The Breaking Point of Institutional Global Diversification

We live in a time where everyone talks about how connected the world has become, but if you are an investor in India trying to put your money into international markets, that connection feels more like a one-way street with a massive roadblock. I have been watching the situation with Indian mutual funds lately, and it is honestly getting hard to ignore how frustrating the landscape has become for the average person trying to diversify their savings. By 2026, we have reached a point that feels less like a minor regulatory hiccup and more like a full-blown crisis for anyone who wants to own a piece of global growth.

Think about the big names we usually trust with our money. Axis Mutual Fund, Nippon India, and Kotak Mahindra have all been put in an incredibly awkward position. They are not stopping their international funds because they want to or because the US or European markets are doing poorly. In fact, the demand from regular people like you and me is higher than it has ever been. People want to hedge against the local currency or get a slice of the big global tech giants. Yet, these fund houses are being forced to turn customers away. They are stopping lump-sum payments, refusing to let people switch money from one fund to another, and even putting a ceiling on systematic investment plans. It feels like trying to get into a popular club that has reached capacity, only the bouncer is a decades-old government regulation that no one seems interested in updating.

The root of this whole mess is a very specific, very rigid ceiling. Back in the day, the Securities and Exchange Board of India and the Reserve Bank of India set an industry-wide limit of seven billion dollars for overseas investments. There is a separate one billion dollar bucket just for Exchange Traded Funds, but the total is what really matters. When that rule was written, seven billion dollars probably sounded like a massive, untouchable mountain of money. But today, the Indian mutual fund industry is a different beast entirely. We are looking at a total asset base of over eighty lakh crore rupees as of early 2026. If you do the math, that seven billion dollar limit converts to roughly sixty thousand crore rupees. That is less than one percent of the total money managed by the industry. It is a tiny, cramped box for an industry that has grown way too large for it.

What this creates on the ground is a chaotic and frankly unstable environment. Because the limit is hit so frequently, fund houses have to play this strange game of waiting for redemptions. The regulator only allows them to take in new money to the exact extent that existing investors take their money out. So, if a few people sell their international units on a Tuesday, the fund might have enough headroom to open for a few hours on Wednesday. You get these sudden announcements where a fund opens for a day or two and then slams the door shut again the moment that tiny bit of space is filled. It makes it impossible for a regular person to plan their finances. How can you run a disciplined monthly SIP when the fund might just stop taking your money next month without warning?

The most frustrating part of this is how blatantly unfair it feels when you look at how the rules change depending on how much money you have in the bank. While a middle-class saver is told they cannot put five thousand rupees a month into a Nasdaq index fund because of national macro-economic stability, the rules for the truly wealthy are completely different. Under the Liberalised Remittance Scheme, or LRS, any resident individual can legally send up to two hundred and fifty thousand dollars out of the country every single year. They can buy property in London, open a brokerage account in New York, or just let the cash sit in a foreign bank account.

If you stop to think about that, the contradiction is staggering. A single high-net-worth individual can move nearly two crore rupees out of India every year with relatively little friction. But if a thousand retail investors want to pool their much smaller savings together into a low-cost, regulated, and transparent mutual fund, they are blocked by a ceiling that has not moved in years. We have created a system that actively discourages institutionalized, safe retail investing while leaving the door wide open for massive amounts of capital to fly out of the country in private accounts.

It feels like we have built a structural wall around the domestic mutual fund industry that does not actually stop money from leaving India. All it does is change who is allowed to send it and how they do it. It has turned the very basic concept of risk management and global diversification into a luxury item. If you are wealthy enough to manage your own offshore accounts, the world is your oyster. But if you are a regular person trying to use a simple domestic platform to protect your savings, you are left standing outside the door, waiting for a tiny bit of headroom to open up. It is a strange, disappointing reality for a market that claims to be moving toward a global future.

The Architecture of India's Outbound Capital Controls

It feels like we have been hitting the same brick wall for years now, but to really get why this situation is so frustrating in 2026, we have to look at where these investment caps actually came from. That seven billion dollar limit everyone talks about did not just appear out of nowhere, but it was born in a completely different world. Back when it was first scribbled into the rulebooks, India was in a defensive crouch. Our foreign exchange reserves were tiny compared to the hundreds of billions we have sitting in the vault today, and our domestic stock markets were still pretty shaky. The people in charge back then were worried about one thing: survival. They wanted to make sure that if a global crisis hit, all the capital in the country would not just vanish overnight in a massive wave of flight. They also wanted to make sure that the money Indian families were saving was being funneled into building our own roads, bridges, and factories rather than just being sent abroad to fuel other economies. It was an extension of that old school mindset where you manage the capital account very tightly because you are terrified the currency will just collapse if you let people move money too freely.

The real trouble started not with the intent of the policy, but with how it was actually put into practice. It was a classic case of rigid design. Instead of making the limit a moving target—something that could grow as the mutual fund industry got bigger or as our national reserves climbed—they just picked a flat, nominal number and stayed there. It was seven billion dollars, period. This lack of foresight became a massive headache in 2022 when the industry finally hit that ceiling. At that point, the regulator, SEBI, stepped in and did something that still feels incredibly arbitrary today. They basically took a snapshot of every fund house at that exact moment and told them they could never go beyond their current balance.

Think about how that works for a second because the math is actually pretty punishing. If a specific fund house happened to have six hundred million dollars invested globally on the day the music stopped, that six hundred million became their permanent ceiling. They were locked in. If the market dipped or if people started pulling their money out and the fund dropped down to four hundred million, the manager could accept new money to get back up to six hundred, but they could never cross it. It did not matter if they were the best performing fund in the country or if they had thousands of new investors banging on the door. They were stuck with their historical high point.

This created a totally warped playing field. If you were a newer fund house that was growing fast but had not yet moved much money overseas when the freeze happened, you were basically out of luck. You were stuck with a tiny limit while the older, bigger players got to keep their massive share of the pie. It stopped being about who had the best strategy or the lowest fees and started being about who happened to be big at the right time in 2022. For the average person just trying to put some of their savings into a global tech fund or a diversified international portfolio, it means they are often told the fund is closed for new subscriptions. They are essentially left standing at the gate while the system protects a status quo that stopped making sense a long time ago. We are operating a modern, globalized financial system using a set of emergency brakes that were designed for a much smaller and more fragile economy. It has moved beyond being a simple regulation and has become a genuine distortion of how the market should function.

The LRS Surge: Exposing the Policy Contradiction

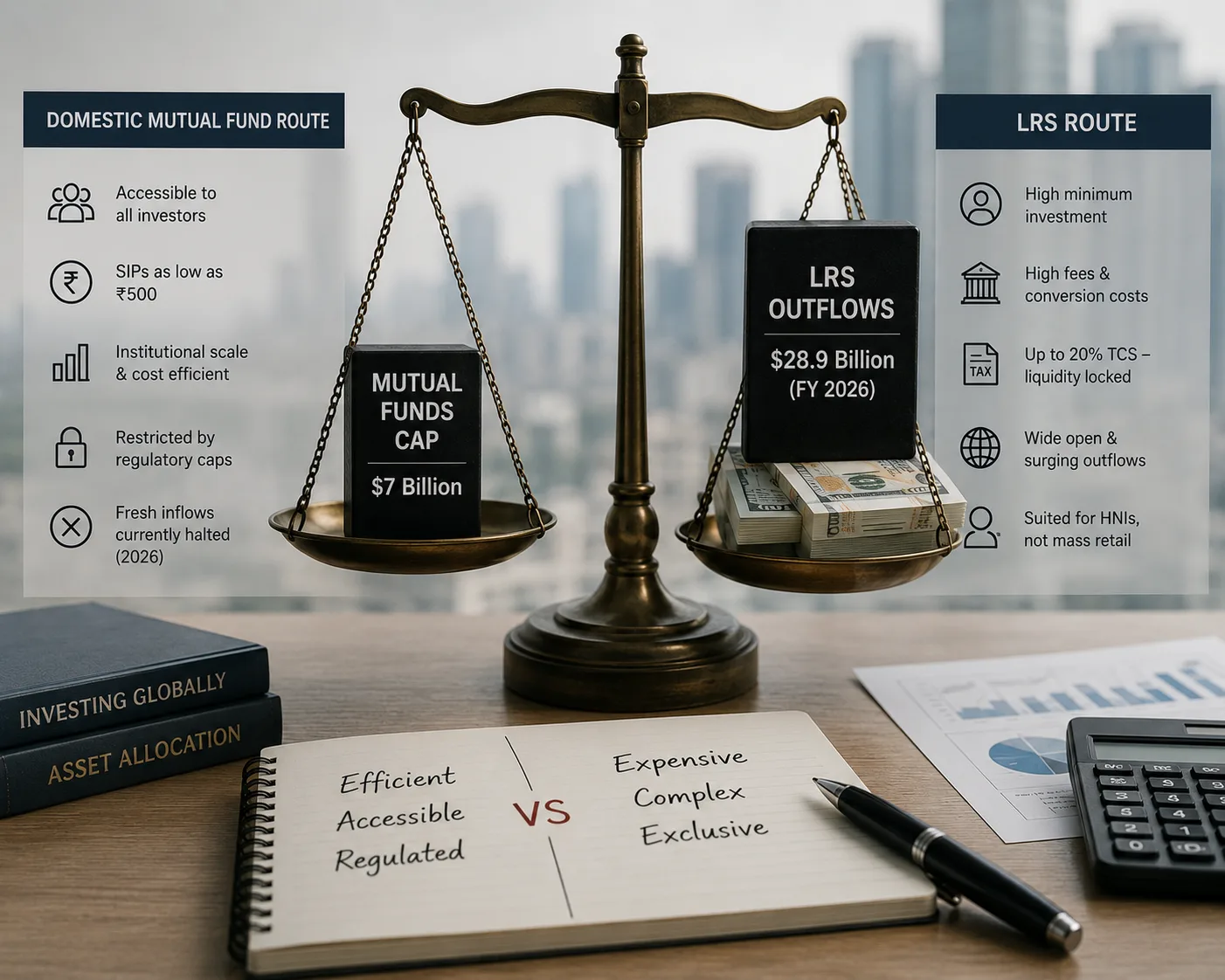

Recent data from the Reserve Bank of India has pulled back the curtain on a policy contradiction that is becoming harder to ignore. If you look at the macroeconomic figures for the financial year ending in 2026, the numbers tell a story of two very different worlds. On one side, individual outward remittances through the Liberalised Remittance Scheme, or LRS, have climbed to an all-time high of 28.9 billion dollars. At the same time, Indian corporate investment abroad grew by 11 percent to reach over 48 billion dollars. These are massive movements of capital. But when you place these figures next to the mutual fund industry, the disconnect is startling. The entire lifetime cap for the domestic mutual fund sector is stuck at a mere 7 billion dollars. To put that in perspective, the LRS route allows more money to leave the country in a single quarter than the entire mutual fund industry has been permitted to invest globally over several decades.

This asymmetry creates a real mess for the average person trying to build a portfolio. Because domestic mutual funds are essentially locked out of international markets by these caps, investors who have the means and the knowledge are simply going around them. They are moving their money into offshore portfolio management services, direct international brokerages, and various digital wealth apps that plug directly into the LRS system. It is a migration that leaves the domestic mutual fund industry behind, but more importantly, it creates several practical problems for the investors themselves.

One of the biggest issues is the sheer cost of entry. If you want to use the LRS route to access international markets through a professional offshore portfolio manager, you are usually looking at a minimum investment of about 75,000 dollars. That is roughly 66 lakh rupees. For most people, that is a massive hurdle that effectively shuts out the mass retail investor. Beyond the entry fee, there is the problem of frictional leakage. When an individual sends money abroad, they get hit with bank fees, high currency conversion spreads, and wire charges. These costs eat into the principal before a single dollar is even invested. If a domestic mutual fund were handling this, they would be converting currency in bulk at institutional rates, which is far more efficient.

Then there is the headache of the tax collection at source regime. Right now, if your LRS remittance crosses a certain threshold, you are hit with a TCS rate of up to 20 percent. Even though you can eventually claim this back or offset it against your final tax liability, it still means a significant chunk of your money is sitting with the government for months instead of compounding in the market. It is a huge drain on liquidity that hurts the long-term growth of a retail portfolio.

When you compare the two paths, the differences are stark. The domestic mutual fund route is designed for everyone, with SIPs starting as low as 500 rupees. It is capital efficient because of institutional scale and it does not suffer from the upfront liquidity drain of TCS. However, it is currently strangled by regulatory caps that have halted fresh inflows across most major funds as of 2026. On the other hand, the direct LRS route is wide open and surging, as evidenced by that 28.9 billion dollar figure, but it is largely reserved for high-net-worth individuals who can stomach the high fees and the 20 percent upfront tax hit. We are essentially in a situation where the most accessible and efficient way to invest globally is the one most restricted by policy.

The Macroeconomic Irony and Systematic Risks

I have been looking at how India handles its foreign investment rules lately, and there is a really strange irony in how the central bank and market regulators are managing things. Right now, there is a seven billion dollar cap on mutual funds that want to invest abroad. The regulators are holding onto this limit because they are nervous about the Rupee. They want to keep foreign reserves stable, especially when oil prices are jumping around or when global investors start pulling money out of Indian markets. It makes sense on paper, but in practice, it is creating exactly the problem they are trying to avoid.

By keeping the door shut for mutual funds, the system has accidentally pushed everyone toward the Liberalized Remittance Scheme, or LRS. This is a much messier way for money to leave. Think about how it works when you use a domestic mutual fund. If you buy into an international fund through an Indian asset management company, that money stays within a regulated environment. The AMC is an Indian entity. If you decide to sell your holdings, the AMC liquidates those foreign assets, the money hits the Indian banking system, and it is converted right back into Rupees. Everything is visible, and the wealth effectively stays within the domestic framework. The regulator can see exactly where the money is and how it moves.

Now compare that to what happens when an investor uses the LRS route to send money abroad directly. That capital just leaves the domestic financial system entirely. It moves into foreign cash accounts, international equities, or other dollar-denominated assets where it can sit for years or even decades. Once it is out there, it can remain offshore indefinitely. The regulator has much less control over when or if that money ever comes back to the Indian economy. It is a genuine, structural drain on domestic reserves because the loop is never necessarily closed.

We are seeing the fallout of this now in 2026. Both the RBI and SEBI have started breathing down the necks of corporate treasuries and family offices. They are sending out all these regulatory queries, trying to verify if the money being sent overseas actually has a real commercial reason behind it. They are clearly worried about the volume of capital leaving the country, yet they are ignoring the most straightforward fix staring them in the face.

If the regulators just lifted that seven billion dollar cap for institutional players, they could channel all that demand for global diversification through clean, visible domestic mutual fund structures. It would be much easier to monitor. Instead of chasing down individual transfers and questioning every corporate move to see if it is legitimate, they could let the regulated funds handle it in a way that keeps the capital tied to the Indian financial architecture. It is a weird disconnect where the fear of losing reserves is actually making the reserve drain harder to manage and less transparent. Pushing people toward unpooled, direct offshore accounts is the exact opposite of maintaining a stable, controlled capital account.

The Path Forward: Structural Integration Over Arbitrary Caps

We have reached a point where the current way India handles overseas investments through mutual funds is not just frustrating but fundamentally broken. The framework we are using today was built for a different era of the Indian market, and it is simply not sustainable anymore. We saw the breaking point clearly in 2026 when various asset management companies had to abruptly stop taking new money for international funds because they hit a wall. That wall is the static seven billion dollar industry cap, a number that feels increasingly arbitrary as our domestic market grows. If regulators want to fix this capital control problem, they need to stop relying on these fixed, nominal caps and move toward a dynamic system that actually reflects the size of the modern economy.

One way to do this is to get rid of that seven billion dollar figure entirely and replace it with a limit that moves. We could tie the allowance for overseas investments to a conservative percentage of the total assets under management across the entire mutual fund industry. Alternatively, it could be linked to a moving average of India's total foreign exchange reserves. Either approach would create a system that scales naturally. When the domestic financial ecosystem expands or when our national reserves are healthy, the capacity for safe global diversification would grow right alongside it. This would prevent the kind of sudden, jarring disruptions that leave investors stranded and fund managers unable to execute their strategies. It is about building a release valve that adjusts based on the actual pressure in the system.

There is another path policymakers could take that might be even more straightforward, and that is integrating these investments directly into the existing Liberalised Remittance Scheme, or LRS. Right now, every individual in India has a personal annual limit of two hundred and fifty thousand dollars for sending money abroad. If someone buys an international mutual fund through a domestic provider, that investment could simply count against their own personal LRS quota. This would instantly remove the institutional bottleneck that holds back the entire industry. By doing this, we create a much more level playing field. A small retail saver should have the same access to global assets as a wealthy investor who has the resources to set up direct foreign brokerage accounts. Using the LRS framework keeps the total movement of capital under the watchful eye of regulators while ensuring the process is transparent and accessible through domestic platforms that people already trust.

The reality is that as more Indians look to diversify their portfolios and protect themselves against local market volatility, the demand for international exposure is only going to go up. Keeping a rigid lid on that demand does not stop the need for diversification; it just creates distortions and unfairness. Whether it is through a macro-linked dynamic cap or a unified individual limit, the goal is the same. We need a regulatory environment that recognizes how much the Indian investor has evolved. Moving away from these outdated nominal caps would show that the regulators are ready to support a more mature, globally connected financial landscape instead of trying to manage a modern economy with tools from the past.

References & Further Reading

- AMFI Urges RBI to Raise $7 Billion Overseas Investment Limit Amid Volatile Markets — Outlook Money

- Outward Remittances Slipped 2% to $28.98 Billion in FY26: RBI Data — Business Standard

- Check SEBI Limits on Overseas Investment by Mutual Funds — Vested Finance

Disclaimer: All the data and macroeconomic analysis provided above were sourced from publicly available internet resources, historical regulatory circulars from SEBI and RBI, and economic trend studies done upon cross-border capital flows. This content is for analytical and educational purposes only and should not be construed as formal financial, legal, or investment advice.