Autonomous Frameworks and the Illusion of Fiscal Neutrality

Building on the historic July 2026 bilateral summit in New Delhi between Indian Prime Minister Narendra Modi and Japanese Prime Minister Sanae Takaichi, a seismic shift in regional energy system was crystallized. Against the backdrop of fanfare at the announcement of a new $10 billion Japanese investment package in areas including critical minerals, semiconductors, and artificial intelligence, the signing of the India-Japan Liquefied Natural Gas (LNG) Stockpiling Pact turned out to be the strategic centerpiece of the engagement. The arrangement aims at developing an airtight Joint Task Force on LNG Stockpiling under the long-established India-Japan Energy Dialogue for sharing market intelligence and developing mutual fall-back options in case of global supply downturns.

At least on the storytelling front, the Ministry of Petroleum and Natural Gas shows nothing but standard geopolitical realism. India is still quite exposed to the turbulent waters of West Asia, as it relies on the Strait of Hormuz for the vast majority of its LNG imports — a region currently rife with systemic tension. In comparison, Japan has methodically weaned itself off West Asian hydrocarbon basins to just 10% of its overall purchases after decades' worth of insulating itself. By partnering with the world's second biggest LNG trader, New Delhi gains access to an advanced institutional safety net that can help it navigate through abrupt commodity price hikes or physical shortfalls.

"Energy resilience is not energy resilience only if measured by the pace of availability of energy; energy resilience should be weighed against infrastructural and financial longevity needed to deliver it."

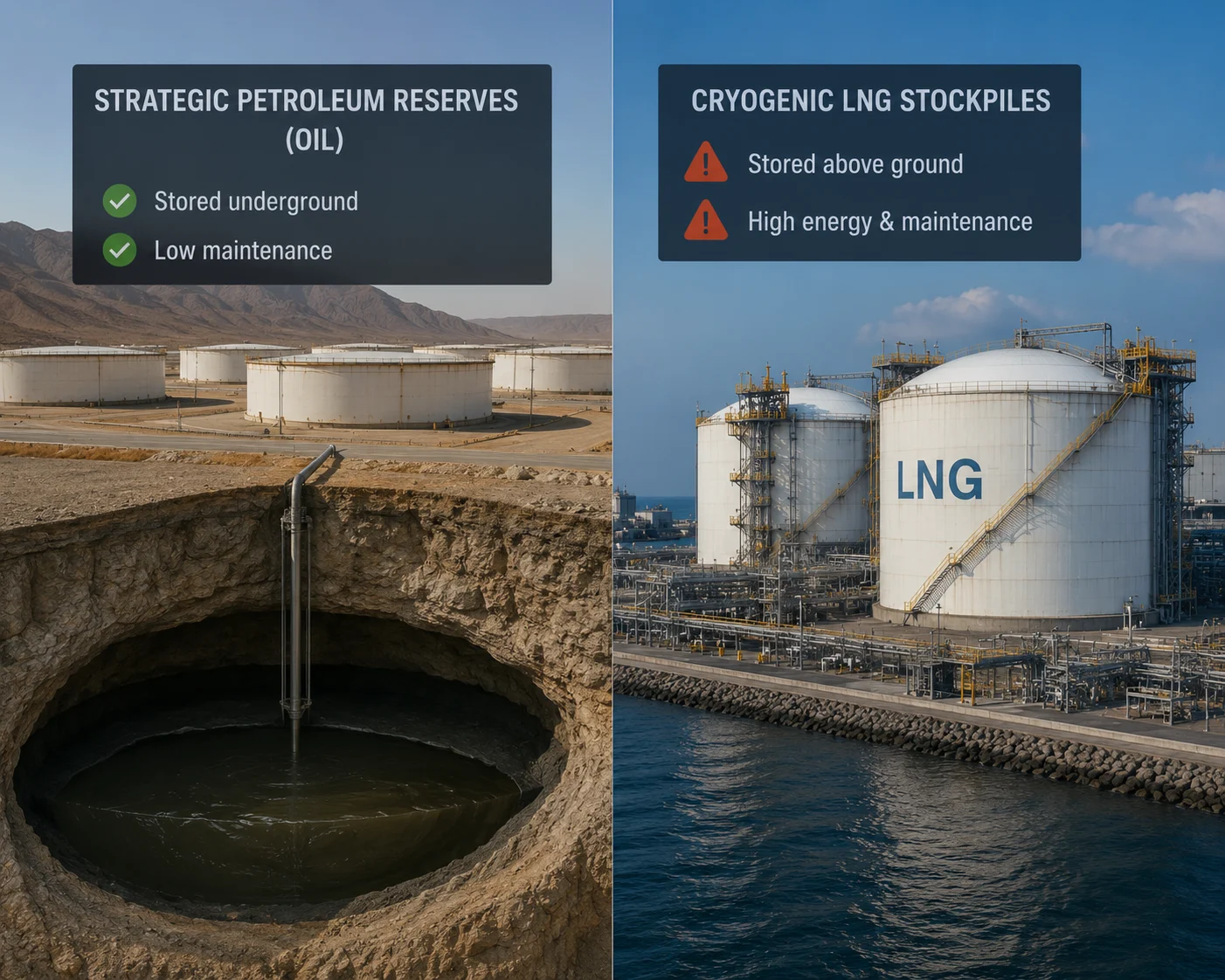

Yet beneath the jubilant press statements is a quiet fiscal reality that the government has consistently left out of public parliamentary briefings: the massive, ongoing capital outlay necessary to develop and maintain a cryogenic strategic natural gas reserve. Unlike crude oil, which is relatively stable when stored in underground salt caverns or unlined rock caverns, natural gas must be supercooled to a mind-blowing minus 162 degrees Celsius to keep it in liquid form. This technicality changes the whole math when it comes to national security reserves, with a relentless, compounding fiscal burden on the Indian exchequer to silently bear for the next two decades.

The Cryogenic Conundrum: The Hidden Capital and Operational Drain

To get a sense of the size of these opaque fiscal commitments, you need to go deep into the thermodynamics of LNG infrastructure. When the government builds a Strategic Petroleum Reserve (SPR), most of the expenses are up-front site acquisition, cave drilling, and filling the crude stock. After filling, crude oil deteriorates at such a slow rate that operational costs are negligible. LNG stockpiling, by contrast, rebuffs fiscal passivity. Supercooled liquid storage necessitates high-tech double-walled nickel-steel alloy tanks, layered with advanced vacuum insulating materials. Even at the best commercial levels of engineering, a certain amount of Boil-Off Gas (BOG) is going to be physically generated. BOG is a continuous birth of evaporation, as the ambient heat is continually infiltrating the storage vessel, heating the liquid methane to the point where it changes its state back to gas. At typical commercial regassification terminals, this boil-off gas is captured right away and sent at pressure into active gas pipelines where it is sold in the commercial market. But in a strategic stockpile where the fuel is sitting idle for long stretches to provide an emergency buffer, BOG is a much more significant financial hemorrhage. The task force must decide from among two very costly options: install multi-million-dollar cryogenic reliquefaction plants that use enormous amounts of electrical power to re-liquefy the gas, or continually vent the evaporating volumes into the atmosphere, while commercializing them, thus forcing the government to remain under pressure to keep buying substitute spot cargoes at high market rates to replenish the national target level.

Strategic Fiscal Briefing: Internal technical audits indicate that a 30-day strategic buffer of LNG at current demand levels would result in an unanticipated operating cost burden of around $1.2 billion per year. That amount doesn't include the initial capex to install the specialized double-walled containment structures, that cost about 3.5 times more per MMBtu of storage capacity than traditional crude oil caverns.

In addition, the "budgetary" terms of the pact reflect a one-sided cost sharing. Under the revised 'Free and Open Indo-Pacific' (FOIP) energy principles, Japan's high-level role will be based on technology transfers, joint upstream investments in third countries and market-stabilizing information-sharing mechanisms. The physical strain of constructing, maintaining and insulating the physical cryogenic tank farms along the Indian coastline is entirely borne by Indian state-run public sector undertakings (PSUs) such as GAIL and IOCL. By focusing the dialogue on general geopolitical cooperation, the real money has been buried under off-balance-sheet arrangements, away from the view of the immediate fiscal deficit metrics.

Structural Metrics: Strategic Petroleum Reserves vs. Cryogenic Gas Stockpiles

To highlight the different economic characteristics of these national priority assets, the following comparative outline sheds light on the structural contrast between traditional oil stockpiling and the new LNG reserve scheme under the 2026 agreement:

| Operational Metric | Strategic Petroleum Reserves (SPR) | Cryogenic LNG Stockpiles |

|---|---|---|

| Primary Storage Technology | Underground Salt/Rock Caverns | Above-Ground Double-Walled Cryogenic Tanks |

| Storage Temperature | Ambient Temperature (15°C – 25°C) | Supercooled Cryogenic (−162°C) |

| Boil-Off / Asset Degradation | Negligible (<0.05% per annum) | High (0.05% to 0.15% daily evaporation loss) |

| Estimated CapEx (per MMBtu) | $4.50 – $6.00 | $18.50 – $24.00 |

| Energy Input for Maintenance | Very Low (Occasional pumping power) | Extreme (Continuous cooling & reliquefaction) |

| Infrastructure Lifespan | 50+ Years with minimal overhaul | 20–25 Years before critical alloy fatigue |

This systematic comparison exposes the core flaw in treating the LNG stockpiling pact as an extension of normal energy security accounting. The capital velocity required to maintain a liquid methane shield is drastically higher than that of crude oil. Over a typical twenty-year operating horizon, the cumulative losses from boil-off control, along with the tremendous energy requirements to run the refrigeration cycles, end up increasing the initial cost of the gas holding by a factor of two. These figures have never been incorporated into the Ministry's public financial forecasts, suggesting a sizable, off-balance sheet debt that will be passed on to the taxpayers of tomorrow.

The Geopolitical Premium and Currency Volatility

The economic-financial rationale for incurring this high fiscal burden is closely related to the evolving global macro environment. Among the major breakthroughs achieved in the Modi-Takaichi talks was the development of a bilateral local-currency settlement mechanism. To enable businesses to make direct cross-border payments in Indian Rupees (INR) and Japanese Yen (JPY), the mechanism is now in place to facilitate direct payment bills between Indian and Japanese companies. Japanese non-residents are allowed to open special bank accounts in Indian banks. Subsequently, the goal of long-term development in policy is suggested: shielding bilateral energy trade from the volatile revaluations of the United States Dollar (USD) and also alleviating transaction frictions of the global SWIFT network with which it is often associated.

However, even this complex financial product has latent risk. While the Rupee-Yen direct clearing system cushions both the countries against any sudden dollar shocks, it makes the LNG pact vulnerable to the structural weaknesses of its two domestic currencies. The Yen has traditionally been a funding currency that suffers from severe macroeconomic headwinds and is extremely dependent on global interest rate differentials. The rupee constantly has to deal with domestic inflationary forces, for one. When the exchange rate dynamic behaves unsettlingly, the value of imports of specialized Japanese cryogenic valves, insulation membranes and re-liquefaction turbines grows by leaps and bounds, inflating the capital spending on the project even more.

"A system for settling currency transactions can be no more robust than the underlying physical trade it was intended to serve. In the domain of energy-asset volatility, it may similarly disguise the role of hidden fiscal risks."

Additionally, many international environmental watchdogs have been sounding the alert on Japan's overall trajectory as a major LNG trader in the Asian theater. Independent audits from entities such as Zero Carbon Analytics have found that Japan's large scale resales of surplus LNG volumes to developing countries in Asia unleashed a massive carbon and methane footprint across the entire supply chain. By closely linking India's storage infrastructure to Japan's regional trading arms, New Delhi inadvertently takes on some of this environmental liability, and risks a stumbling block in its future pursuits of international green finance and sustainable development bonds.

Re-engineering the Balance Sheet: Policy Recommendations

In order for the India-Japan LNG Stockpiling Pact not to become a structural fiscal debt trap, the government has to come out of its opacity policy and adopt a transparent, adaptive multi-layered risk management strategy. Step one is the reshaping of the nation's LNG purchasing contract architecture. The joint task force undertaking should seize the moment and utilize its combined geopolitical leverage to obliterate the restrictive "Destination Clauses" that the West Asian megaproducers are known to wield. These provisions bar purchasers from reselling excess volumes, which in turn confines physical gas within certain latitude and longitude coordinates, and disallows buyers from using flexible, market-based cross-hedging techniques.

Secondly, rather than purely dedicating to government-paid strategic reserves, India needs to create incentives for commercial "Peak-Shaving" facilities developed with private infrastructure conglomerates. In a peak-shaving scenario, high-cost cryogenic storage is partially subsidized by consumers operating the inventory position during seasonal demand peaks — generating active income on the frozen assets rather than being a dead weight on the national accounts.

Lastly, there is a need to develop a regionalized, transparent LNG spot price indicator that is representative of actual South Asian supply-demand dynamics to wean the region off steam-coal linked long-term pricing mechanisms that have long disadvantaged Asian buyers through the infamous 'Asian Premium.'

Read Further

- Japan and India to Set Up Task Force on LNG Stockpiling — The Japan Times

- How West Asia Conflict Threatens LNG Supply Chain Powering India's Economy — Business Standard

- India's Nuclear Target Needs 18,000 Tonnes of Uranium Per Year. It Can't Get Them — OneMint

Disclaimer: All data, factual assessments, and projections presented in this monograph are synthesized from public energy policy studies, geopolitical analysis, and macroeconomic research on India-Japan bilateral energy frameworks. This analysis is compiled for educational and research reference and does not constitute a formal investment brief or sovereign advisory.