In today's hyper-digitized financial landscape, we are led to believe that numbers do not lie. We buy policies based on stellar percentages displayed in bold fonts across front-page advertisements and digital banners. Yet, there is a fundamental friction between algorithmic perfection and operational reality. Just as modern corporate cultures fall into the trap of over-relying on automated metrics while completely abandoning the traditional principles of reflection and rigorous baseline evaluation, the Indian retail health insurance sector has built its entire marketing empire on a deeply deceptive foundation: the Claim Settlement Ratio (CSR).

For decades, a single percentage — often hovering gracefully between 95% and 99% — has been weaponized by insurance companies to build unearned trust. It is presented as an absolute guarantee of reliability, an unassailable metric of financial corporate honour. But in a striking and unprecedented development, the Insurance Regulatory and Development Authority of India (IRDAI) has pulled back the curtain. The regulator's own leadership, spearheaded by Chairman Ajay Seth, has effectively labelled these blanket assertions an institutional misdirection, signalling a massive corporate governance shift that forces the top management's remuneration to be linked to real, customer-centric outcomes rather than engineered, superficial performance charts.

Autonomous Engineering of a Mathematical Fiction

The fundamental crisis of the current health insurance matrix lies in how this math is constructed. To the average middle-class Indian consumer, a Claim Settlement Ratio of 98% implies that out of 100 people who walked into a hospital and submitted their bills, 98 walked out completely reimbursed. This interpretation is entirely wrong. The standard formula historically utilised by insurers to project their operational prowess is a playground of definitions:

CSR = (Total Claims Settled ÷ Total Claims Received) × 100

This equation appears linear and transparent, yet its inputs are thoroughly manipulated. Under the current unstructured framework, there is no single, industry-wide standardised method for defining what constitutes a "received" or "payable" claim in promotional material. Many private healthcare insurers selectively design their marketing baselines. They deliberately count only the claims they internally deem "payable," completely excluding claims that are stuck under multi-layered internal review, delayed in legal arbitration, or categorised under documentation technicalities. By narrowing the denominator, the resulting percentage artificially surges, producing an unblemished aesthetic that completely masks the raw transactional friction experienced by the consumer on the ground.

Furthermore, the headline CSR operates as an aggregate by volume, completely blinding the consumer to the value distribution of payouts. In the fiscal year 2023–24, Indian healthcare insurers processed more than 2.69 crore claims, dispersing an aggregate of approximately ₹83,493 crore. A superficial glance at these multi-billion-rupee numbers suggests an incredibly robust, high-performing pipeline. However, when we perform an analytical deep-dive into the audited data submitted to the regulator, the underlying micro-realities reveal a deeply disturbing asymmetry. The vast majority of these seamlessly settled claims are for minor, low-value, routine outpatient procedures or micro-bills averaging slightly above ₹31,000. These are small, clear-cut cases that require minimal corporate scrutiny and are passed through rapidly to protect the company's volume metrics.

"Evolving expectations of customers and the needs of the economy require us to place greater emphasis on measurable customer outcomes, transparency in decision-making, responsiveness, and sustainable value creation. Accordingly, the revised performance framework will move beyond traditional operational and financial metrics..."

The Real Metrics: Deductions, Disallowances, and Delayed Realities

The true operational failure of the system manifests when a policyholder triggers a claim for a massive, catastrophic medical emergency — the exact scenario for which health insurance is purchased. When a major hospitalisation occurs, the deceptive mask of the 98% CSR completely falls away. The aggregate ratio explicitly fails to reveal the prevalence of partial rejections, deep deductions, and administrative haircuts that leave families in extreme financial distress despite having active coverage.

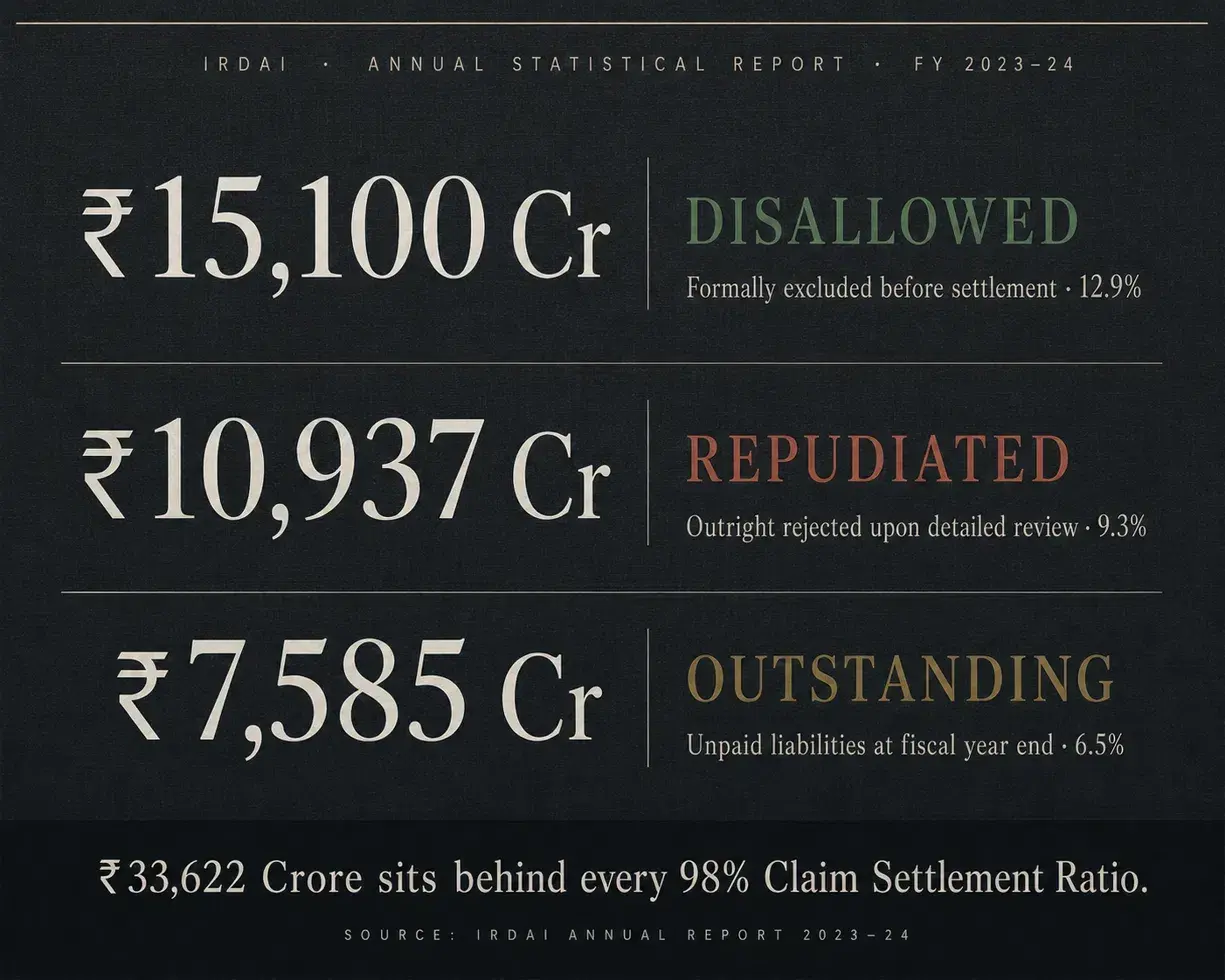

According to comprehensive data compiled by the IRDAI, during the 2023–24 financial cycle alone, a massive sum of approximately ₹15,100 crore was formally disallowed by insurance companies across India. This represents a staggering 12.9% of the total claim amounts filed by policyholders. Think about this reality: nearly thirteen percent of the financial volume that citizens expected to be covered under their legal contracts was flatly refused. On top of these direct deductions, an additional ₹10,937 crore (9.3%) of claims were outright repudiated upon detailed review, and another ₹7,585 crore (6.5%) remained hanging in corporate purgatory as outstanding, unpaid liabilities at the end of the year. When you break down the financial volume, the actual volume-to-value deficit reveals that the real rupee-for-rupee protection received by consumers is nowhere near the 95%+ figures claimed in weekend newspapers.

| Claim Outcome Status (FY 2023–24) | National Volume / Value Share | Real-World Implication for Policyholders |

|---|---|---|

| Settled Volume (Aggregate) | ~83.0% to 87.5% | Dominantly composed of small, routine, low-value outpatient treatments |

| Disallowed Value (Deductions) | 12.9% (₹15,100 crore) | Arbitrary cuts on consumables, PPE, sub-limits, and room rents |

| Repudiated / Rejected Claims | 8.0% to 9.3% | Complete denial of payment due to pre-existing clauses or non-disclosure |

| Outstanding / Pending Year-End | 5.0% to 6.5% | Claims stuck in infinite documentation loops, causing massive debt |

This massive gap between marketing rhetoric and financial execution traces back to complex, predatory clauses embedded within multi-page, fine-print contracts. Insurers continuously exploit structural loopholes such as non-medical exclusions, strict room-rent sub-limits, and tiered waiting periods ranging from 24 to 48 months for specific diseases. Common items vital for surgeries — such as gloves, syringes, administrative charges, and advanced hygiene kits — are summarily classified as "non-payable consumables." Consequently, even if a claim is recorded in the corporate ledger as "100% Settled" for the purpose of the CSR, the policyholder is frequently forced to pay 20% to 40% of the total hospital bill out of their own pocket.

The Structural Redesign: Regulatory Intervention and Mandatory Disclosures

Recognising that the industry's metrics have become a structural hazard to public trust, the IRDAI has initiated an extensive, mandatory corporate governance overhaul. The regulator has issued explicit directives under the revised IRDAI (Corporate Governance for Insurers) Regulations. In an unprecedented move to enforce ethical accountability, the executive remuneration, bonuses, and incentives of Managing Directors (MDs), Chief Executive Officers (CEOs), and Key Managerial Personnel (KMPs) have been explicitly tied directly to measurable customer outcomes rather than top-line premium growth or manipulated settlement volumes.

This regulatory shift targets the complete asymmetry of knowledge that has historically left small retail policyholders at a severe disadvantage when dealing with large, multi-layered financial corporations. The explosive rise in public dissatisfaction is clearly reflected in the regulator's own Bima Bharosa portal. In the recent fiscal period, general and health insurance grievances skyrocketed by nearly 45% in a single year, reaching an alarming 1,37,361 reported disputes. Crucially, over 69% of all documented complaints against general and health insurers were directly linked to severe claims handling issues: prolonged processing delays, unexpected underpayments, or arbitrary, bad-faith rejections.

Ultimately, the era of relying on a single, monolithic, and unverified Claim Settlement Ratio is over. Just as financial survival in the private sphere requires an intentional, conscious approach to personal spending — much like the deliberate, handwritten self-reflection of the traditional Japanese Kakeibo method — evaluating corporate protection requires rigorous, unbundled analysis. As the updated regulatory framework takes immediate effect, consumers must look past headline percentages and demand deep transparency regarding partial payouts, actual out-of-pocket costs, and real turnaround speeds. Only when top insurance executives are financially penalised for delayed and deducted claims will the corporate apparatus shift from engineering brilliant marketing statistics to providing genuine, compassionate healthcare security for the citizens of India.

References

[1] Insurance Regulatory and Development Authority of India (IRDAI). Annual Report 2023–24: Health Insurance Claims Data and Statistical Supplement — Click here

[2] Press Information Bureau, Government of India. IRDAI Revises Corporate Governance Framework Linking Executive Pay to Customer Outcomes — Click here

Disclaimer: All the data, statutory facts, and regulatory quotes provided above were meticulously compiled from verified public internet resources, official Press Information Bureau (PIB) releases, and the audited annual statistical publications of the Insurance Regulatory and Development Authority of India (IRDAI). This investigative analysis is strictly intended for educational and general informational awareness and must not be construed as formal, definitive legal, financial, or corporate insurance advice.