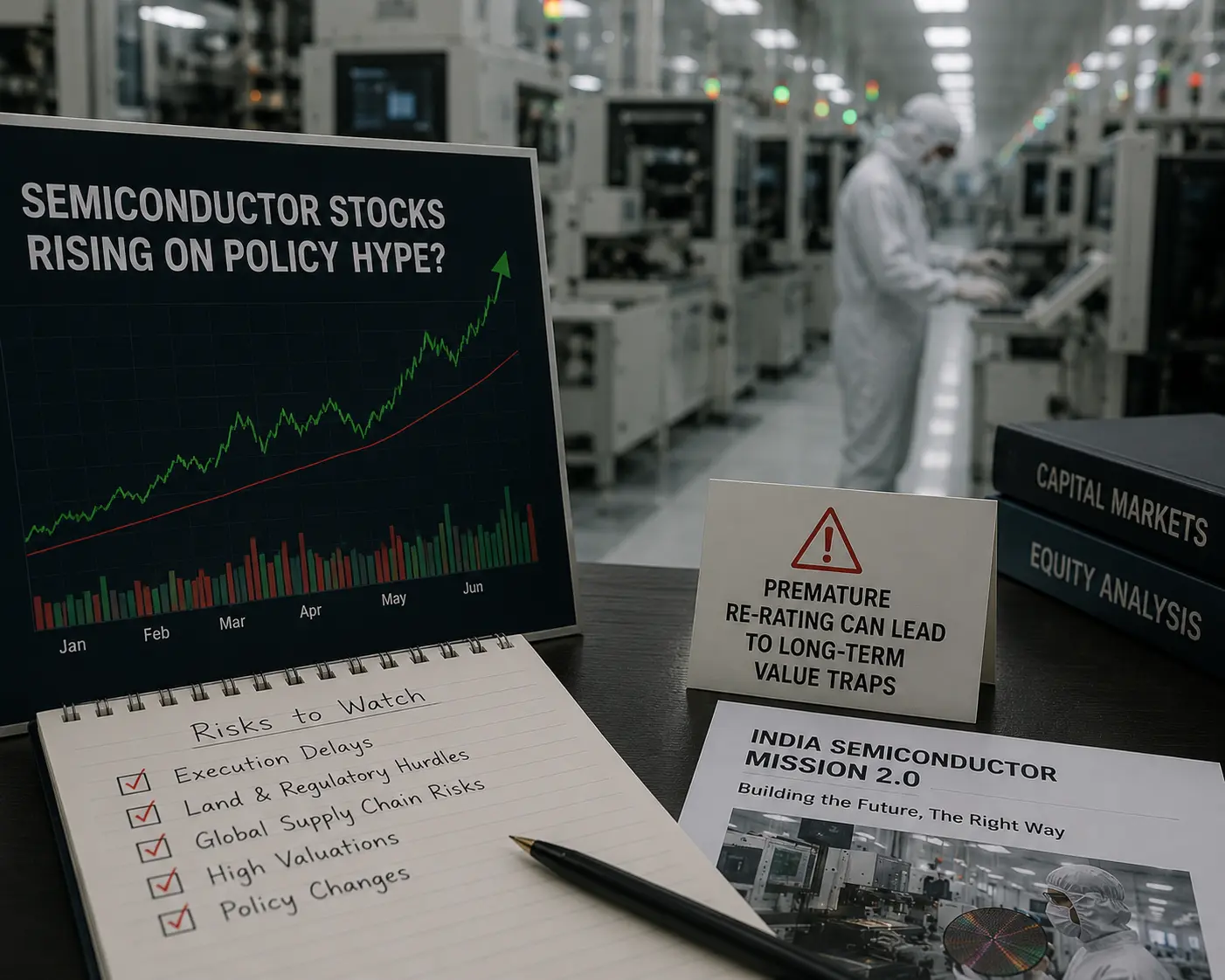

In an age when markets react to headlines more rapidly than actual factories are ever built, we have become too dependent on first announcements, and somehow these are too useful for short-term traders and not useful for long-term wealth creators. Whenever a gigantic multi-billion dollar policy framework is leaked or cleared by an internal committee, the stock market starts to behave like an autonomous machine, crunching in decades of perfect execution in just a few minutes. We see public companies' stocks soaring 20%, 50% or even doubling their market caps in value before they've even laid a single brick of concrete or packaged a single chip. We don't know where or when we actually forgot the age-old guidelines of value investing and fundamental discipline; we don't know.

So, this article is basically gonna teach you guys what to do about the enormous speculative rallies caused by policy blueprints and what to do about true, original, fundamental analysis of companies inside the Indian chipmaking space. We examine the recent Rs. 1.25 lakh crore outlay clearance for the India Semiconductor Mission (ISM) 2.0. We track down why the market re-rated these stocks before the Union Cabinet green-lit the final dotted line, and we work out here the hidden risks and structural realities of this long-term technological journey.

The Rs. 1.25 Lakh Crore Heavy-Weight Outlay and the Market Euphoria

With government programs now leading to growth in India's industrial infrastructure, public and retail stock speculation seems to be centered around funding for the high-tech sectors. In recent days the Expenditure Finance Committee (EFC) under the Ministry of Finance has approved a huge proposal for Rs. 1.25 lakh crore specifically under the India Semiconductor Mission (ISM) 2.0. This is a giant leap from the Rs. 76,000 crore package provided under the first edition of the mission. This announcement, directly derived from the milestones of the Union Budget 26-27, will add to building India's capabilities across the entire deep-tech matrix. Instead of only focusing on regular outsourced semiconductor assembly and test (OSAT) facilities, Mission 2.0 seeks to support advanced areas such as capital equipment manufacturing, raw materials supply chains, specialized chemical infrastructure and indigenous intellectual property (IP) design architectures.

ISM 2.0 — Overall Key Structural Shift: In contrast to what its predecessor was — one that would concentrate on building heavy production foundries — ISM 2.0 further deepens India's approach in another important strategy: it will add support for productisation significantly and establish a stronger focus on talent generation and ecosystem integration. It provides a standardised fiscal support mechanism of up to 50 per cent for sanctioned silicon fabs, compound semiconductor plants and display manufacturing units, making a very conducive ground for global and domestic joint ventures. As news emanated from within the walls of the expenditure department, there was no waiting for the formal Union Cabinet nod on Dalal Street. Financial tickers went off right away. The market's thinking is simple: if the government is pouring an additional 65% capital into a crucial strategic industry, the first movers will have a permanent cushion of liquidity and guaranteed state support.

This forward pricing mechanism has re-rated multiples for mid-cap, small-cap, and micro-cap companies which have even a distant relationship with the electronics assembly, design or testing value chain.

Top Semiconductor and Ancillary Stocks Experiencing Re-Rating

These are the names of certain key public companies and ecosystem participants whose valuations are in the process of being re-rated by the market just before the final Cabinet nod:

1. CG Power and Industrial Solutions Ltd. A leading infrastructural player who has shown tremendous development through its joint venture for running an advanced OSAT packaging plant in Gujarat. Investors have aggressively priced in the multi-year revenue pipelines from this project, leading to extreme valuation premiums, even though commercial scale operations require systematic gestation periods. Brokerages are still split, with conservative firms remaining cautious on near-term multiple expansion.

2. MosChip Technologies Ltd. Being one of India's few pure-play listed semiconductor design and silicon engineering services companies, MosChip directly falls under the core of ISM 2.0's thrust on design-led incentives. With strong financial growth in FY26 on the cards, delivering net sales of Rs. 5.85 billion and growth-key acquisitions in the form of a 73% stake in Vayavya Labs to strengthen embedded software capabilities — recording a revenue CAGR of 38% over five years — the scrip has been grabbed by retail and institutional investors as a play on design-centric IP solutions.

3. Kaynes Technology India Ltd. A leading electronic manufacturing services (EMS) provider entering strongly into complex advanced semiconductor packaging units. The company's unparalleled execution ability is obvious, yet its stock has experienced enormous multiple expansions, leading global research houses to scrutinize whether the short-term cash flows could justify the sky-high market cap levels attained well before construction implementation.

4. ASM Technologies Ltd. A provider of engineering and product development services for semiconductor equipment manufacturers. Since ISM 2.0 directly supports local hardware and sub-component production, this micro-cap stock morphed into a momentum darling, demonstrating just how volatile free-float shares can get on macro policy news.

Tata Group Ecosystem The mega silicon fab plants are concentrated within the unlisted Tata Electronics entity, but the listed entities of the Tata group have a halo effect. The market is giving the benefit of the doubt on the long-term captive demand for auto-grade chips in Tata Motors and the infrastructure synergy with Tata Power that will lead institutional money into these blue-chip Tatas.

Cons of the Premature Re-Rating and Policy Hype

Policy-driven valuation expansions, after all, are still market-based psychology, not ground truth. They can reliably give a positive short-to-mid term direction, but they also create a large deviation in what the retail public expects about when the projects will actually be commissioned — a pattern seen in the last several cycles. Recent market cycles have shown that big infrastructure policies do get a strong headline direction from which to build, but when the retail public mass-positions just because headline outlays look good, there's a massive gap of accuracy between expected project commissioning and reality. Historical patterns suggest that at least two of every five major high-tech announcements undergo a structural industry slowdown, land alignment delays, or regulatory re-evaluation, dumping the speculative pricing out with very large error margins that can yield capital traps for late-stage investors.

The Challenge of the Execution Gap: Semiconductor foundries are some of the most intricate engineering structures ever created by man. They need steady ultra-purified water supplies, stable power grids, decadal capital cycles, and specialized international talent. Buying up token stocks with ridiculous 90x or 100x Price-to-Earnings ratios before a single commercial wafer is minted spawns an endless cycle of monitoring policy changes, culminating in a soul-numbing chore for the average retail investor whose anxiety grows with his meager compounding returns.

The Essential Figures of India's Chip Aspirations (ISM 1.0 vs ISM 2.0)

To gauge the extent of what is being attempted, it is necessary to look at the aggregate data from the first stages and the forthcoming targets under the Rs. 1.25 lakh crore roadmap for the financial years from 2026 onwards:

| Parameters & Metrics | ISM 1.0 | ISM 2.0 Budget (2026) |

|---|---|---|

| Total Government Fiscal Outlay | Rs. 76,000 Crore | Rs. 1,25,000 Crore |

| Key Operational Focus | Mega Fabrication & OSAT Units | Full Supply Chain, Equipment, Design & IP |

| Design Linked Incentive (DLI) Projects | 24 Startups Supported | Targeting 50+ Specialized Product Firms |

| Access to Advanced Design Tools | 105 Companies / Research Centres | Expanded to 250+ Ecosystem Partners |

| Target Node Specialisation | Mature Nodes (28nm to 110nm) | Mature Nodes + Exploration of Power & Compound Nodes |

| Average Domestic Market Projection | $45–$50 Billion (2024-25) | $100–$110 Billion by 2030 |

The Balanced Approach: Merging Macro Momentum with Micro Sanity

Now, you might think we are belittling the audacious scope of the India Semiconductor Mission, but it is no such thing — it is the kind of fundamental discipline that makes you fully aware of what you are buying and whether or not you are buying something good, or something bad. It's the kind of thinking that builds a habit to always think twice before putting money in a momentum trade, which basically underpins long-term success in capital preservation and portfolio management. The government's desire is evident: they are helping to build a fiscal wall to protect domestic electronics manufacturing from being overwhelmed by imports. Our job as smart investors is not to disregard this huge tailwind, but to avoid getting fleeced into paying crazy premiums for concepts that are still waiting on a final Cabinet nod and months of operational vetting. Seek out companies with robust organic cash flows from their core legacy operations that see the semiconductor lift as a free optional lottery ticket — and avoid those whose entire existence is tied to a single piece of government subsidy clearance.

"Invest consciously, calculate fundamentally and save your capital from the noise of early headlines."

Read Further

- Finance Ministry Panel Clears Rs. 1.25 Lakh Crore Outlay for ISM 2.0 — Daily Pioneer

- MosChip Technologies Acquires 73% Stake in Vayavya Labs for ₹245.49 Crore — Electronics For You

- India Doubles Down on Chips: Rs. 1.25 Lakh Crore Cleared for Semiconductor Mission 2.0 — Republic World

Disclaimer: All the analytical data, corporate figures, and policy updates provided above were compiled from public internet resources, press releases, and independent equity research studies done upon the Indian manufacturing ecosystem. This report should not be taken as an official quote or a piece of formal financial advice for immediate equity accumulation.