In today's globalized macro-financial architecture, where institutional capital allocations are increasingly governed by rule-based algorithmic indexes, emerging market debt has transitioned into a highly benchmarked asset class. Over the last few years, the Republic of India has successfully executed a systematic opening of its domestic sovereign bond market to international investors. This structural evolution culminated in the nation securing positions within three of the world's most prestigious fixed-income benchmarks. Yet, beneath the triumphant headlines declaring a structural shift in foreign portfolio investments (FPI), a profound asymmetry exists. As we look across the financial landscape of 2026, it becomes increasingly clear that while India has secured a trio of index inclusions, only one serves as the true engine of structural, automatic, and unyielding passive capital inflows.

"Sovereign index inclusion is frequently heralded as a uniform gateway to global liquidity. In reality, the architecture of tracking funds creates a sharp divergence between optical inclusion and structural passive tracking."

To fully understand the mechanics of this phenomenon, one must dismantle the operational and institutional definitions that separate active mandates from pure passive replication. In fixed-income asset management, benchmarking falls into two disparate structural models: benchmark-aware active management and rigid passive indexing. When an index provider alters its composition, passive Exchange-Traded Funds (ETFs) and index mutual funds are legally and structurally mandated to buy the underlying assets in exact proportion to their index weights. Conversely, active asset managers utilize the benchmark merely as a performance hurdle or a loose asset allocation guide. If an active fund manager holds an aversion to a specific country due to currency volatility, operational friction, or geopolitical risk, they can choose to be structurally underweight or entirely absent from that country — regardless of its official weight within the index.

The Triad of India's Bond Index Inclusions

Between 2024 and 2026, India successfully finalized its cross-border integrations into three core sovereign debt tracking matrices. These steps represent a significant milestone in the development of the Indian bond market, shifting what was once a relatively isolated domestic debt landscape into a core focal point for international fixed-income allocators. The three specific inclusions are:

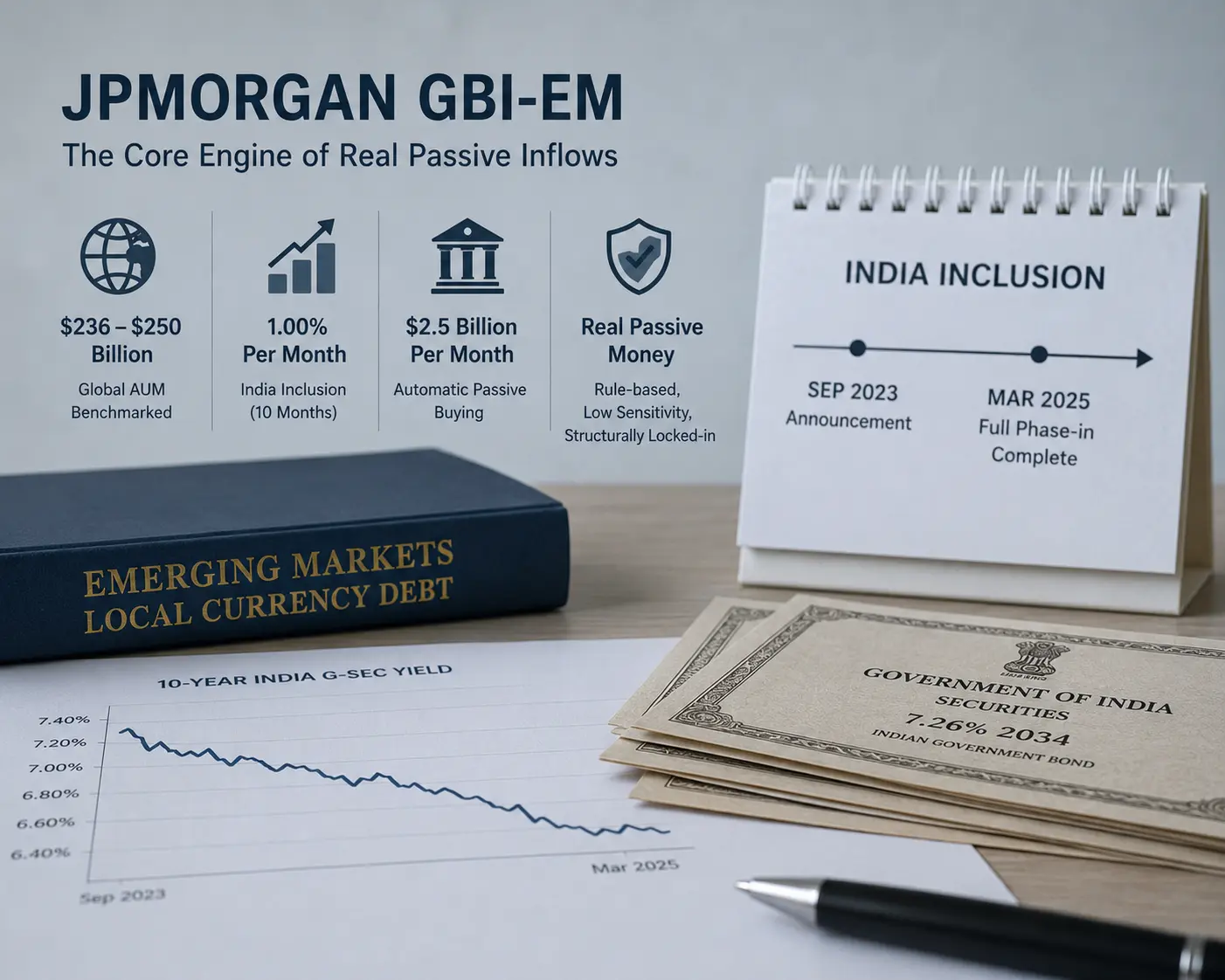

- The JPMorgan GBI-EM Global Diversified Index: Announced in September 2023, with the structural implementation commencing on June 28, 2024, and concluding in March 2025, reaching the maximum capped weighting of 10.00%.

- The Bloomberg EM Local Currency Government Index: Announced in early 2024, with its multi-stage inclusion rollout commencing on January 31, 2025, and phasing in over a ten-month horizon to hit a full market-value weighting cap.

- The FTSE Russell Emerging Markets Government Bond Index (EMGBI): Finalized for implementation in September 2025, with inclusion occurring across a six-month tranced timeline to capture a projected 9.35% index allocation.

Optically, these three indices appear to form a unified wall of global capital inflows. Financial analysts and mainstream financial publications often treat these inclusions as additive vectors, multiplying estimated capital inflows by three to project astronomical liquidity injections into the Indian Fully Accessible Route (FAR) bonds. This additive methodology is fundamentally flawed. To expose the underlying truth, we must analyze the structural capital tracking each individual benchmark.

| Index Platform / Benchmark Name | Inclusion Timeline Window | Capped / Target Weight | Total AUM Tracked | Nature of Core Tracking Capital | Actual / Expected Passive Inflows |

|---|---|---|---|---|---|

| JPMorgan GBI-EM Global Diversified | June 2024 – March 2025 | 10.00% (Max Cap) | ~$236 Billion – $250 Billion | Strict Passive & Pure Index Replication | ~$25.0 Billion |

| Bloomberg EM Local Currency Govt | January 2025 – October 2025 | 10.00% (Market Value) | ~$20 Billion – $30 Billion | Highly Active & Blended Mandates | ~$2.0 – $3.0 Billion |

| FTSE Russell EMGBI Index | September 2025 – March 2026 | ~9.35% (Tranced) | ~$30 Billion – $35 Billion | Active-Biased / Sovereign Wealth | ~$3.0 Billion |

The Core Engine: Why JPMorgan GBI-EM Brings the Only True Passive Tsunami

The structural reality of international emerging market debt allocation reveals that the JPMorgan GBI-EM Global Diversified Index is the absolute heavyweight benchmark for local currency sovereign debt. Globally, the total volume of institutional capital structurally tied to the GBI-EM family sits at approximately $236 billion to $250 billion. More importantly, the internal allocation of this capital leans heavily toward pure passive index replication vehicles, exchange-traded funds, and institutional mandates that leave zero operational discretion to the asset manager.

When India was added to this index at a rate of 1.00% per month over a 10-month period, a structural mechanism was triggered. Every passive manager tracking the index was legally required to automatically purchase Indian FAR bonds at a run-rate of approximately $2.5 billion per month. This automatic buying occurred regardless of prevailing macroeconomic concerns, domestic inflation trajectories, or the political configurations within New Delhi. The passive fund managers did not execute these trades because they held a tactical preference for Indian macro-stability; they executed them because the underlying index architecture gave them no other choice.

The numbers validate this mechanism clearly. During the period spanning from the initial announcement in September 2023 through the complete phase-in by March 2025, net capital inflows into India's FAR bonds scaled to over ₹1.9 trillion (approximately $25 billion). The structural demand triggered a persistent tightening in domestic yields, pushing the 10-year Indian benchmark government bond yield down significantly, moving from around 7.20% down toward 6.75% over the cyclical timeline. This behavior perfectly describes "Real Passive Money" — flows that arrive automatically, exhibit low sensitivity to short-term global shocks, and remain anchored in the domestic financial system because they are structurally locked into the global index composition.

The Optical Illusion of Bloomberg and FTSE Russell Benchmarks

In stark contrast to the JPMorgan GBI-EM, the Bloomberg Emerging Market Local Currency Government Index and the FTSE Russell EMGBI present an optical illusion of capital depth. While the global parent complexes of Bloomberg and FTSE manage multi-trillion-dollar indices — such as the massive Bloomberg Global Aggregate Bond Index, which commands between $2.0 to $2.5 trillion in benchmarked AUM — the specific emerging market subsets into which Indian bonds have been integrated command only a fraction of that scale.

The Bloomberg EM Local Currency Government Index is predominantly utilized as a performance hurdle by active global bond managers rather than a core underlying asset for pure passive ETFs. When active managers dominate an index's user base, inclusion does not generate a mandatory wave of capital. Instead, it forces active managers to make an active decision: do they want to initiate direct allocations to India, or would they prefer to remain underweight and fulfill their emerging market exposure via more liquid or operationally familiar Latin American or European sovereign assets?

"Assuming that inclusion in three separate indexes translates to three distinct waves of multi-billion dollar inflows misinterprets the plumbing of global asset management. If the benchmark is tracked actively, the inflow is merely a suggestion, not a mandate."

Furthermore, operational hurdles have heavily modified the trajectory of these secondary inclusions. In early 2026, Bloomberg Index Services Ltd (BISL) closely monitored the operational frictions encountered by foreign portfolio investors in the domestic Indian market, including custodian margins, post-trade settlement configurations across divergent time zones, and the tax reporting documentation required under Indian fiscal laws. Because these indices are primarily utilized by active institutional allocators who are highly sensitive to operational friction, the actual passive capital triggered by the Bloomberg EM and FTSE EMGBI inclusions amounted to a modest $2.0 billion to $3.0 billion each — a minor fraction compared to the JPMorgan capital wave.

Mathematical Modeling of Index Tracking Mechanics

To mathematically illustrate the divergence in capital behavior between these indices, we can formulate the Expected Passive Capital Inflow (I_p) for a specific country inclusion as a function of total benchmarked assets, the target weight, and the passive replication coefficient:

I_p = AUM × W × R_p

Where AUM represents the total institutional assets benchmarked to the specific index, W represents the final targeted country weight within that index matrix, and R_p represents the Passive Replication Coefficient — defined as the precise percentage of tracking capital that utilizes pure, non-discretionary passive duplication models (0 ≤ R_p ≤ 1).

For the JPMorgan GBI-EM Global Diversified index, the parameters resolve to an exceptionally high replication factor. Assuming an AUM of $240 billion, a capped target weight (W) of 10.00% (0.10), and a passive replication coefficient (R_p) estimated at 0.85, the structural capital inflow calculation yields:

I_p = $240,000,000,000 × 0.10 × 0.85 = $20,400,000,000

When factoring in the active benchmark-aware overlays that are forced to closely shadow the index to minimize tracking error, the total capital flow expands directly to the realized $25 billion mark. Conversely, applying this exact model to the Bloomberg EM Local Currency Index reveals the structural shortfall. While the target weight remains structurally similar at 10.00%, the tracking pool's active bias drives the passive replication coefficient down significantly to an estimated R_p = 0.10. On a smaller asset base of $25 billion, the formula reflects the true nature of the flow:

I_p = $25,000,000,000 × 0.10 × 0.10 = $250,000,000

This mathematical proof isolates the fundamental reality: without a massive asset base or a highly non-discretionary passive replication profile, index inclusions are simply optical victories that fail to deliver meaningful, structural capital inflows into a country's sovereign balance sheet.

Key Takeaway for Sovereign Debt Strategists

The structural success of India's sovereign debt program does not rest on accumulating a large number of index inclusions. Instead, it relies on maximizing the country's weight within highly passive, non-discretionary indexes like the JPMorgan GBI-EM, while continuing to target the eventual holy grail: inclusion in the Bloomberg Global Aggregate Index.

Looking Forward: The Ongoing Battle for the Global Aggregate

Recognizing this structural divergence, the Reserve Bank of India (RBI) and the Ministry of Finance have altered their long-term capital market strategy. Throughout late 2025 and into mid-2026, Indian financial regulators implemented significant policy adjustments targeted at global capital pools. On June 5, targeted regulatory amendments optimized the operational frameworks governing the Fully Accessible Route (FAR) bonds, leading to a strong resurgence in capital inflows with foreign portfolio investors injecting over $2.0 billion into rupee debt within a two-week window.

The absolute focus of these regulatory adjustments is to secure entry into the flagship Bloomberg Global Aggregate Bond Index. Unlike the niche emerging market indices, the Global Aggregate Index is a primary pillar of global fixed-income wealth, tracking trillions of dollars in high-grade institutional capital. Even a conservative 1.00% target weighting for India within the Global Aggregate benchmark could trigger an immediate, non-discretionary passive inflow of $25 billion to $30 billion. This would effectively match the entire multi-year impact of the JPMorgan inclusion in a single structural cycle.

For the broader macro context of how FPI outflows and domestic institutional bidding are interacting in India's bond market right now, see India's Rupee Depreciation Is Creating Structural Bid from Life Insurers and PSU Banks That the FPI Outflow Narrative Is Missing 2026.

Institutional Conclusion & Summary

India's transformation into a major destination for global fixed-income capital is an undeniable macroeconomic success. However, institutional investors, sovereign wealth funds, and domestic policy architects must analyze the index metrics with absolute precision. The three current index inclusions are not equals. The Bloomberg and FTSE Russell additions provide valuable optical credibility and entice marginal active capital, but they lack the structural framework to generate mandatory institutional demand. The JPMorgan GBI-EM Global Diversified Index stands alone as the single true vector of non-discretionary, multi-billion-dollar passive capital inflows into the Indian debt markets.

Read Further

- India's Inclusion in JPMorgan GBI-EM Global Diversified Index — Invest India, Government of India

- India's Recent Index Inclusion: A Double-Edged Sword — Invesco Asia Pacific Institutional Research

- FPI Flows Post JP Morgan Bond Index Inclusion — SBI Research, July 2024

Disclaimer: The data and structural analysis presented in this article are synthesized from historical fixed-income research data, index provider mandates, SBI Research, Invesco institutional analysis, and international portfolio flow studies. This report is for analytical and educational purposes and does not constitute formal investment, legal, or financial advisory allocation guidance.