In today's era where corporate perks and digital policy copies are being issued and generated instantly, we are too much dependent on them and somehow we feel secure, and somehow we are not. We browse through polished mobile apps seeing a reassuring "Rs. 10 Lakh Sum Insured" banner, completely oblivious to the mechanics waiting to trap us at the billing counter.

Insurance policies are something that were created to protect our hard-earned savings during emergencies with better efficiency. But when we just ended up depending on automated renewals and employers' HR portals for everything, we don't know where we actually forgot the hidden math and old structural conditions embedded in insurance rulebooks. We assume that a medical bill of Rs. 6 Lakh will be completely wiped out if our cover is Rs. 10 Lakh. So this article is going to get you all aware about what the actual breakdown looks like and what we should do with original fine prints before checking into a hospital network.

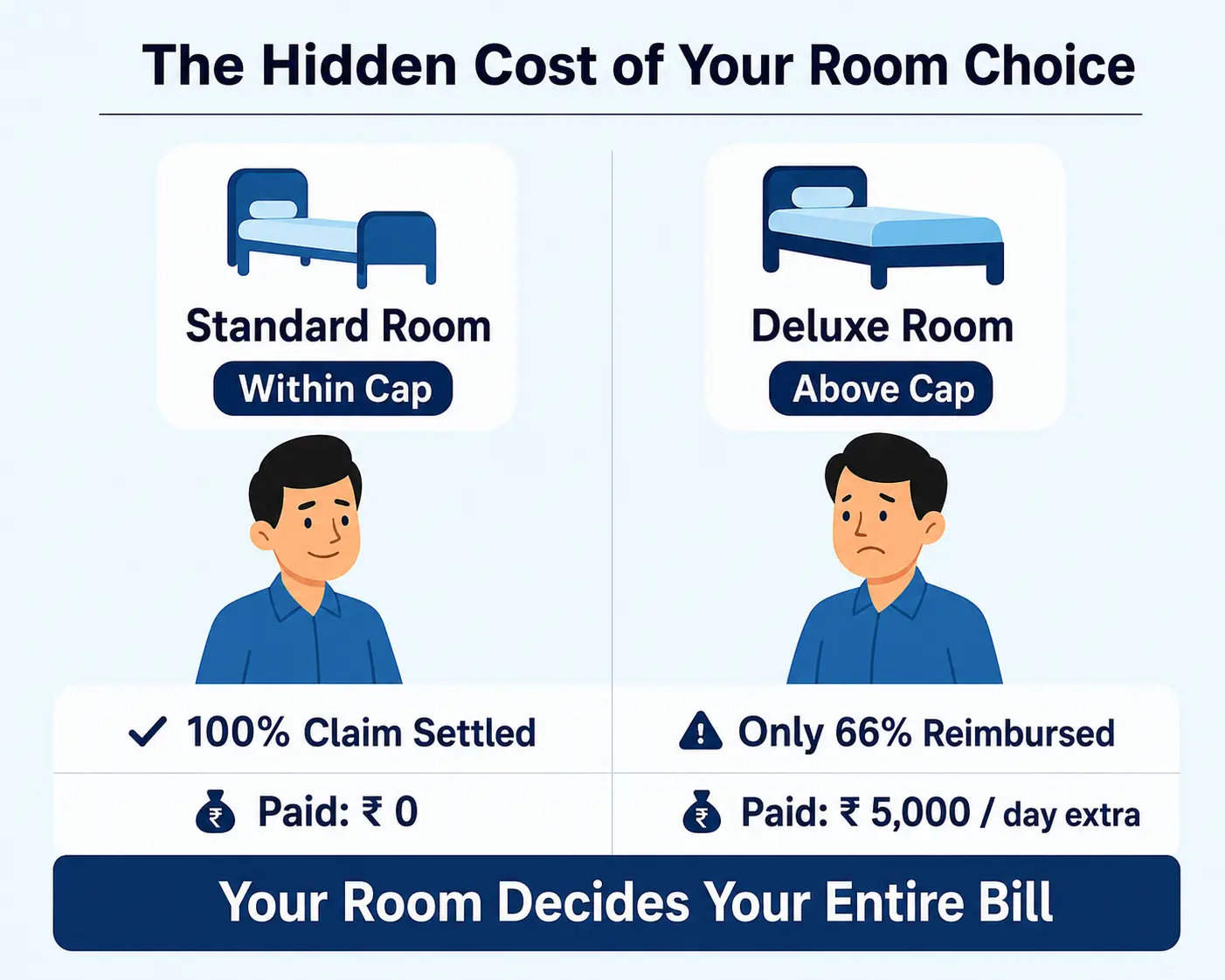

The Room Rent Cap: The Silent Multiplier of Claims Reductions

This is the single biggest culprit behind major financial shocks. Most standard retail and corporate health policies restrict your daily room rent to exactly 1% of your total Sum Insured. For a Rs. 10 Lakh cover, that allows a room variant of Rs. 10,000 per day. But if you hold a legacy or corporate policy of Rs. 3 Lakh or Rs. 5 Lakh, or find yourself trapped under older policy constructs, your room allowance caps out dynamically.

Choose your room consciously, because it dictates your entire hospital bill proportionally.

The danger is not just paying the room difference out of pocket. Hospitals operate on dynamic pricing structures tied directly to room categories. If you admit into a Deluxe Room costing Rs. 15,000 when your eligible cap is Rs. 10,000, your policy triggers a proportionate deduction across the entire invoice. Doctors' consulting fees, surgical charges, OT costs, and nursing services are scaled down by a factor of 10,000 / 15,000 (or 66.6%). Everything gets chopped down proportionally.

Co-payment and Disease-Specific Sub-limits

In recent analytical studies, it was seen that major policy designs provide corporate covers or senior citizen plans with built-in co-payments ranging from 10% to 20%. A vast difference of out-of-pocket expenses is seen when specific procedures get sub-limited. Even if you have a Rs. 10 Lakh macro-cover, specific treatments like Cataract surgeries, Hernia repairs, or Joint replacements have local ceilings hidden inside the structural charts.

The Mathematical Reality: If a standard Cataract surgery costs Rs. 1,20,000 and your specific disease sub-limit caps out at Rs. 40,000, your macro-cover of Rs. 10 Lakh will fail to trigger for the remainder, leaving a straight deficit of Rs. 80,000 on that item alone.

Non-Medical Expenses: The Excluded Consumables

Giving zero attention to the consumables checklist will become an endless loop of getting multiple items rejected at discharge, which will become a tiresome chore of settling bills out of your savings. Items like PPE kits, surgical gloves, administrative charges, masks, and specialised nebulizer kits fall under "Non-Medical Expenses". In modern heavy surgical procedures, these consumables can easily scale up to 10% to 15% of the gross billing statement, and traditional basic covers completely refuse to absorb them.

An Authentic Claim Reduction Case Study

To see how a Rs. 10 Lakh policy scales down to Rs. 3.8 Lakh in a real scenario, here is an actual surgical billing breakdown for a major cardiovascular intervention:

| Billing Component | Actual Hospital Bill | Insurance Allowed Amount | Clause Applied |

|---|---|---|---|

| Room Rent (4 Days) | Rs. 60,000 (Rs. 15,000/day) | Rs. 40,000 | Capped at 1% of Sum Insured (Rs. 10,000/day) |

| Operation Theater & Surgeon's Fee | Rs. 2,50,000 | Rs. 1,66,666 | Proportionate deduction applied (10k / 15k room ratio) |

| Medicines & Implants | Rs. 1,80,000 | Rs. 1,30,000 | Specific non-standard charges excluded |

| Consumables & Hygiene Kits | Rs. 70,000 | Rs. 0 | Non-Medical Expenses Clause (Non-payable) |

| Investigations & Diagnostics | Rs. 40,000 | Rs. 40,000 | Fully covered under diagnostic limits |

| Gross Total | Rs. 6,00,000 | Rs. 3,76,666 | Net Payable Claim (~Rs. 3.8 Lakh) |

Reviewing this data, the client is forced to absorb a massive Rs. 2,23,334 shortfall out of pocket, despite holding a proud macro-cover limit of Rs. 10 Lakh. The calculations show that it is the structural fine-prints that slice through the claim, rather than the primary value of your sum insured.

References

[1] Insurance Regulatory and Development Authority of India (IRDAI). Guidelines on Standardisation of Health Insurance Products — Click here

[2] IRDAI. List of Standardised Non-Payable Items in Health Insurance Claims — Click here

Disclaimer: All the data provided above was compiled from internet resources, regulatory disclosures, and analytical case studies done upon insurance systems. This should not be taken as an absolute corporate quote or official financial advice.