, BPEA Private Equity Fund IX, at a massive 15.6 billion dollars. To put that in perspective, it is officially the largest Asia-focused private equity fund ever raised. But the raw number only tells half the story. Because of the way they have structured co-investments with their limited partners, EQT is actually looking at a total deployment capacity of over 30 billion dollars across Asia over the next five years. When you are sitting on a mountain of dry powder that large, you cannot just sprinkle it around. You need deep, liquid markets that can actually handle billion-dollar checks without breaking. In the current Asian landscape, that really only leaves you with two major destinations: Japan and India.

Japan is certainly attractive for specific types of deals, like corporate carve-outs or taking public companies private. We saw this recently with EQT's 2.7 billion dollar acquisition of the elevator maker Fujitec. It is a stable, mature environment for that kind of work. However, India offers something different and perhaps more vital for a fund of this size. It is one of the few places globally that combines high secular growth and massive digital shifts with an ecosystem that is finally mature enough to support mid-to-large-cap buyouts. It is no longer just a venture capital playground; it is a serious buyout market.

You can see how serious EQT is by looking at their internal leadership changes. They recently appointed Hari Gopalakrishnan to co-head EQT Private Capital Asia alongside Nicholas Macksey. Hari is the person who essentially built their India private equity practice from the ground up. Taking the person who ran the India desk and putting them in charge of the entire pan-Asian platform is a massive signal. It shows that India has moved from being a satellite office or a secondary allocation to being the actual engine room of the firm's regional strategy. There is a fundamental principle here about spending consciously and saving intentionally, a maxim that applies to the world's biggest sovereign wealth funds and private equity firms just as much as it does to individuals as they look toward the trends of 2026.

This shift in leadership aligns perfectly with their thematic investment framework. EQT isn't interested in spreading money thin across hundreds of speculative, minority venture stakes anymore. They are concentrating their capital into large-cap, control-oriented deals. If you look at their current India portfolio, you see big bets on enterprise applications, tech-enabled services, and healthcare. They have assets like IGT Solutions and AIG Hospitals where they aren't just passive investors. They take control, revamp the governance, bring in CEOs who understand how to use AI, and fund smaller acquisitions to bolt onto the main business. They are essentially taking domestic companies and trying to turn them into global champions through active ownership.

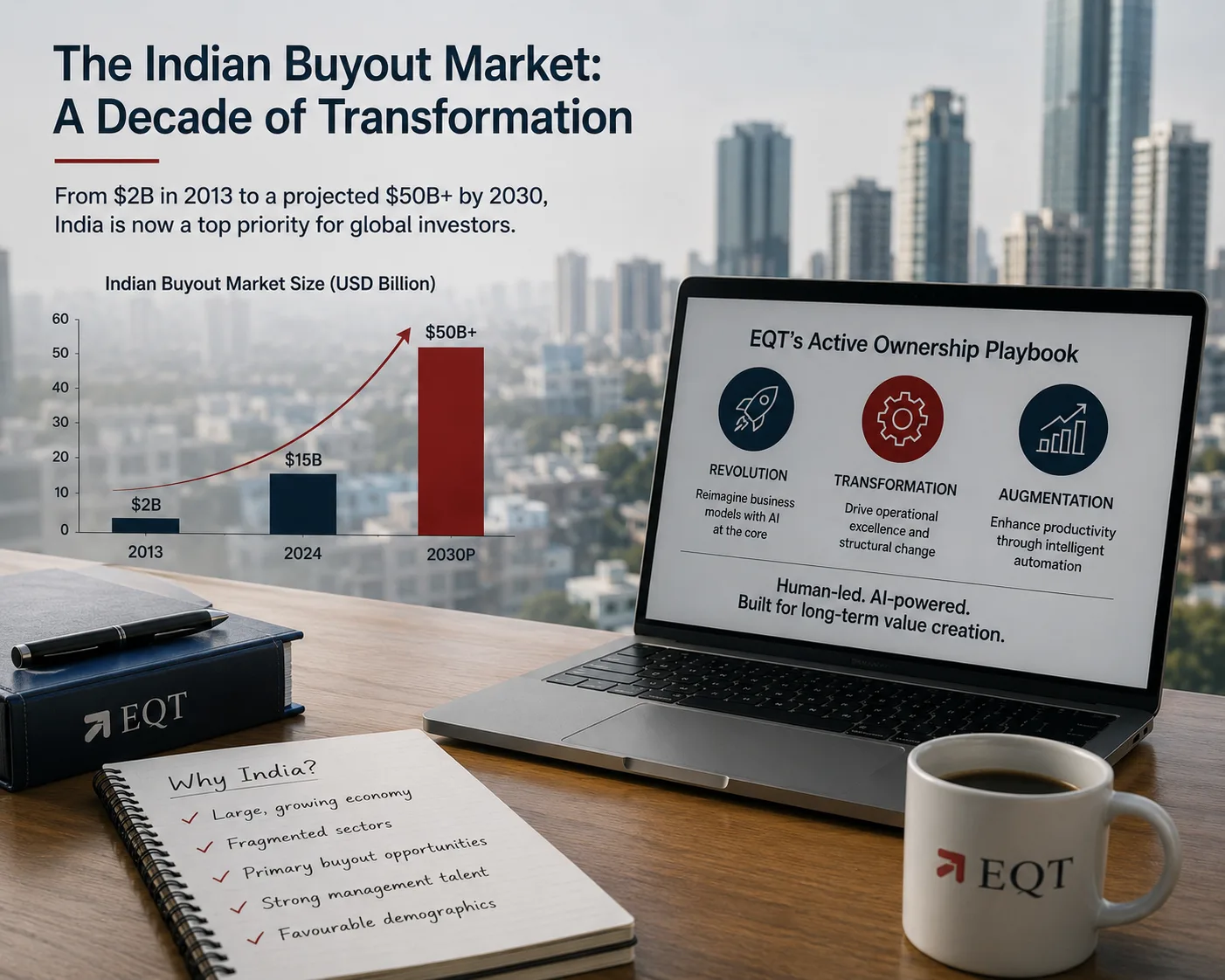

The numbers backing this shift are pretty striking when you look at the trajectory. Back in 2013, the total Indian buyout market was worth about 2 billion dollars. By 2024, that number hit 15 billion, and it is projected to cross the 50 billion dollar mark by 2030. EQT's own fund sizes have followed a similar path, growing from 3 or 4 billion dollars a decade ago to this current 15.6 billion dollar behemoth. Their strategy has evolved alongside the market, moving from minority growth capital into specialized tech and services outsourcing, and now finally into full-scale control buyouts focused on AI-driven transformation. It is a clear evolution from a mid-market focus to a dominant, large-scale regional player.

The Complexities and Risks of Private Equity Over-Concentration

I have been watching the narrative around India lately, and it is certainly a compelling one. The growth numbers are there, and the structural story is hard to ignore. However, when you look at it through a professional financial lens, there is a lot of risk hidden in such a heavy geographic concentration. It reminds me of the common mistake people make with automated systems or AI tools. They get so caught up in the output that they forget to do the manual reflection required to see if those numbers actually make sense in the real world. Global private equity firms are facing a similar institutional trap. If they decide to inject billions of dollars into a single market without meticulously calculating every possible downside, they are asking for trouble.

What we are seeing now is a massive influx of Western capital into India, particularly in the mid-to-large buyout space. This has caused valuation multiples to expand dramatically. It is becoming an incredibly crowded environment where everyone is chasing the same few high-quality targets. When you have that much money competing for the same space, the price goes up regardless of whether the underlying value has increased. It creates a situation where you are paying for perfection, but perfection rarely happens in the real world.

According to recent private equity industry reports, there is a very real challenge surfacing. Automated screening tools are great at finding enterprise targets that look highly profitable on paper. They can crunch the numbers and flag a company in seconds. But the actual execution of a corporate transformation is far more complex than a software program can predict. Many major capital deployments end up with significant execution gaps. Sometimes it is because the initial projections were just too optimistic, and other times it is a total cultural mismatch between the investors and the local management.

When you look at complex integrations that involve multiple geographies or massive tech overhauls, there is almost always a gap between what the investment committee saw in their initial models and what the operational reality looks like a year later. The data shows that nearly two out of every five corporate transformations face major delays or fail to hit their efficiency milestones. Why? Because local regulatory hurdles, labor laws, and supply chain realities in India do not always align with a top-down valuation model designed in an office thousands of miles away. In the investment world, a mistake like that leads to severe margin compression. It is not just a rounding error; it compromises the returns for the entire fund.

Beyond the numbers, there is the human element of operational fatigue. The constant need to screen new targets, perform deep-layered diligence, and stay on top of compliance across a complex local ecosystem can turn into an exhausting loop. You are always tracking something, always correcting something. This places an intense administrative burden on investment teams. Eventually, they hit a wall. Decision-making slows down because the team is spread too thin, trying to manage the sheer volume of details that a simpler market wouldn't require.

For a group like EQT Asia, deciding to make India a top priority means their regional teams are going to be operating under an intense microscope. They will be dealing with the daily grind of managing local currency fluctuations, navigating the nuances of tax law interpretations, and trying to figure out how to successfully exit a domestic investment when the time comes. These are not just line items on a report; they are crucial, labor-intensive daily chores. If they do not maintain a grounded and highly disciplined approach to pricing, and if they do not prioritize deep-rooted human relationships over high-level quantitative growth metrics, what started as a top-priority strategy could very easily become a massive institutional headache. You cannot just math your way through a market this complex. You need to be on the ground, and you need to be prepared for the reality that the spreadsheet is often the last thing that actually matters when things get difficult.

The Structural Foundations: Why the Indian Buyout Market Works

Running a blog for years has taught me that market trends often sound like noise until you look at the specific numbers that anchor them. Right now, there is a lot of talk about India, but the conviction EQT is showing is rooted in a very specific historical timeline that I think is worth breaking down. If you look back to 2013, the landscape was almost unrecognizable. EQT made a massive move then by taking a controlling stake in Hexaware Technologies, which was a landmark IT services buyout at the time. To put that into perspective, the entire Indian buyout market back then was only worth about 2 billion dollars. That means a single deal like Hexaware wasn't just a big transaction; it represented a huge slice of the country's entire private equity ecosystem.

By the time we hit 2024, that annual volume has surged to nearly 15 billion dollars. It is a massive jump in just over a decade, but the real story is where it goes next. If the current crop of multi-billion-dollar deals actually hits their targets over the next few years, we are looking at a market that could easily top 50 billion dollars by 2030. That kind of growth trajectory is why international investors, the Limited Partners who provide the capital, are feeling so much more confident lately. From what the leadership at EQT is seeing, these global investors don't just see India as another emerging market anymore. They see it as a stable harbor that is somewhat insulated from the geopolitical chaos happening elsewhere, especially since the country is now contributing roughly half of all global growth.

One thing that makes the Indian market particularly interesting right now, especially compared to the US or Europe, is the nature of the deals themselves. In more mature Western markets, things have become a bit stagnant. You often see what we call sponsor-to-sponsor transactions, where one private equity firm just sells a company to another private equity firm. It starts to feel like a game of musical chairs with the same assets. India is different because it is still dominated by primary buyouts. You have these massive, long-standing family-led businesses that have reached a point where they need a professional global hand to move to the next level. You also see large corporations carving out non-core units that they no longer want to manage. Because these sectors are often fragmented, it creates a perfect environment for a programmatic buy-and-build strategy. Instead of getting into a frantic bidding war over a recycled asset, a firm like EQT can basically hand-craft a deal and establish a proprietary position where they have actual control over how the business is run.

This leads into what EQT calls their active ownership playbook, which by 2026 is going to be almost entirely centered on how they use artificial intelligence to create operational alpha. They don't just view AI as a buzzword or a way to automate a few spreadsheets. They have a specific philosophy where they categorize every company they own into one of three buckets: Revolution, Transformation, or Augmentation. This dictates how deeply they integrate new tech into the core business model. For example, when they look at a healthcare asset or a tech services platform, they aren't just looking for minor efficiency gains. They are bringing in management teams that are specifically trained to think in terms of AI. They want to see backend scheduling handled entirely by algorithms, global procurement systems that optimize themselves, and service delivery paths that are completely streamlined.

The goal here isn't just to ride the general wave of India's economic growth. That would be the easy way out. The real aim of this human-led industrial approach is to fundamentally change the way these companies function at their core. By improving the underlying EBITDA margins through better tech and smarter management, they are essentially future-proofing these businesses. Whether the end goal is a high-profile public listing on a global exchange or a strategic sale to a major international player, the business needs to look lean and highly profitable. This transition from a family-run operation to a tech-enabled global competitor is what will likely define the next decade of the Indian buyout market.

References & Further Reading

- EQT Raises Asia Pacific's Largest Private Equity Fund, Closing BPEA IX at USD 15.6 Billion in Total Commitments — EQT Group (Official Press Release)

- EQT Closes Largest-Ever Asia PE Fund, Expects Strong Co-Investment Flow — ION Analytics (Mergermarket)

- EQT Private Capital Asia Bets on Indian Healthcare, Other Sectors — Medical Buyer

Disclaimer: All the data, strategic insights, and institutional metrics provided above were synthesized from public corporate announcements, financial statements, and regional private equity market studies. This comprehensive analysis is intended for informational and educational purposes only and should not be construed as official financial advice, investment recommendations, or an official quote from EQT AB or its affiliates.